Return on investment has become the defining question in marketing technology. As MarTech budgets have grown to represent the single largest category of marketing expenditure — accounting for approximately 26 percent of total marketing budget according to Gartner — the pressure on CMOs to demonstrate measurable commercial returns from technology investment has intensified correspondingly. The challenge is not trivial: marketing technology ROI operates across time horizons from immediate conversion improvement to long-term brand equity and customer lifetime value growth, making it inherently multi-dimensional to measure within the $589 billion global MarTech market.

Why MarTech ROI Is Difficult to Measure

The measurement challenge stems from several structural characteristics of marketing technology investment. Much of the value is infrastructural — investing in a Customer Data Platform, a CRM, or a data integration layer does not generate direct revenue but enables other investments to perform better. Additionally, the value of MarTech compounds over time — a marketing automation system improves as more data accumulates and workflows are refined, meaning early ROI calculations often understate long-term value. Marketing attribution — the process of assigning commercial credit to specific activities — adds further complexity, as documented in the analysis of marketing analytics.

Frameworks for Measuring MarTech ROI

Despite these challenges, organisations are developing increasingly rigorous measurement frameworks. The efficiency model measures labour hours, agency costs, or manual process steps eliminated by automation. According to Nucleus Research, marketing automation delivers an average ROI of $5.44 per dollar invested, largely driven by efficiency gains. The revenue contribution model attributes incremental revenue directly to technology-enabled capabilities — for personalisation technology, A/B testing can isolate uplift from personalised versus non-personalised experiences. The total cost of ownership model frames ROI against the full cost including implementation, administration, training, and integration maintenance — particularly important for large enterprise deployments.

