In a glass-walled trading room on the 22nd floor of a Manhattan office building, a programmatic trader refreshes her dashboard at 9:07 AM. Within the time it takes her coffee to cool, 4.7 million advertising auctions have resolved, each running in under 100 milliseconds, each governed by algorithms assessing hundreds of data signals simultaneously. The inventory being traded spans every major American publisher, social platform, and connected television service. The technology stack powering those auctions, the demand-side platforms, supply-side platforms, data management infrastructure, and attribution systems, is overwhelmingly American in origin, American in operation, and American in revenue. This is not a coincidence. It is the outcome of two decades of deliberate investment, ecosystem building, and regulatory latitude that no other market has replicated at scale.

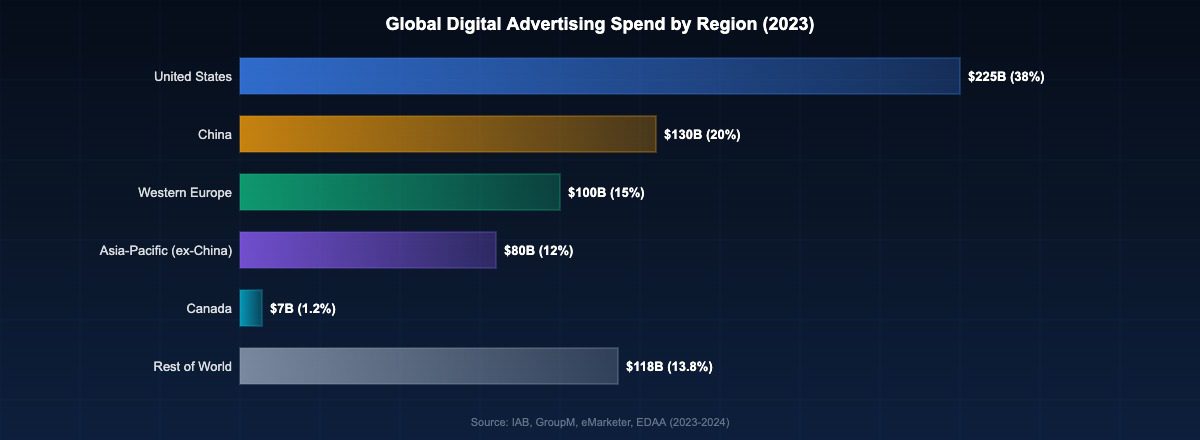

North America, led by the United States, accounts for approximately 38 per cent of global digital advertising spend, according to GroupM’s 2024 global advertising forecast. In absolute terms, the Interactive Advertising Bureau reported total US digital advertising revenue of $225 billion in 2023, a figure that exceeds the combined digital advertising markets of Western Europe and China when measured in US dollars at current exchange rates. Understanding why this dominance exists, and whether it is sustainable, requires examining the structural conditions that created it.

The Origin Story: Why the US Built the Stack First

The United States created the foundational infrastructure of modern programmatic advertising for reasons that were partly technological, partly commercial, and partly regulatory. The commercial internet emerged first at scale in the US, providing the early audience base that justified investment in advertising technology. Google’s 2008 acquisition of DoubleClick, valued at $3.1 billion, established the template for vertical integration across the advertising value chain and triggered a wave of investment into competing infrastructure. The Trade Desk, founded in 2009, Magnite’s predecessor Rubicon Project, founded in 2007, and Index Exchange, founded in 2003, all emerged from this period of US-based ecosystem development.

The venture capital environment in the United States provided funding for AdTech startups at a velocity and scale that no other market matched. According to Crunchbase data, US-based AdTech companies raised more than $4.2 billion in venture funding between 2015 and 2020. The Sand Hill Road funding environment, combined with the density of advertising agency holding companies (WPP, Publicis, IPG, Omnicom, Dentsu all maintain substantial US operations), created a demand-side ecosystem that both needed and could commercially validate new AdTech infrastructure.

Regulatory conditions also played a role that is difficult to overstate. The United States has historically applied a significantly lighter regulatory touch to data collection and use in digital advertising than Europe or Asia. The absence of a federal privacy law equivalent to the EU’s General Data Protection Regulation until very recently allowed US-based AdTech companies to build targeting and measurement capabilities grounded in granular user-level data that European competitors were constrained from replicating. The GDPR, which came into force in May 2018, created an immediate structural advantage for companies that had built their technology and data assets before the regulatory environment tightened in Europe.

Market Size and Competitive Position

style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;” style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;”

| Market / Region | Digital Ad Spend (2023) | % of Global Total | Source |

|---|---|---|---|

| United States | $225 billion | ~38% | IAB / GroupM 2024 |

| China | $130 billion | ~20% | eMarketer 2024 |

| Western Europe | $100 billion | ~15% | EDAA / GroupM |

| Asia-Pacific (ex-China) | $80 billion | ~12% | GroupM 2024 |

| Canada | ~$7 billion (USD) | ~1.2% | IAB Canada 2023 |

| Rest of World | ~$118 billion | ~13.8% | GroupM 2024 |

The US digital advertising market’s scale is not just large in absolute terms, it is large relative to the size of the US economy and population in ways that reflect genuine structural advantages rather than simply demographic weight.

The US accounts for approximately 4.2 per cent of global population but generates 38 per cent of global digital advertising spend. This per capita advertising intensity reflects several factors. American consumers are among the most digitally engaged in the world, with smartphone penetration exceeding 85 per cent and average daily digital media time of approximately 7.4 hours according to eMarketer’s 2024 US Digital Media Usage Report. The US e-commerce market, which drives significant retail media and performance advertising investment, reached $1.1 trillion in 2023 according to the US Census Bureau’s Annual Retail Trade Survey.

