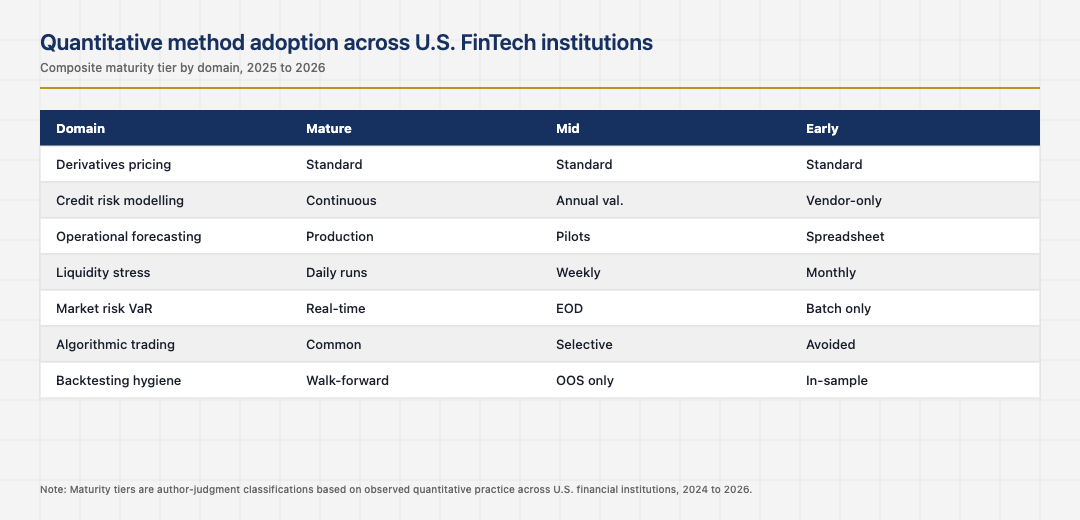

Quantitative methods in U.S. FinTech sit in an awkward zone between the trading-floor quant tradition that produced the modern derivatives industry and the data-science discipline that produced modern AI. The U.S. financial institutions that use quantitative methods well in 2026 borrow from both traditions without confusing them. The institutions that confuse the two usually produce models that look sophisticated and behave unreliably in production.

This piece looks at where quantitative methods are actually delivering value in U.S. FinTech in 2026, the methodological choices that distinguish productive programs, the supervisory considerations that constrain deployment, and the operational realities that determine whether quantitative outputs translate into business outcomes.

The two traditions and the productive intersection

The trading-floor quant tradition emphasises mathematical rigour, theoretical models grounded in stochastic calculus, and careful attention to no-arbitrage conditions. The data-science tradition emphasises empirical methods, model selection through cross-validation, and pragmatic acceptance of black-box methods when they outperform interpretable ones. Both traditions have legitimate strengths.

The productive intersection in U.S. FinTech is using rigorous theoretical models where the structure of the problem supports them and using empirical methods where the structure does not. Pricing of derivatives benefits from the trading-floor tradition. Credit decisioning benefits from the data-science tradition. Operational forecasting benefits from a mix. The institutions that respect this division of labour produce models that work. The institutions that try to apply one tradition universally usually have models that work in their natural domain and fail in others.

Risk modelling and the regulatory capital connection

Risk modelling is where quantitative methods have the most direct connection to U.S. financial regulation. Capital requirements depend on risk-weighted assets, which depend on the risk models used to compute them. The institutions whose risk models satisfy supervisory expectations cleanly hold less capital against equivalent exposure than the institutions whose models do not. The financial value of strong risk modelling is therefore directly measurable in regulatory capital saved.

The discipline that makes risk modelling work is rigorous validation, transparent assumption documentation, conservative treatment of model uncertainty, and continuous monitoring against actual outcomes. The institutions that built this discipline have lower capital costs than the ones that did not. The gap is significant enough to be visible in return-on-equity comparisons across institutions of similar size and business mix.

The operational forecasting use case

Operational forecasting has become a quietly productive use case for quantitative methods in U.S. FinTech. Capacity planning for call centers, staffing for branches, inventory of cash for ATM networks, transaction volume forecasting for payment operations, and demand modelling for product launches all benefit from quantitative forecasting. The methods range from classical time-series approaches like ARIMA and exponential smoothing to modern machine-learning methods like gradient boosting and neural networks adapted for time-series.

The institutions that built operational forecasting capabilities reduce labour costs, improve customer experience through better staffing, and reduce inventory costs in the cash and capital they hold. The benefits are unglamorous and consistent. The institutions that did not build the capabilities often do not know what they are leaving on the table, since the comparison is to a counterfactual they cannot easily measure.

Backtesting discipline and the cherry-picking trap

Backtesting is the most consistently misused tool in quantitative finance. Models that look strong in backtests routinely underperform in production. The pattern is well-documented: implicit data snooping, overfitting to historical idiosyncrasies, ignoring transaction costs and slippage, and selection bias in which strategies are reported. The mature pattern is rigorous out-of-sample validation, walk-forward analysis, and explicit documentation of every model variation tested.

The institutions that respect backtesting discipline produce models that hold up in production. The institutions that treat backtests as confirmation rather than test usually find their production performance disappointing relative to their backtest performance. The cost of backtesting discipline is intellectual honesty and the willingness to discard models that did not actually work. The institutions that built that culture into their quantitative teams compound their advantage over time.

The next phase of quantitative methods in U.S. FinTech

The next phase is shaped by the integration of large language models with quantitative pipelines, the increasing computational capability available for more elaborate models, and the continuing tightening of supervisory expectations around model deployment. The institutions that built strong quantitative foundations in the previous phase will absorb these changes cleanly. The institutions that have not will continue to produce quantitative outputs that their leadership treats with appropriate caution.

Read across the full picture, quantitative methods in U.S. FinTech in 2026 are a mature discipline with specific patterns: respect for the productive intersection of theoretical and empirical traditions, rigorous risk modelling tied to regulatory capital, productive operational forecasting use cases, and backtesting discipline that catches the failure modes before production does. The institutions that respect them deliver real value. The institutions that miss any one usually have quantitative outputs that look sophisticated and behave unreliably.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.