A brand manager at a major consumer goods company opens her campaign reporting dashboard on a Wednesday morning and sees something her predecessors never could: the exact number of shoppers who saw her brand’s sponsored listing on a grocery platform and purchased the product within the same session. Not an estimated reach figure, not a modelled attribution score, but verified purchase data from the retailer’s own transaction records. This is the promise that retail media technology has made good on, and it is transforming where advertising budgets flow, who controls premium inventory, and what the AdTech stack of the next decade will look like.

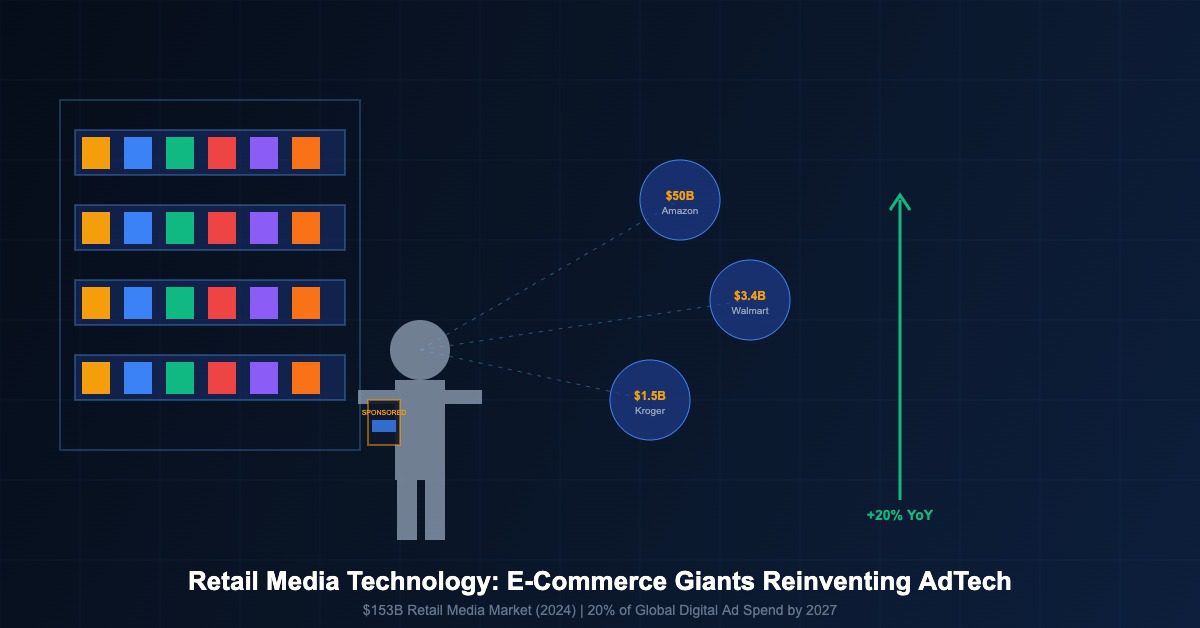

Retail media, defined as advertising sold by retailers within their owned digital properties using their proprietary customer purchase data, has become the fastest-growing category in digital advertising. According to GroupM’s Global Advertising Forecast published in 2024, global retail media revenue reached approximately $153 billion in 2024 and is projected to account for approximately 20 per cent of all digital advertising spend by 2027. That growth trajectory makes retail media the single most significant structural shift in the advertising industry since the emergence of social media advertising in the early 2010s.

The Technology Architecture Behind Retail Media

Retail media networks are not simply advertising sales teams bolted onto e-commerce businesses. The most sophisticated retail media operations represent genuine AdTech platforms in their own right, built on proprietary data infrastructure that gives them measurement and targeting capabilities that no external platform can replicate.

The foundational technology layer is the retailer’s first-party data asset: the accumulated record of customer purchases, browsing behaviour, search queries, and loyalty programme interactions. Amazon’s data asset, built across hundreds of millions of customer transactions spanning two decades, is the most extensive commercial dataset in the world for purchase intent signals. Walmart’s data combines online purchase behaviour with in-store transaction data from its network of more than 4,600 US stores, providing insight into physical shopping behaviour that purely digital platforms cannot access. Kroger’s 84.51 analytics subsidiary has built targeting and measurement infrastructure on the company’s loyalty programme data covering more than 60 million households.