The US also leads in connected television advertising, a category that is reshaping the premium video advertising market. US CTV advertising revenue reached approximately $25 billion in 2023 according to the IAB, representing more than half of global CTV advertising spend. The fragmented streaming landscape in the US, with Netflix, Disney+, Hulu, Peacock, Paramount+, and Amazon Prime Video all running advertising-supported tiers simultaneously, has created an unusually dense marketplace for premium video inventory that has driven investment in CTV-specific AdTech infrastructure.

The Technology Companies That Define the Category

style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;” style=”width:100%;border-collapse:collapse;margin:24px 0;font-size:15px;”

| Company | Category | 2023 Ad Revenue | HQ |

|---|---|---|---|

| Alphabet (Google) | Platform + AdTech stack | $237 billion | Mountain View, CA |

| Meta Platforms | Social platform advertising | $135 billion | Menlo Park, CA |

| Amazon Advertising | Retail media + DSP | $50 billion | Seattle, WA |

| The Trade Desk | Independent DSP | $1.95 billion | Ventura, CA |

| Microsoft Advertising | Search + LinkedIn ads | ~$18 billion | Redmond, WA |

| Magnite | Independent SSP / CTV | $613 million | New York, NY |

The infrastructure of US digital advertising dominance is concentrated in a small number of companies of very different types. The platform layer, dominated by Alphabet and Meta, captures the largest share of advertising revenue through owned media environments. The independent AdTech layer, led by The Trade Desk and the demand-side platform market, provides the infrastructure through which advertisers access publisher inventory outside the platform walled gardens. The measurement and verification layer, represented by companies including DoubleVerify, Integral Ad Science, and Nielsen, provides the accountability infrastructure that advertisers require to justify spend.

The Trade Desk’s revenue trajectory illustrates the commercial scale achievable in independent AdTech. From approximately $661 million in revenue in 2020, The Trade Desk grew to approximately $1.95 billion in 2023, a compound annual growth rate of approximately 43 per cent over three years. Its Unified ID 2.0 initiative, which aims to create a privacy-preserving identity framework for the post-cookie environment, is being adopted by publishers and advertisers globally, representing US AdTech infrastructure extending into non-US markets.

Retail media has become the fastest-growing segment of US digital advertising. Amazon Advertising crossed $50 billion in annual revenue in 2024, making Amazon the third-largest digital advertising company in the world by revenue. Walmart Connect, Target’s Roundel, and Kroger Precision Marketing have each built advertising businesses that leverage retail purchase data for closed-loop attribution technology that outperforms traditional digital advertising measurement. This retail media ecosystem is overwhelmingly US-centric in both its development and its commercial scale.

Canada and the North American Context

While the US dominates North American and global digital advertising, Canada occupies a meaningful secondary position within the regional market. The Canadian digital advertising market was estimated at approximately $9.2 billion (CAD) in 2023 according to the Interactive Advertising Bureau of Canada. Canadian digital advertising spend is proportionally high relative to GDP, reflecting the country’s high internet penetration rate of 94 per cent and above-average smartphone adoption.

Canada’s AdTech ecosystem benefits significantly from proximity to US markets and US technology infrastructure. The major US DSPs, SSPs, and measurement platforms all operate in Canada, and Canadian publishers are integrated into the same programmatic trading infrastructure as US publishers. The principal distinction is regulatory: Canada’s Personal Information Protection and Electronic Documents Act (PIPEDA) and Quebec’s Law 25, which introduced GDPR-comparable consent requirements in 2023, have created a more complex data compliance environment for Canadian AdTech operations than exists in most US states.

Mexico and other Latin American markets are increasingly attracting AdTech investment, with eMarketer projecting Latin American digital advertising to grow at approximately 12 per cent annually through 2027, outpacing growth in North America and Europe. However, the infrastructure and technology companies driving that growth remain predominantly US-headquartered, reinforcing rather than challenging US AdTech leadership at the global level.

Structural Risks to US Dominance

US dominance of global digital advertising and AdTech is not guaranteed. Several structural forces are creating competitive pressure that did not exist five years ago.

The Chinese digital advertising ecosystem, dominated by Alibaba, Tencent, Baidu, and ByteDance, has developed entirely separately from the US AdTech stack. ByteDance’s TikTok demonstrated that a non-US company could build a global advertising platform that competes directly with Google and Meta for advertiser budgets. TikTok’s advertising revenue reached an estimated $18 billion globally in 2024, growing at rates that exceed any US platform.

European AdTech companies, while smaller individually than their US counterparts, have built GDPR-compliant infrastructure that positions them to benefit from continued regulatory tightening. Companies including Criteo (French-listed), Azerion (Dutch), and Equativ (French) have built capabilities specifically designed for the privacy-constrained European environment. As US regulators consider federal privacy legislation, European companies may find their compliance infrastructure represents a genuine competitive advantage in the evolving US market.

The concentration of US AdTech within a small number of platforms is also attracting sustained regulatory scrutiny. The DOJ’s antitrust case against Google’s advertising technology business, which proceeded to trial in 2024, could result in structural remedies that alter the competitive dynamics of the US market significantly. A court-mandated separation of Google’s buy-side and sell-side advertising tools would represent the most significant structural change to the US AdTech market since the DoubleClick acquisition in 2008.

US dominance of digital advertising rests on a combination of first-mover advantage, regulatory latitude, capital availability, and the network effects of the world’s most commercially developed digital economy. Those advantages remain substantial, but the forces reshaping the global AdTech market, privacy regulation, platform competition from non-US players, and antitrust enforcement, are all creating conditions in which the margin of US leadership may narrow even if its absolute scale continues to grow.

Related reading: AdTech Market Concentration | AdTech Market Size Estimates | Programmatic Advertising and RTB | Demand-Side Platforms

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.