The story of US real-time payments since 2017 has been one of two parallel rails maturing into a single operating reality for most banks. The Clearing House launched RTP that year as a private-sector real-time settlement network. The Federal Reserve launched FedNow in July 2023 as a public-sector counterpart. By the end of 2025, both networks settle billions of dollars of transactions daily, both are still growing at double-digit rates, and most US banks of any meaningful size now connect to both. The Clearing House reports that RTP reached more than 700 financial institutions and over $400 billion in cumulative volume by Q3 2025.

That two-rail outcome was not the result anyone predicted at the start. The original expectation was that one rail would absorb the other. Instead, both have grown by accommodating different bank profiles, different transaction types, and different reach requirements. The story below is what actually happened on the ground, what the numbers reveal about the next stage of US real-time payments, and what fintech infrastructure builders should be planning around as the rails normalise into a settled piece of US financial plumbing.

The state of US real-time payments infrastructure in 2025

US real-time payments crossed two meaningful thresholds in 2025. The first was that combined RTP and FedNow daily volumes consistently outran the daily volumes of same-day ACH for selected use cases like payroll deferrals, gig-worker payouts, and B2B last-mile payments. The second was that the network of banks supporting at least one rail expanded to cover roughly 87 percent of US deposit accounts, up from below 60 percent at the start of 2024. The reach expansion is what unlocked corporate treasury teams to design real-time into core payment flows, rather than treating it as a niche product reserved for one or two use cases.

Federal Reserve quarterly statistics show FedNow processed approximately $853 billion in 2025, with quarter-over-quarter growth averaging 35 percent. RTP processed about $560 billion in the same period at a steadier 18 percent quarterly growth rate. Combined annual settlement runrate sits near $1.2 trillion as of late 2025, less than 1 percent of total US payment volume but the fastest-growing payment category by a wide margin.

The threshold question has shifted accordingly. The conversation in 2024 was whether real-time would scale at all. The conversation in 2025 is what real-time replaces and on what timeline. The answer that is emerging is that the rails replace expensive same-day ACH for selected high-value-per-transaction flows, and they sit alongside ACH and card rails for everything else, at least for the next several years.