Above the data layer sits the media execution infrastructure: ad serving technology that places sponsored product listings, display placements, and video formats within the retailer’s digital properties; a demand-side platform layer for off-site programmatic activation of retail audiences; and measurement systems that connect ad exposure to verified purchase outcomes through the retailer’s own transaction data. Amazon’s retail media stack is fully vertically integrated: its DSP (Amazon DSP), ad server, and attribution system all operate within Amazon’s ecosystem, measuring against Amazon’s transaction data.

style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;” style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;”

| Retail Media Network | Parent Retailer | Est. Ad Revenue (2024) | Key Data Asset |

|---|---|---|---|

| Amazon Advertising | Amazon | $50 billion+ | Purchase history, search intent |

| Walmart Connect | Walmart | ~$3.4 billion | In-store + online purchase data |

| Kroger Precision Marketing | Kroger | ~$1.5 billion | 84.51 loyalty programme data |

| Target Roundel | Target | ~$1.5 billion | Circle loyalty + store traffic |

| Instacart Ads | Instacart / Maplebear | ~$1 billion | Grocery purchase + delivery data |

| Boots Media Group | Boots / Walgreens Boots | Not disclosed | Advantage Card health data |

Why Retail Media Is Winning Budget from Traditional Digital Channels

The commercial logic driving retail media’s growth is the quality of its measurement proposition. Traditional digital advertising metrics, cost per click, cost per thousand impressions, and even modelled last-click attribution, are increasingly recognised as imperfect proxies for actual commercial outcomes. Retail media networks offer something categorically different: verified purchase attribution grounded in the retailer’s own sales data.

For a fast-moving consumer goods brand running sponsored product campaigns on Kroger Precision Marketing, the measurement output is not a CTR or a viewability percentage but a sales lift figure expressed in actual units sold and incremental revenue generated, measured against a holdout group of similar households that did not see the advertising. This closed-loop attribution model, which the industry refers to as “SKU-level measurement”, gives brand managers a quality of evidence that justifies budget reallocation from traditional media.

According to research published by Boston Consulting Group in 2024, consumer goods companies that allocated more than 15 per cent of their digital advertising budgets to retail media networks reported average return on ad spend figures of 4.2x, compared with 2.8x for the same brands’ non-retail digital advertising. The measurement advantage is translating directly into budget share.

The other driver of retail media budget growth is the deprecation of third-party cookies. As privacy-preserving advertising frameworks restrict the use of cross-site behavioural data for targeting, advertisers are seeking alternative audience data sources with genuine consent and accuracy. Retailer loyalty programme data is first-party data collected with clear consent from customers who actively opt in to exchange their data for discounts and personalised offers. This makes retail audience segments legally robust in a way that third-party cookie-based segments are not.

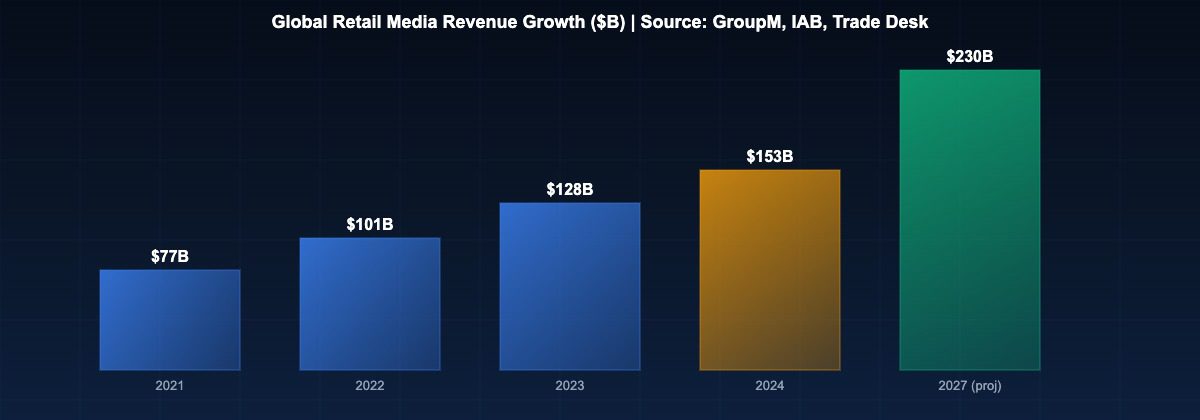

The Retail Media Growth Trajectory

style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;” style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;”

