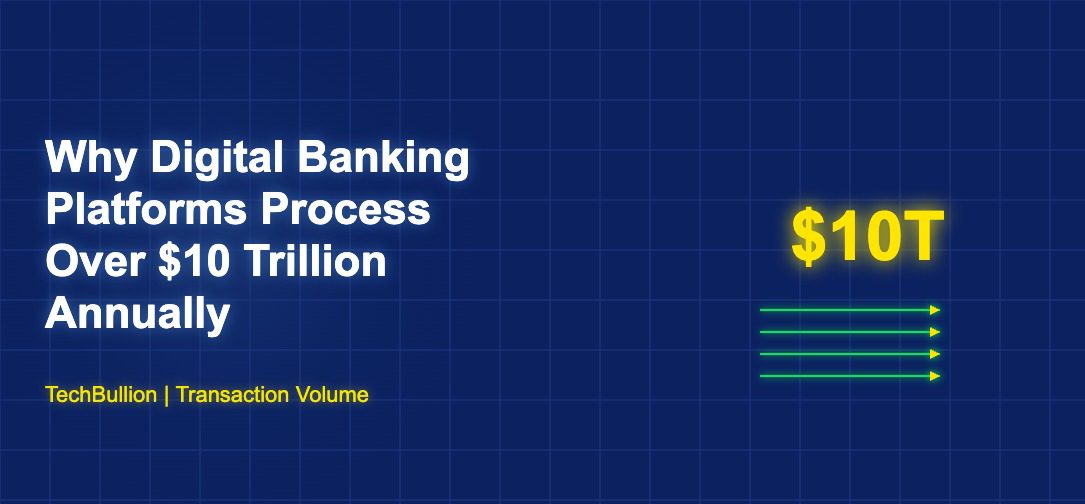

The Scale of Digital Banking Transaction Volumes

Digital banking platforms now process over $10 trillion in transactions annually, a figure that encompasses payments, transfers, lending disbursements, investment transactions, and other financial flows conducted through digital channels. This transaction volume, compiled from data reported by major digital banking platforms, central banks, and industry analytics firms like Statista, reflects the scale at which digital banking has become central to the global financial system rather than a niche alternative to traditional banking.

The $10 trillion figure is particularly significant because it demonstrates that digital banking has moved beyond consumer convenience into systemically important territory. Transaction volumes of this magnitude mean that digital banking platforms are processing a meaningful share of global economic activity, creating both opportunities and responsibilities that come with systemic relevance.

Payment Transactions Driving the Largest Volume

Payment processing accounts for the majority of digital banking transaction volume. Consumer payments through digital wallets, mobile banking apps, and online payment platforms generate billions of individual transactions that collectively represent trillions of dollars in value. Business payments processed through digital banking platforms, including payroll, vendor payments, and commercial transactions, add substantial additional volume.

The growth in digital payment volume reflects the ongoing shift from cash and check-based transactions to digital alternatives. In markets where this shift is most advanced, such as China, India, and the Scandinavian countries, digital payments have become the dominant transaction method, with cash usage declining to a small fraction of total transactions. Even in markets where cash remains more prevalent, the trend toward digital payments is consistent and accelerating.

Cross-Border Transactions Adding Significant Volume

International money transfers and cross-border payments processed through digital platforms contribute significantly to the $10 trillion total. Platforms like Wise, Remitly, and PayPal process billions of dollars in cross-border transactions that would previously have flowed through traditional correspondent banking channels or physical money transfer operators.

The migration of cross-border transactions to digital platforms is driven by cost savings, speed improvements, and convenience advantages that digital platforms offer over traditional alternatives. According to the World Bank, the average cost of sending remittances has declined in corridors where digital platforms have gained significant market share, demonstrating the competitive pressure that digital banking volume creates on traditional cross-border payment pricing.

Lending Disbursements Through Digital Channels

Digital lending platforms contribute to transaction volume through loan origination and disbursement. Consumer loans, small business credit, buy-now-pay-later transactions, and various forms of digital credit represent a growing share of total lending activity, with disbursements and repayments flowing through digital banking infrastructure.

The speed of digital lending transactions is particularly notable. While traditional bank loans may take weeks to process and disburse, many digital lending platforms complete the entire process from application through disbursement in minutes or hours. This speed means that digital lending platforms can process more transactions per unit of time, contributing to overall transaction volume growth.

Investment and Wealth Management Activity

Digital investment platforms contribute to transaction volume through stock trades, fund purchases, cryptocurrency transactions, and various other investment activities. The democratization of investing through platforms like Robinhood, eToro, and various robo-advisors has dramatically increased the number of individual investment transactions, with millions of retail investors making trades through mobile applications daily.

Cryptocurrency exchanges process particularly high transaction volumes due to the 24/7 nature of crypto markets and the high trading frequency among crypto enthusiasts. While the dollar volume of crypto transactions fluctuates with market conditions, the cumulative contribution to digital banking transaction volumes has been substantial during periods of active market participation.

Infrastructure Supporting Trillion-Dollar Volumes

Processing over $10 trillion in annual transactions requires massive and highly reliable technology infrastructure. Digital banking platforms invest heavily in systems capable of handling peak transaction loads, maintaining data consistency across distributed systems, and ensuring that every transaction is processed accurately and securely.

The infrastructure requirements for trillion-dollar transaction processing include real-time processing capabilities that can handle thousands of transactions per second, redundant systems that ensure service continuity during component failures, and comprehensive security systems that protect against both external threats and internal errors. The engineering challenges of operating at this scale are substantial and represent a significant competitive moat for platforms that have successfully built and maintained the required infrastructure.

Regulatory Implications of Systemic Scale

As digital banking platforms process transaction volumes that represent a meaningful share of total economic activity, regulatory attention increases correspondingly. Regulators responsible for financial stability are increasingly interested in understanding the operational resilience, risk management practices, and contingency planning of digital banking platforms whose failure could have broader systemic implications.

This regulatory attention is both a challenge and a validation for digital banking platforms. Meeting heightened regulatory expectations requires ongoing investment in compliance, risk management, and operational resilience. But the regulatory acknowledgment of digital banking’s systemic importance also legitimizes the platforms and may ultimately create regulatory frameworks that support their continued growth within appropriate guardrails.

The Trajectory Toward Even Larger Volumes

The $10 trillion annual transaction volume will continue growing as digital banking penetration increases globally, as more transaction types move to digital channels, and as the global economy itself grows. Each of these factors contributes independently to volume growth, and their combined effect suggests that digital banking transaction volumes will continue climbing for years to come.

The growth trajectory raises important questions about the future structure of the financial system. As digital platforms process an ever-larger share of financial transactions, the balance of power, influence, and responsibility between traditional financial institutions and digital platforms will continue shifting. The platforms that process these trillions in transactions are not merely technology companies. They are becoming core financial infrastructure upon which the global economy increasingly depends.