Walk past the analytics floor of any large US bank and you will hear two languages in the air. One is Python, which has won most of the data engineering and machine learning work. The other is R, which never quite left, and which still runs a meaningful slice of the risk, pricing, and regulatory analytics that move actual dollars. R programming for finance has settled into a smaller but durable role, and the firms that use it have specific reasons for doing so.

Where R Programming for Finance Actually Lives Today

Inside US financial institutions, R is concentrated in three places. The first is risk and capital modeling, where stress testing teams at the largest banks build, calibrate, and document models that ultimately get reviewed by the Federal Reserve. The second is buy-side research, where hedge funds, quant shops, and asset managers run statistical work on time series and cross-sectional return data. The third is regulatory and compliance analytics, where teams produce reports that need a clear audit trail from raw data to the final figure.

None of these have moved wholesale to Python, and the reason is more cultural than technical. R was built by statisticians, and the statistical literature inside finance, including a long shelf of textbooks on time series, derivatives pricing, and credit risk, still ships with R code. When a new graduate from a US masters in financial engineering arrives at a desk, they often already know R, and the desk is already running R packages that match the papers they read.

Survey data from Stack Overflow and the JetBrains developer ecosystem report puts R in roughly 4 to 6 percent of professional developer use, far behind Python. But inside US banking quantitative analytics teams, the share is meaningfully higher, and inside academic-leaning corners of buy-side firms it is higher still.

Job market data adds a second signal. Postings in the US that explicitly require R have not collapsed. They have shifted toward roles labelled quantitative analyst, risk modeler, model validator, and senior data scientist, rather than the generic data analyst role where Python now dominates. The pay band for senior R-fluent roles inside US banks remains competitive with the Python equivalent.

The Specific Workloads R Handles Cleanly

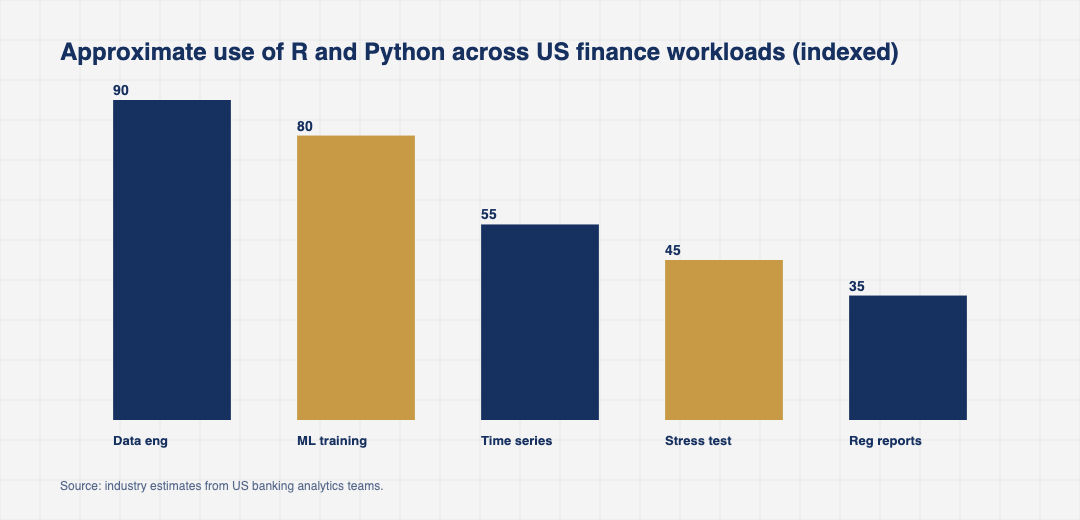

R is strong where statistics is the product, not the supporting layer. A few workloads in US finance illustrate the pattern.

Time series forecasting is the clearest case. The forecast package, fable, prophet, and a wide range of state space and regime switching libraries make it straightforward to estimate, validate, and present models on financial series. Analysts can move from a raw price file to a calibrated model with confidence intervals and residual diagnostics in fewer lines than the Python equivalent.

