Walk through the programmatic advertising ecosystem and you will eventually hit a wall. Actually, you will hit three of them. Alphabet, Meta, and Amazon have each constructed advertising environments so complete, so deeply instrumented, and so commercially self-sufficient that the data, the audiences, the inventory, and the measurement all remain firmly inside their perimeters. What the industry calls walled gardens are not metaphors. They are the defining architectural feature of modern digital advertising, and understanding what sits behind each wall explains why three companies headquartered within 50 miles of each other in the United States are absorbing nearly two-thirds of global digital advertising spend outside China.

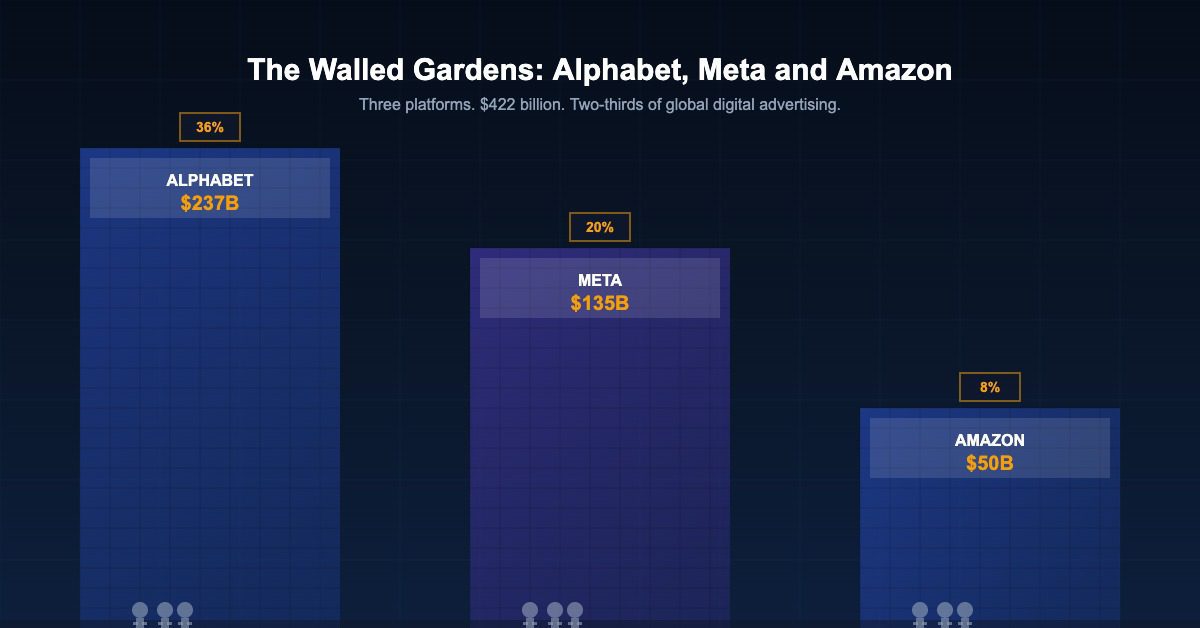

Together, Alphabet, Meta, and Amazon generated approximately $422 billion in advertising revenue in 2024, according to each company’s investor relations filings and GroupM’s This Year Next Year global advertising forecast. That figure represents roughly 64 per cent of all digital advertising revenue generated outside China, a level of market concentration that has no precedent in the history of media. Understanding what built these walls, what keeps them standing, and what forces might eventually bring them down is the most consequential strategic question in the advertising industry today.

Alphabet Built the First and Deepest Wall in Digital Advertising History

Google’s advertising operation, which generated $237 billion in revenue in 2024, is the most vertically integrated structure in the history of the advertising industry. The wall that Alphabet has built is not a single barrier but a series of concentric ones, each reinforcing the others and each feeding the same data advantage that makes the system increasingly difficult to compete against.

At the outermost ring sits Google Search, which processes more than 8.5 billion queries per day and represents the world’s largest database of commercial intent. When a user types “best running shoes for flat feet” into a search bar, they are providing Google with a targeting signal of extraordinary specificity, one that no social platform, no publisher, and no programmatic network can replicate from outside Google’s environment. Search advertising generated approximately $175 billion of Alphabet’s revenue in 2024, according to the company’s financial disclosures, precisely because intent at the moment of query is the most commercially valuable signal in advertising.