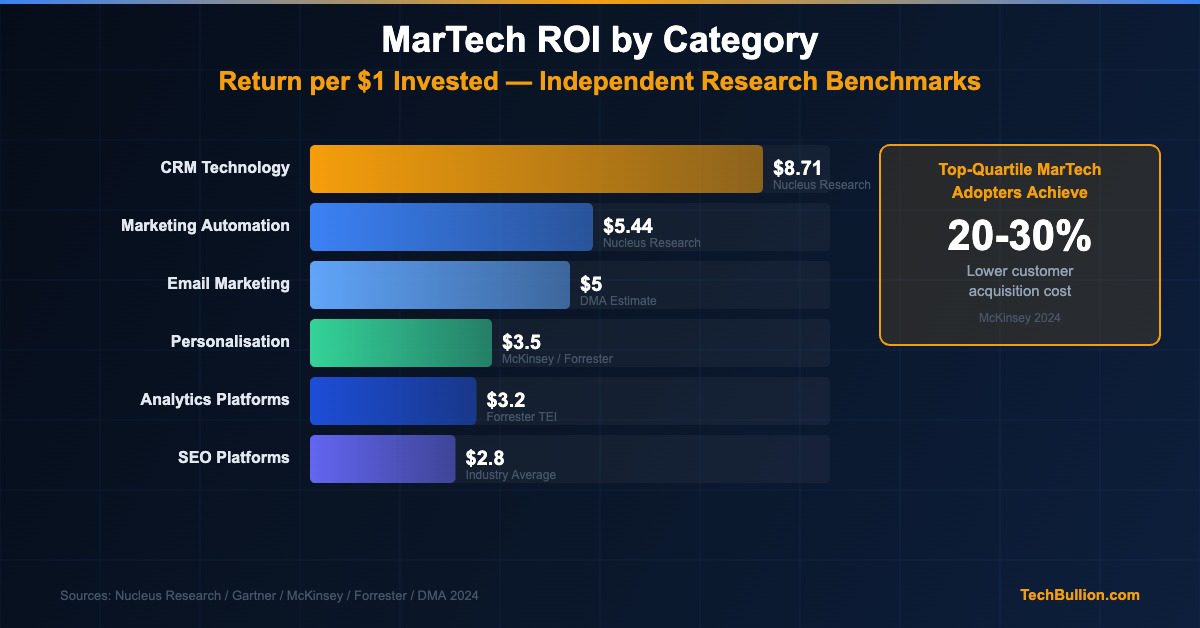

Benchmarks for MarTech ROI by Category

Research from Forrester, Gartner, and technology vendors provides benchmark ROI data for major MarTech categories. CRM technology delivers some of the best-documented returns — Nucleus Research estimates CRM delivers $8.71 return per dollar invested, making it one of the highest-return technology categories in enterprise software. Marketing automation ROI benchmarks cluster around $5 to $8 per dollar invested. CDP investments are harder to benchmark directly but organisations that have implemented them report 15 to 30 percent improvements in campaign conversion rates. Search marketing technology ROI is strongly positive in competitive verticals. For email marketing, the DMA estimates $36 ROI per dollar spent.

The Role of Analytics in Demonstrating ROI

One of the more complex dimensions of MarTech ROI is that demonstrating it requires the same analytics infrastructure that constitutes part of the investment being evaluated. Organisations that have invested in sophisticated measurement capabilities are better positioned to demonstrate the ROI of their broader MarTech stack — creating a virtuous cycle where analytics investment validates the rest of the stack. According to Forrester, companies in the top quartile of MarTech capability maturity outperform peers on customer acquisition cost, customer retention rate, and marketing-sourced revenue.

Building the Internal Business Case

For marketing operations and technology leaders, the most compelling ROI cases combine short-term efficiency evidence with long-term revenue impact projections — baseline metrics before implementation, projected improvements from comparable case studies, a full cost model, a timeline to breakeven, and a sensitivity analysis. The 80 percent of decision-makers expecting budget growth are making this calculation and finding it positive. The trajectory of the MarTech market towards $1.27 trillion by 2031 is the collective result of thousands of organisations concluding that their investment is generating sufficient return to justify continued commitment — and the measurement frameworks evolving within the industry are making that calculation ever more rigorous.

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.

Industry Adoption and Implementation Trends

Adoption patterns across industries reveal significant variation in implementation maturity and strategic priorities. Financial services and healthcare organizations have led enterprise adoption, driven by regulatory requirements and the potential for operational efficiency gains. According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020. Mid-market companies have followed, though their implementations tend to focus on specific pain points rather than comprehensive overhauls.

For more coverage on related topics, explore our dedicated section on technology insights.

Risk Factors and Strategic Considerations

Several factors could moderate the growth trajectory that current projections suggest. Macroeconomic uncertainty, including persistent inflation in key markets and tightening credit conditions, may constrain capital expenditure budgets in the near term. Regulatory fragmentation across jurisdictions creates compliance costs that disproportionately affect smaller operators. Talent shortages in specialized technical roles remain a bottleneck, with demand for qualified professionals exceeding supply by an estimated two-to-one ratio in most developed markets according to PwC’s workforce analysis. Organizations that address these constraints proactively will be better positioned to capture market share.

Industry Adoption and Implementation Trends

Adoption patterns across industries reveal significant variation in implementation maturity and strategic priorities. Financial services and healthcare organizations have led enterprise adoption, driven by regulatory requirements and the potential for operational efficiency gains. According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020. Mid-market companies have followed, though their implementations tend to focus on specific pain points rather than comprehensive overhauls.

Readers interested in this space may also find value in our reporting on AI-powered marketing.

Risk Factors and Strategic Considerations

Several factors could moderate the growth trajectory that current projections suggest. Macroeconomic uncertainty, including persistent inflation in key markets and tightening credit conditions, may constrain capital expenditure budgets in the near term. Regulatory fragmentation across jurisdictions creates compliance costs that disproportionately affect smaller operators. Talent shortages in specialized technical roles remain a bottleneck, with demand for qualified professionals exceeding supply by an estimated two-to-one ratio in most developed markets according to PwC’s workforce analysis. Organizations that address these constraints proactively will be better positioned to capture market share.