Statistical inference is the second case. When a team needs a clean hypothesis test, a properly specified mixed effects model, or a Bayesian posterior, R has decades of peer-reviewed packages behind it. For US regulators reviewing a model, that lineage is a feature, not a footnote.

Reproducible reporting is the third case. R Markdown and Quarto allow analysts to interleave code, output, charts, and prose in a single document that re-runs end to end. For monthly risk reports, regulatory submissions, and internal valuation memos at US banks, this matters. A reviewer can run the document again and verify that every number on the page came from the data on the date stamped at the top.

R Versus Python in the US Finance Stack

The comparison between R and Python inside US finance is not really a contest. It is a division of labor that has stabilized.

Python sits in the engineering pipeline. Data ingestion, feature stores, machine learning model training, deployment, and orchestration in services like Airflow, MLflow, and Databricks have settled on Python. The job postings for ML engineers and quant developers at US banks reflect this clearly.

R sits in the analytical bench. When a senior quant needs to look at a series, fit several specifications, and decide which model is fit for purpose, the work usually happens in R. When that model is approved, it often gets translated, sometimes wrapped, sometimes rewritten, into the Python or C++ that production uses.

This split is not new. What is new in 2026 is that the firms running it have stopped trying to consolidate. After several rounds of failed migrations, most large US banks have accepted that R will remain in the modeling layer for at least the next several years.

One subtle reason R has held on is that the analytical work itself is often more important than its place in the production pipeline. The cost of running a model in Python in production is real, but it is dwarfed by the cost of getting the model wrong in the first place. Senior US quants tend to be conservative about where they do the actual modeling, and R is still where many of them are most fluent.

The Friction Points US Banks Still Run Into With R

R is not without cost in a regulated US environment. Three friction points come up repeatedly.

The first is dependency management. CRAN package versions evolve, sometimes with breaking changes, and reproducing a model from three years ago requires careful version pinning. Renv and Posit Package Manager have made this tractable, but it remains operational work that Python users with locked virtual environments often take for granted.

The second is talent supply. The pool of strong R programmers in the US is smaller than the Python pool and has been declining at the entry level. Banks have responded by training internally, by hiring from statistics and biostatistics graduate programs, and by keeping senior R users on long retention plans. The talent question is the single most cited reason why some teams are slowly migrating off R, even when the analytical case for staying is clear.

The third is integration with modern data platforms. R has connectors to Snowflake, Databricks, BigQuery, and S3, but the experience is not always as polished as the Python equivalent. For very large feature engineering jobs, US teams often pull data into R for analysis only after the heavy lifting is done elsewhere.

Where R Programming for Finance Is Heading

Three signals shape the trajectory.

The first is Quarto. Built by Posit, Quarto extends the R Markdown model to Python, Julia, and Observable, and standardizes the way reproducible technical documents are produced. For US banks that have invested heavily in R Markdown for regulatory reporting, Quarto offers a path forward without forcing a rewrite.

The second is the deepening overlap between R and Python through tools like reticulate and rpy2. Inside a single analytical project, US quants now routinely call Python from R or R from Python, depending on which language has the better library for a given task. This pragmatic interoperability is what allows R to keep its niche.

The third is the slow but steady investment in R model deployment tools. Plumber for APIs, Pins for model artefacts, and Vetiver for production lifecycle management have closed some of the gap between an interactive R session and a model serving real traffic. For some workloads at smaller US firms, this is enough to keep the whole pipeline in R.

For US banking technology leaders, the practical question is not whether to invest in R, but how much of the analytical bench to keep there and how to manage the interface to the Python production layer.

R will not displace Python in US finance, and most teams stopped expecting it to. The interesting question is the opposite one. Where the analysis is hard, the statistics matters, and the audit trail has to survive a regulator, R is still doing useful work inside the US financial system. Quietly, but consistently, and with a community that has stopped apologizing for being smaller than the one next door.