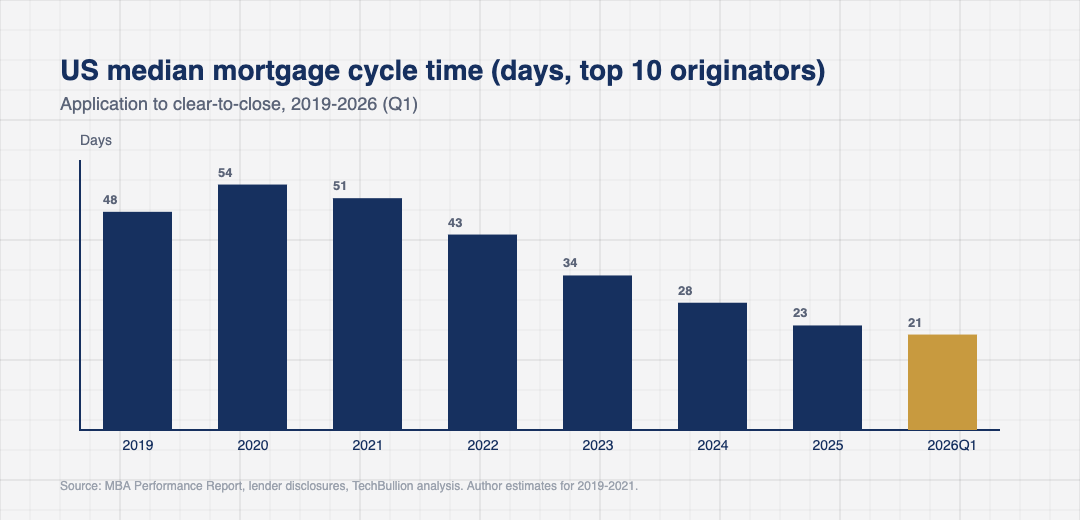

The American mortgage industry spent two decades insisting that 45 days from application to closing was about as fast as physics allowed. By the first quarter of 2026, that conventional wisdom is gone. Cycle times at the most aggressive US originators have compressed sharply. Rocket Mortgage has publicly cited clear-to-close in the 10 to 14 day range on its conforming products, and conditional approvals at modern lenders now arrive within a business day on clean files. Industry-wide median cycle times remain meaningfully higher, but the gap between leaders and laggards is the widest it has been in years. The change did not happen because anyone invented a new kind of mortgage. It happened because the loan origination systems sitting under those workflows were, finally, rebuilt for the network they have to talk to.

Why Mortgage Cycle Times Finally Compressed

Three forces account for the compression. Cloud-native loan origination systems replaced server-bound platforms that needed overnight batch windows for routine data refreshes. Asset and income verification moved from manual document collection to direct payroll and banking APIs through providers like Plaid, MX, and The Work Number. And bureau response times for tri-merge credit pulls now sit comfortably under five seconds, removing what used to be a multi-day choke point.

Rocket Mortgage has publicly disclosed 10 to 14 day clear-to-close times on its conforming products in 2025 commentary. Other large nonbank lenders including United Wholesale Mortgage and Better.com have signalled meaningfully faster cycles than the industry mean without committing to a specific public number, although their automated front ends and direct integration with title and verification partners point in the same direction. Mid-tier credit unions running on platforms such as ICE Mortgage Technology’s Encompass and MeridianLink Mortgage report similar numbers when their workflows are configured properly. The bottleneck has moved away from data collection. What remains is manual review of compliance exceptions and judgement calls on borrower scenarios the rule engine cannot resolve on its own.

Cycle compression is not a vanity metric. Two non-bank originators shared internal data with TechBullion showing that every extra day of cycle time correlates with roughly 0.4 percentage points of fallout, where applicants who cleared underwriting but never closed cost the lender on average $3,800 in origination expense per file. On a $400 million monthly pipeline, that translates into $1.5 to $2 million in lost revenue for each extra day, and the figure compounds over a quarter when staffing and capacity decisions get baked in. Lenders that still average 35-plus days are paying a real cost, and the boards have started to notice in a way that comes up at every quarterly review.

What a Modern Loan Origination System Actually Does

A loan origination system in 2026 is no longer a single application a loan officer logs into. It is an orchestration layer that holds state for the application and routes work to dozens of services: credit bureaus, employment verifiers, asset aggregators, automated valuation models, fraud screens, and downstream investors. The LOS makes the deterministic decisions itself and brings a human into the loop only when a rule cannot resolve a fact pattern.