| Year | Global Retail Media Revenue | YoY Growth | % of Digital Ad Market |

|---|---|---|---|

| 2021 | $77 billion | +53% | ~14% |

| 2022 | $101 billion | +31% | ~16% |

| 2023 | $128 billion | +27% | ~19% |

| 2024 | $153 billion (est.) | +20% | ~22% |

| 2027 (forecast) | $230 billion (est.) | Projected ~15% CAGR | ~20% |

The pace of retail media growth has consistently exceeded analyst forecasts. The Trade Desk’s estimate that retail media would account for approximately 20 per cent of global digital advertising by 2027 was considered optimistic when published in 2022 but has been broadly validated by subsequent market data. The IAB’s 2024 Retail Media Measurement Standards report, which represented the first attempt to create consistent measurement methodology across retail media networks, noted that more than 200 distinct retail media networks were operating globally as of 2024, up from approximately 50 in 2020.

The proliferation of retail media networks beyond the US into Europe and Asia-Pacific is accelerating. In the UK, Tesco Media and Insight Platform, Boots Media Group, Sainsbury’s SmartShop, and Asda Media are all competing for consumer goods advertising budgets. In France, Carrefour Links has built a retail media platform that reaches more than 30 million customers across its European retail operations. In Asia-Pacific, Shopee, Lazada, and Coupang have built retail media businesses that are growing rapidly alongside their e-commerce platforms.

How Retail Media Is Reshaping the AdTech Ecosystem

The rise of retail media is not merely creating a new advertising channel: it is restructuring the competitive dynamics of the entire AdTech ecosystem. Several established AdTech categories are being disrupted by retail media’s emergence as a dominant force in digital advertising.

Trade promotion budgets, the money that consumer goods companies historically spent on in-store promotions, end-cap displays, and cooperative advertising with retailers, are being redirected into digital retail media. According to Kantar’s 2024 Brand Strategy Report, more than 35 per cent of traditional trade promotion spend from major consumer goods companies has migrated to retail media networks in the past three years. This represents a genuinely new pool of money entering the digital advertising ecosystem, rather than a reallocation from existing digital channels.

The independent AdTech ecosystem is both threatened and enabled by retail media’s growth. The threat comes from the vertical integration of major retail media networks: Amazon, Walmart, and Kroger all operate proprietary AdTech stacks that bypass the open programmatic ecosystem entirely for their on-site inventory. Every dollar of media spend that flows through a closed retail media network is a dollar that does not flow through independent DSPs, SSPs, or ad exchanges.

The opportunity for independent AdTech lies in the off-site activation component of retail media. When a retailer uses its customer purchase data to target advertising on publisher websites and connected television inventory outside its own properties, that off-site activation typically flows through programmatic infrastructure. The Trade Desk has built direct integrations with multiple retail media networks for exactly this purpose, positioning itself as the independent buy-side infrastructure for off-site retail media activation. Its Kokai platform, launched in 2023, includes dedicated retail data marketplace functionality that allows advertisers to activate retailer first-party data across open programmatic inventory.

The measurement standardisation challenge represents perhaps the biggest unresolved structural issue in retail media. With more than 200 retail media networks each reporting performance using proprietary metrics and methodologies, advertisers managing budgets across multiple networks face significant comparability challenges. The IAB’s Retail Media Measurement Standards, published in 2024 and developed with input from P&G, Unilever, Nestle, and major retailers, represent the first substantive effort to create consistent reporting frameworks. Their adoption will determine whether retail media can scale further into upper-funnel brand advertising, where standardised reach and frequency metrics are essential for media planning.

The e-commerce giants that built retail media have created something that the traditional AdTech industry did not: an advertising model where the data, the inventory, and the measurement are all owned by the same entity, and where the measurement is grounded in commercial outcomes rather than proxy metrics. That structural advantage is what is drawing budget from traditional channels and from the open programmatic ecosystem, and it shows no signs of diminishing as the category continues to grow.

Related reading: AdTech Market Concentration | North America AdTech Leadership | Attribution Technology in AdTech | Programmatic Advertising and RTB

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.