OAuth 2.0 and OpenID Connect have become the convergence point for authentication and authorisation across U.S. financial software. The early period of competing identity protocols and bespoke authentication implementations has largely ended. The remaining design decisions are about how to use OAuth and OIDC well, how to manage the consent and token lifecycle in a regulated environment, and how to integrate the protocols with the broader supervisory expectations that the CFPB’s 1033 final rule has hardened.

This piece looks at where OAuth and OpenID Connect have settled in U.S. finance, the milestones in the protocols’ evolution, the design decisions that distinguish strong implementations from weak ones, and the regulatory environment that is now shaping how the protocols are deployed.

The convergence on OAuth was unevenly fast

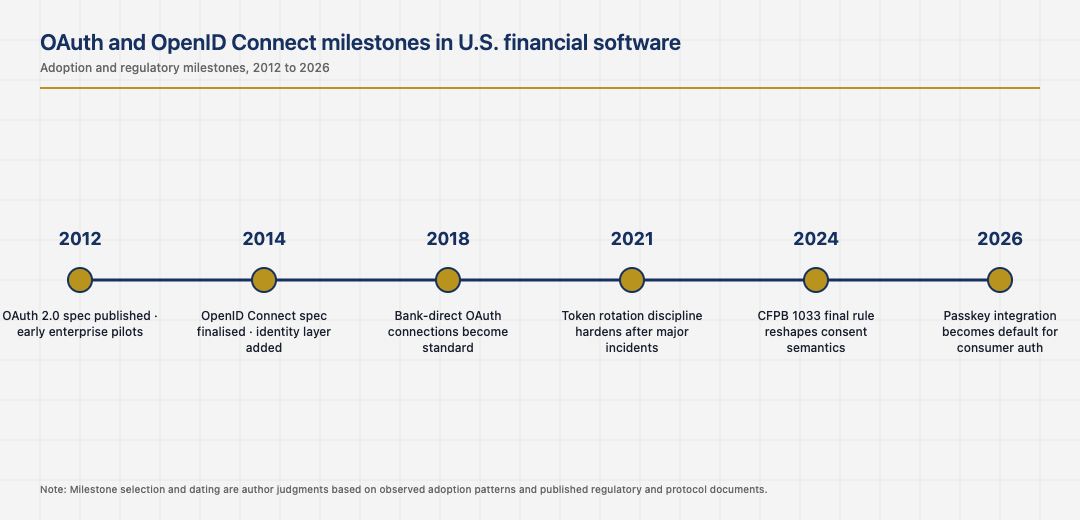

OAuth 2.0 took longer to land in U.S. finance than in adjacent industries. The protocol was published in 2012, but production-grade financial implementations did not become widespread until the late 2010s. The slowness reflected legitimate concerns about consent semantics, token security, and the difficulty of mapping the protocol’s flexibility to the regulated environment that financial institutions live in.

The convergence accelerated as data aggregators standardised on OAuth-based bank connections and the CFPB’s data-rights rulemaking moved toward final form. By the early 2020s, OAuth was the default for any new financial integration. The institutions that adopted it early benefited from the standardisation. The institutions that delayed usually found themselves retrofitting OAuth onto bespoke authentication infrastructure, which was more expensive than greenfield adoption would have been.

Token lifecycle and the rotation discipline

The most important operational discipline in OAuth deployments is token lifecycle management. Access tokens should be short-lived. Refresh tokens should be rotated on every use. Token issuance should be auditable. Token revocation should propagate to consumers within a defined window. The institutions that built token rotation infrastructure into their OAuth deployments have stronger security postures than the institutions that issued long-lived tokens to avoid the operational complexity of rotation.

The cost of token rotation is operational complexity. The benefit is reduced damage from any single token compromise. The institutions that paid the operational cost are reading the cost-benefit tradeoff correctly. The institutions that avoided the cost usually have a small number of credential-compromise incidents per year that better rotation discipline would have contained.

Consent management and the 1033 framework

The CFPB’s 1033 final rule has reshaped consent management for personal financial data in U.S. finance. The rule requires explicit consent, the ability to revoke consent, audit trails of consent changes, and clear specification of what data is being shared and for what purpose. The OAuth consent screen has become the primary surface for these requirements, and the design of that screen now matters as much as the security of the underlying token flow.

The institutions that designed consent screens that genuinely inform users about what data is being shared satisfy the regulatory expectation and produce better customer outcomes. The institutions that designed consent screens to maximise conversion rates regardless of comprehension usually have higher consent volumes and lower defensibility under regulatory scrutiny. The supervisors are increasingly examining consent screen design, and the institutions in the second pattern are now updating their screens under regulatory pressure.

OpenID Connect and the identity layer

OpenID Connect adds an identity layer on top of OAuth, providing standardised identity tokens and user-info endpoints. In U.S. finance, OIDC is increasingly the default for any authentication flow that needs to convey user identity to a relying party. Bank-direct connections, fintech consumer products, and inter-institution federations all benefit from OIDC’s standardisation.

The institutions that adopted OIDC early have cleaner identity flows than the ones that built bespoke identity-conveying mechanisms on top of OAuth. The cleanup work for the institutions that built bespoke mechanisms is ongoing, and the migration to OIDC is one of the quieter modernisation projects across U.S. financial software in 2026. The end state will be more consistent. The migration is expensive in any institution that took the bespoke path.

The next phase of authentication in U.S. finance

The next phase is shaped by passkey adoption, the integration of OAuth with the broader identity ecosystem, and the continuing tightening of supervisory expectations around consent and authentication. The institutions that built mature OAuth and OIDC infrastructure are well-positioned to absorb passkey adoption cleanly. The institutions still struggling with their OAuth deployments will find passkey adoption harder to integrate.

Read across the full picture, OAuth 2.0 and OpenID Connect have settled into U.S. finance as the standard authentication and authorisation framework. The institutions that respect token lifecycle discipline, consent management requirements, OIDC standardisation, and the supervisory environment around all three deliver authentication that holds up across years. The institutions that miss any of these usually have a recurring class of either security incidents or supervisory findings that the missing discipline would have prevented.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.