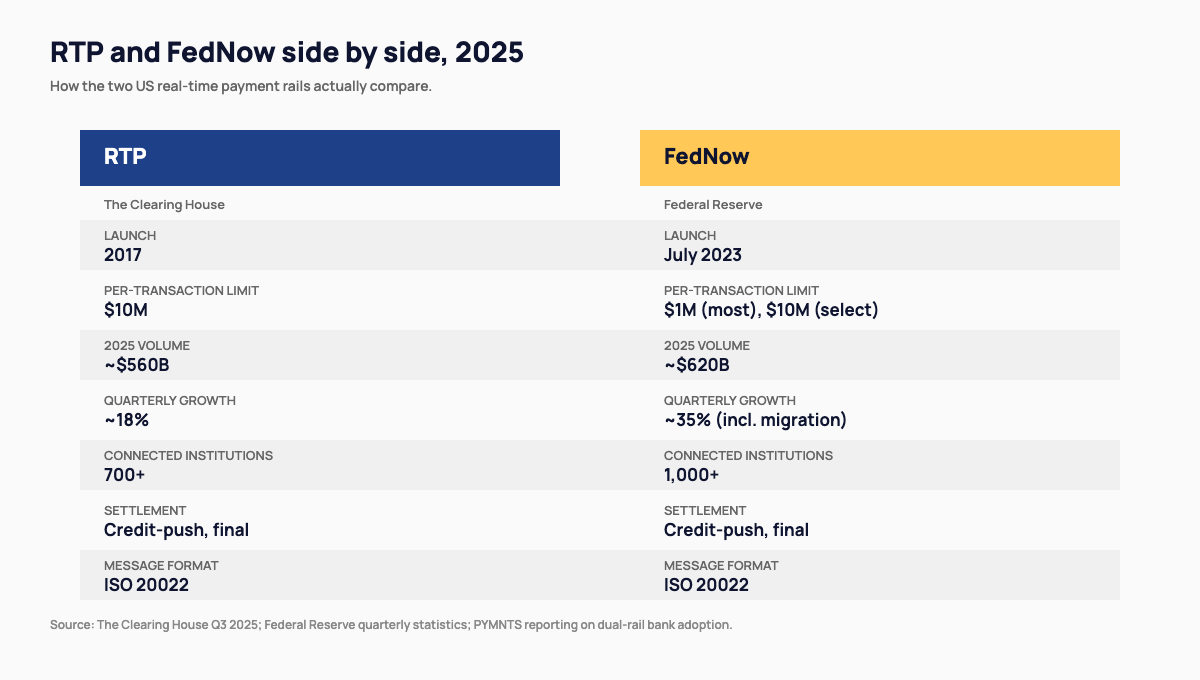

How the two networks compare, and why most banks pick both

The two networks differ on five points that matter for bank treasury teams. First, transaction limits. RTP recently raised its per-transaction limit to $10 million, while FedNow currently caps at $1 million for most participants and $10 million for select sponsors. Second, settlement model. Both are credit-push only and final settlement, with no clawback. Third, ownership and governance. RTP is operated by The Clearing House and owned by its bank participants, while FedNow is operated by the Federal Reserve. Fourth, message format. Both use ISO 20022, but with different supplementary fields. Fifth, fee structure. FedNow’s fee schedule is publicly published and lower per-transaction than RTP for small institutions, which has accelerated FedNow uptake among community banks.

PYMNTS reporting finds that 58 percent of US banks now use both RTP and FedNow, up from less than 20 percent in mid-2024. The reason is reach. Some receiving banks connect only to RTP, others only to FedNow, and a small but meaningful set connect to neither. A bank that wants to guarantee its corporate clients can pay or receive from any counterpart needs both rails. The dual-rail architecture has become the de facto standard for any bank above a few billion dollars in deposits, and that pattern is unlikely to reverse before the end of the decade.

What the FedNow growth rate hides, and where ACH still fits

FedNow’s 35 percent quarter-over-quarter growth rate is the headline that draws coverage, but the figure compresses two distinct dynamics. The first is real new payment volume from corporate treasury and gig-economy use cases. The second is migration. Small and mid-sized banks that had connected to RTP first are adding FedNow as a redundancy layer rather than as a new payment surface. Strip out the migration component and FedNow’s organic growth rate sits closer to 20 to 22 percent, still impressive but less explosive than the headline suggests.

ACH still carries the vast majority of US payments by volume. Same-day ACH alone processed over $2.4 trillion in 2024, about three times the combined real-time volume even after the 2025 surge. The framing that has settled inside payments treasury teams is that real-time is not yet replacing ACH wholesale. It is replacing the pain points where ACH’s batch settlement window or T+1 timing produced commercial friction. The categories where this has happened first are payroll, insurance claims, and B2B invoice settlement. The categories where ACH continues to dominate are recurring bill payments, government disbursements, and any flow where receiver-pull semantics matter more than instant credit. That coexistence will hold for years before the rails-mix shifts decisively in real-time’s favour.

The international comparison, and what it says about the US gap

The international comparison is where US real-time payments still trail meaningfully. India’s UPI processed more than 130 billion transactions in 2024, an order of magnitude above combined US real-time volume. Brazil’s PIX, launched in 2020, settled the equivalent of 25 percent of Brazilian GDP in 2024 and reached roughly 80 percent retail-payment penetration. The UK’s Faster Payments Service has been operating since 2008 and is fully embedded in retail commerce.

The US is comparatively late and comparatively fragmented. The dual-rail architecture, while pragmatic, adds complexity that single-rail jurisdictions like Brazil avoid. The volume gap reflects that, but it also reflects the structural reality that the US has the world’s deepest card-payment infrastructure already, which dampens the urgency to migrate toward a single instant rail. Open innovation patterns playing out across US finance are slowly shifting that, but the catch-up will be measured in years rather than quarters, and the more interesting question for US infrastructure builders is which international design choices to import deliberately and which to adapt for the dual-rail context.

What this means for fintech infrastructure builders, and what 2026 brings

For fintech infrastructure builders, the practical lesson is that real-time is now table stakes for any new payment product targeting US banks or merchants. Building only on ACH or card rails in 2026 limits commercial appeal to a narrow customer set. The strategic question for builders is which abstraction layer to position at: pure rail-access (compete with bank-as-a-service incumbents), instant-payout product layer (target gig platforms and marketplaces), or treasury-orchestration layer (target mid-market corporates). Each layer has different unit economics and different competitive dynamics, and conflating them is how new entrants end up under-priced and under-resourced after their first two years of operation.

What’s coming in 2026 has three legible threads. The first is FedNow raising its per-transaction limit, which will pull in the larger corporate treasury flows that currently still default to wire. The second is fraud and dispute handling. The credit-push, no-clawback model leaves consumer-protection gaps that the CFPB has signalled it intends to address through new guidance. The third is cross-border real-time, where The Clearing House and Federal Reserve are both piloting interoperability with non-US instant rails. The first thread is operational in Q1 2026, the second is regulatory and slow, and the third is years away. Payments systems and infrastructure across the US fintech stack will be feeling the consequences of the first two well before the third matures into anything builders can plan around.