Inside that ring sits YouTube, which reaches over 2.7 billion monthly logged-in users and gives Alphabet dominance over online video advertising at scale. Google Ad Manager controls the ad serving layer for a substantial proportion of the world’s premium publisher inventory. Google’s DV360 demand-side platform gives advertisers the tools to buy that publisher inventory programmatically. Campaign Manager 360 handles attribution across all Google-managed campaigns. The result is that an advertiser running activity across Search, YouTube, and programmatic display can conduct the entire operation within Google’s walled garden, with measurement provided by Google’s own tools and optimisation powered by Google’s own machine learning.

style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;” style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;”

| Company | 2024 Ad Revenue | Primary Platform | Global Share |

|---|---|---|---|

| Alphabet (Google) | $237 billion | Search, YouTube, Display | ~36% |

| Meta Platforms | $135 billion | Facebook, Instagram, WhatsApp | ~20% |

| Amazon Advertising | $50 billion | Sponsored Products, DSP, Video | ~8% |

| All Three Combined | ~$422 billion | Multiple | ~64% (non-China) |

Sources: Company investor relations filings; GroupM This Year Next Year 2024; Insider Intelligence

Meta’s Wall Is Built on Something No Other Platform Has: the Social Graph at Global Scale

Meta’s advertising business, which generated approximately $135 billion in revenue in 2024, is constructed on a different foundation from Alphabet’s. Where Google’s advantage begins with search intent, Meta’s begins with identity. The social graph accumulated across Facebook and Instagram over more than two decades, connecting people to friends, family, interests, and communities, gives Meta a targeting capability based on declared relationships and expressed interests that no external platform can access or approximate.

With approximately 3.27 billion daily active users across its family of applications, Meta offers advertisers reach that genuinely has no equivalent in the history of media. The ability to run a single campaign that reaches a precisely defined audience across Facebook, Instagram, Messenger, and WhatsApp with consistent frequency management and cross-surface attribution is a capability that Meta’s walled garden provides and the open programmatic ecosystem cannot replicate. Every additional day of user activity deepens the social graph, adds to the interest taxonomy, and improves the targeting precision that Meta’s advertising products deliver to brands.

Meta’s machine learning infrastructure, which the company markets as Advantage+, has reached a level of sophistication where many advertisers report that allowing Meta’s algorithms complete creative and audience optimisation control outperforms human-managed campaign structures. This creates a form of dependency that reinforces the walled garden: advertisers who have allowed Meta’s systems to learn from years of campaign performance data are investing in a machine learning model that delivers improving returns and represents a switching cost when considering moving budget elsewhere.

Amazon’s Wall Is the Only One Built Directly on Purchase Data

Amazon Advertising’s $50 billion in 2024 revenue is built on a structural advantage that neither Alphabet nor Meta can replicate: the direct connection between advertising exposure and verified commercial transaction. Amazon knows not just what its customers searched for and what content they consumed, but what they actually bought, how much they spent, when they buy again, and how their purchasing behaviour evolves across hundreds of product categories over years of shopping history.

This purchase data foundation gives Amazon’s measurement proposition a quality of commercial evidence that pure-play media platforms cannot match. When a brand runs a Sponsored Products campaign on Amazon, the measurement output is not a CTR or a viewability percentage but a sales figure, expressed in units sold and revenue generated, attributed directly to advertising exposure through Amazon’s own transaction records. That closed-loop attribution model, grounded in actual commerce rather than modelled probability, is the most compelling measurement story in digital advertising.

The Amazon walled garden extends beyond its own marketplace through Amazon DSP, which allows advertisers to target Amazon audience segments across publisher inventory outside Amazon’s own properties. Amazon’s measurement still closes the loop through Amazon purchase data regardless of where the impression was served, giving brands a performance measurement capability for off-site programmatic advertising that exceeds what any independent ad tech vendor can offer without the transaction data anchor.