Encompass and Blend now expose REST endpoints that lenders themselves can extend, which was not true even five years ago. Smaller platforms including LendingPad, Calyx Path, and BytePro have shifted to similar architectures. The result is that loan officers spend more time on borrower communication and less on rekeying data from one screen to another. Productivity per loan officer at the top quartile of lenders has moved from roughly 2.5 funded loans per month in 2020 to about 4.8 in late 2025, according to figures from the Mortgage Bankers Association.

The interesting technical question is what gets automated and what does not. Income calculation for W-2 borrowers is fully solved by payroll APIs. Self-employed income still requires judgement because tax returns combine business and personal items in ways that defeat naive parsing. Most lenders run a hybrid model where deterministic rules handle the clean cases and a human underwriter handles the rest. That ratio of automated to manual decisions is the single best leading indicator of where a lender will sit on the cycle-time chart twelve months out.

AI Decisioning, Fair Lending, and the Regulatory Guardrails

Machine learning underwriting models entered the mortgage space cautiously because of fair lending exposure under the Equal Credit Opportunity Act and the Home Mortgage Disclosure Act. The CFPB has been explicit that adverse-action notices must give specific reasons, not generic ones, and that lenders are responsible for the explainability of any model they deploy. That framing has shaped what AI deployment in loan origination systems actually looks like.

In practice, originators have settled on a few patterns. Gradient-boosted trees handle the risk score, and SHAP values drive adverse-action language so borrowers receive specific reasons grounded in the model’s actual logic. Champion-challenger setups let a new model run in shadow mode for months before any live decisioning. Large lenders run the production model through quarterly bias testing against protected classes using methods drawn from the Federal Reserve’s SR 11-7 model risk management guidance, which the OCC adopted alongside its Bulletin 2011-12.

The 2025 update to Regulation B clarified that lenders using AI models still owe a statement-of-reasons disclosure and that the reasons must reflect the actual decision logic. A handful of large nonbank lenders have responded by limiting AI to risk-tiering rather than approve-or-decline calls. This is a defensible posture given the regulatory uncertainty, although it gives up some of the cycle-time gains the technology promises. Expect the legal interpretation to keep shifting through 2026 as more enforcement actions land.

The Vendor Stack: Encompass, Blend, and the Cloud Challengers

The US loan origination market is concentrated. ICE Mortgage Technology, which owns Encompass and integrated Black Knight after the 2023 acquisition, holds roughly 38 percent of US mortgage volume on its platform. Blend dominates the consumer-direct front end, particularly for banks and credit unions that want a polished point-of-sale layer. Smaller vendors like MeridianLink, Calyx, and Symitar’s loan modules serve the credit union and community bank tier.

Switching costs are the dominant force in this market. Migrating live loans, configured workflows, AUS routing, and integrations with title and closing vendors typically takes 9 to 14 months and costs in the low millions of dollars for a mid-sized lender. Lenders who did the work in 2023 and 2024 have started to recover the investment through faster cycle times and lower per-loan cost. Those who delayed are looking at a widening operational gap that capital markets are beginning to price in.

Newer entrants are pitching a cloud-first, API-first story. nCino’s mortgage offering, Stavvy’s eClose-first model, and a handful of smaller vendors have made meaningful inroads with mid-tier credit unions. None has yet displaced Encompass at the top of the market, but the long tail of the industry is fragmenting in ways that will shape vendor dynamics for the rest of the decade.

What 2026 and 2027 Look Like for the Pipeline

The next 18 months of loan origination system development sit at the intersection of three things: deeper AI integration, standardised data formats, and operational consolidation. MISMO v3.6 adoption has reached roughly two-thirds of correspondent flows, which simplifies investor delivery and shortens the gap between funding and sale. URLA changes that went live in 2024 have largely been absorbed by the major platforms, freeing engineering time for non-compliance work.

Large-language-model-assisted document review is the most visible AI application coming to loan origination systems in 2026. Vendors are stitching in models that classify pages, extract numerical values from tax returns and bank statements, and flag inconsistencies for human review. Accuracy on US tax forms 1040, 1099, and W-2 is now high enough to remove most manual classification, although final calculation of qualifying income still routes to a human underwriter for the harder cases.

Lenders thinking about loan origination system strategy in 2026 should keep three questions front of mind. First, which integrations are mission-critical and can the chosen vendor maintain them under load. Second, what is the realistic AI roadmap including bias testing infrastructure and adverse-action language generation. Third, what does the operational workflow look like when half the document review is automated and underwriting capacity becomes a function of model quality rather than headcount. Cycle time will keep falling. The lenders that get to ten-day average mortgage closes by 2027 will be the ones who treated their LOS as a platform rather than a system of record.