The FinTech market has entered a period of turbulence. Despite rapid technological advancement, the sector appears to be entering a phase of consolidation, resulting in more modest investment activity in fintech companies. According to KPMG’s Pulse of Fintech report for the first half of 2024, the year began on a challenging note. While declining investment is largely influenced by rising geopolitical uncertainty and global interest rates, investor preferences reveal a clear focus on certain technologies.

Regtech (Regulatory Technology) and AI and the primary points of interest for investors. To understand their impact on the FinTech industry, we spoke with Dr. Avinash Barnwal, a recognized machine learning expert who has been at the forefront of this technological evolution. Dr. Barnwal has observed the development of Regtech, ML, and AI since their early adoption in corporate fintech, contributing to transformative innovations through advanced ML approaches. His work, including highly cited scientific publications at major peer-review journals and world-famous USA-based conferences, as well as Kaggle competition achievements, has earned recognition across the ML community and major financial corporations.

For the past several years, Dr. Barnwal has led a data team at a leading US-based fintech specializing in financing for small and medium-sized businesses (SMBs). Unlike a traditional corporate leader, he is a passionate data advocate who built the organization’s data function from the ground up. Today, he continues to drive it forward, delivering cutting-edge solutions that shape the future of digital lending.

The Hype Over Regtech and AI

In the first half of 2024, Regtech emerged as the clear standout within the fintech sector, drawing USD 5.3 billion in investment and already surpassing the total raised throughout 2023. This reflects a growing recognition that regulatory technology is not just a compliance tool but a strategic enabler, helping fintechs navigate complex rules with precision and efficiency.

Dr.Barnwal’s comment: ‘Regtech uses technologies like AI, ML, cloud computing, and blockchain to create smarter ways to handle regulatory compliance, risk management, and reporting. In fintech, it helps companies manage complex rules more efficiently and at lower cost, turning time-consuming tasks into automated processes.

In the first half of 2024, several factors have put regtech in the spotlight: changing regulations, more detailed reporting requirements, and an ever-shifting risk landscape. These pressures make it harder for companies to keep up, which is why there’s growing demand for solutions that can simplify and automate key compliance and risk tasks. As a result, regtech is becoming a key area for investment and innovation, with the global market set to grow quickly.’

Alongside this, artificial intelligence continues to captivate investors, particularly in the United States, where machine learning is powering innovations in risk assessment, lending, and payments.

Dr.Barnwal’s comment: ‘AI is clearly a trend that is here to stay. In fintech, there is a growing focus on AI-powered solutions, including emerging applications such as behavioral intelligence. At the same time, traditional uses, like risk scoring, remain as important as ever. RegTech specialists, myself included, are increasingly exploring the potential of generative AI and AI more broadly to enhance efficiency, accuracy, and innovation in compliance and risk management.

For instance, frameworks like LangChain illustrate how generative AI can move beyond simple text generation and become a structured decision-support engine for regtech. By combining large language models (LLMs) with workflow orchestration, memory, and external data tools, these systems can interpret regulatory texts, cross-check them against internal policies, and guide multi-step compliance processes in a controlled way. In practice, this means AI can help automate regulatory monitoring, contextual risk assessments, and reporting obligations while maintaining traceability across steps. Used correctly, such architectures do not replace compliance teams. They augment them, reducing manual workload and enabling faster, more consistent responses to an increasingly complex regulatory environment.’

You can discover more expert details from Dr. Avinash Barnwal in his article, where he precisely deciphers LangChain.

Fintech Penetration to Traditional Banking

Since 2022, SMBs have operated under sustained inflationary pressure and one of the most aggressive monetary tightening cycles in recent decades. Although core inflation that elevated throughout 2023 is projected to moderate across most G20 economies, ongoing geopolitical tensions, volatility in energy markets, and supply chain disruptions continue to create upside risks to prices. In response, central banks have maintained restrictive monetary policies to anchor inflation expectations. The consequence is clear: lending conditions remain tight, credit growth is subdued, and access to affordable financing for SMEs has become increasingly constrained. In this environment, many small businesses are turning to technology-driven financing solutions that can assess risk more dynamically and deliver capital more efficiently, filling gaps left by traditional credit channels.