What Makes These Gardens Walls Rather Than Simply Platforms

style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;” style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;”

| Walled Garden | Core Data Advantage | Advertiser Lock-In Factor | Regulatory Challenge |

|---|---|---|---|

| Google / Alphabet | Search intent at point of query | 15+ years of campaign history in Smart Bidding | DOJ antitrust case (2024) |

| Meta Platforms | Social graph and declared interests | Cross-app audience continuity | EU Digital Markets Act gatekeeper |

| Amazon | Purchase history and intent signals | Closed-loop transaction attribution | FTC retail market investigations |

Sources: DOJ antitrust filings; European Commission DMA enforcement; FTC market studies

The defining characteristic of a walled garden is not size but interoperability, or rather the deliberate absence of it. Each of the three dominant platforms keeps advertiser data, audience data, and measurement data entirely within its own environment. An advertiser who builds campaign history, trains audience models, or creates conversion measurement infrastructure inside Google’s ecosystem cannot transfer any of that investment to Meta or Amazon. The data stays inside the wall.

This creates switching costs that compound over time. A brand that has operated Google Smart Bidding campaigns for a decade has contributed years of conversion signals to Google’s machine learning models, progressively improving the algorithm’s ability to allocate that brand’s budget efficiently. Moving budget to a competitor resets that learning entirely. The longer an advertiser spends inside a walled garden, the more valuable their presence becomes to the platform and the more expensive their exit becomes to themselves. This dynamic is not accidental: it is the mechanism through which platform lock-in is maintained without any formal contractual restriction.

Regulatory Pressure Is Testing the Walls from Multiple Directions

The concentration of digital advertising revenue within three walled gardens has attracted regulatory attention across every major jurisdiction simultaneously. The US Department of Justice’s antitrust case against Google’s advertising technology business, which went to trial in 2024, argued that Google has illegally maintained monopolies in publisher ad servers and ad exchanges by tying its own tools together and excluding competitors. The case specifically targeted the vertical integration that makes Google’s walled garden so commercially durable, and any structural remedy could require Google to divest either its buy-side or sell-side advertising tools.

The European Union’s Digital Markets Act, which entered full enforcement in 2024, designates Alphabet, Meta, and Amazon as gatekeepers and imposes obligations including data access for third parties, interoperability requirements, and fair trading rules that specifically target the mechanisms by which walled gardens exclude competition. The DMA’s requirement that gatekeepers allow third-party programmatic advertising vendors equivalent access to their platforms’ data and functionality is directly aimed at the self-preferencing that sustains platform dominance.

The UK’s Competition and Markets Authority has published detailed market studies concluding that the vertical integration of Google’s advertising technology stack gives it the ability to preference its own products at each layer of the ecosystem to the detriment of publishers, advertisers, and competing technology vendors. The CMA’s proposed remedies are among the most structurally ambitious of any regulator, including mandatory separation of buy-side and sell-side tools and real-time access to auction data for third parties.

What Lies Outside the Walls and Why It Still Matters

The open programmatic ecosystem that operates outside the three walled gardens is not trivial. The Trade Desk generated approximately $1.95 billion in revenue in 2023 serving advertisers who want independent, non-platform-aligned buying infrastructure. Magnite, PubMatic, and Index Exchange collectively represent billions of dollars in publisher monetisation for inventory that sits outside platform control. Connected television, which is rapidly becoming the most strategically important advertising channel, is largely outside the direct control of the three walled gardens and depends on independent attribution technology and programmatic infrastructure.

The deprecation of third-party cookies, which Google has repeatedly delayed but not abandoned as a direction of travel, is restructuring the economics of the open ecosystem in ways that cut both ways. On one hand, it removes the cross-site behavioural targeting that independent programmatic advertising relied upon. On the other, it increases the relative value of first-party data held by publishers and brands, creating demand for the clean room technology, identity resolution services, and data collaboration infrastructure that independent vendors are building.

The three walled gardens will not be dismantled by regulatory action alone. Network effects, data advantages accumulated over decades, and the genuine commercial performance of their advertising products create durable structural advantages that no intervention can eliminate entirely. What regulation can do, and what it is beginning to do, is constrain the most extreme forms of self-preferencing, mandate some degree of data access and interoperability, and create space for independent technology vendors to compete in categories that walled gardens have historically foreclosed. That competition, however constrained, is where the most interesting AdTech innovation is being built.

Related reading: AdTech Market Concentration: Why Three Companies Control 56% | Retail Media Technology | Programmatic Advertising and RTB | Privacy-Preserving Advertising

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.