Dr.Barnwal’s comment: ‘When interest rates remain high and banks tighten their lending standards, small businesses often find it harder not only to afford loans, but to qualify for them. As a result, many turn to fintech lenders that use technology to assess risk in more flexible ways. Instead of relying only on historical financial statements, modern platforms use machine learning to analyse real-time cash flow data, transaction histories, and other digital signals to form a more up-to-date picture of a company’s financial health.

This shift, however, raises important technological challenges. Fintech lenders must securely process large volumes of data, ensure their models remain accurate in changing economic conditions, and provide clear explanations for automated decisions to meet regulatory expectations. Systems must also be scalable and resilient, capable of handling growth without weakening risk controls.

These demands are accelerating innovation. As fintechs continue to improve data infrastructure, risk modelling, and AI-driven compliance tools, they set new standards for speed, transparency, and precision in lending. Over time, this momentum influences the broader banking sector, encouraging traditional institutions to modernise their own technology and strengthen their use of advanced financial tools.’

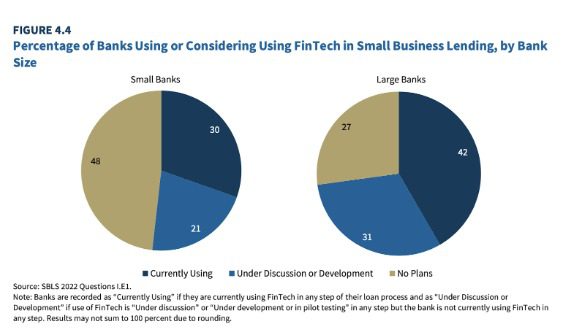

Indeed, according to the Federal Deposit Insurance Corporation (FDIC), banks are relying on financial technology far more than in the past. Around two-thirds of large banks and slightly more than half of small banks either already use financial technology in small and medium-sized business (SMB) lending or are considering adopting it.

At the same time, greater reliance on FinTech introduces new potential challenges. As banks automate underwriting and shift toward data-driven decision models, there is a risk that the relationship-based component of small business lending becomes de-emphasised. Removing human judgement from credit decisions may improve efficiency, but it can also disadvantage small businesses that do not fit standardised data patterns and are better assessed through long-term banking relationships. For relationship-dependent borrowers, the erosion of personalised evaluation may lead to reduced access to credit, even when the underlying business fundamentals are sound.

Dr.Barnwal’s comment: ‘In reality the technology behind modern credit decisioning is far more nuanced than a simple yes-or-no algorithm. Advanced ML models analyse thousands of structured and unstructured data points, including transaction flows, seasonality patterns, revenue volatility, and behavioural signals, to build a multi-dimensional view of a business. This level of analytical depth would be impossible to replicate consistently through manual underwriting alone.

The technological complexity lies not only in the models themselves, but in the infrastructure: secure data pipelines, real-time processing, model monitoring for drift, and explainability layers that ensure transparency and regulatory compliance. When implemented responsibly, these systems do not remove judgment but augment it. They allow lenders to differentiate risk more precisely, identify viable businesses that traditional scorecards might overlook, and deliver decisions faster. In that sense, well-designed fintech infrastructure can expand access to credit rather than restrict it, particularly for SMEs that lack long banking histories but demonstrate strong operational performance in real time.’

The practical impact of this technological approach is measurable. Following a recent update of the risk scoring system led and implemented by Dr. Barnwal, the approval rate was significantly improved without increasing overall portfolio risk. In large-scale SME lending, even a one- or two-percentage-point uplift can translate into thousands of additional businesses gaining access to capital annually, while maintaining stable loss performance.

In data science terms, achieving such an improvement within an already optimised risk framework is highly significant. Mature lending models operate near efficiency frontiers, where incremental gains require substantial advances in feature engineering, model calibration, and validation. An increase therefore reflects not a cosmetic adjustment, but a meaningful enhancement in risk differentiation, enabling the lender to approve more creditworthy applicants who might previously have been declined under less precise models.

Final Word

The evolution of fintech demonstrates how technology is reshaping financial services, particularly in SMB lending. Advanced AI and ML enable lenders to process complex data, automate compliance, and make faster, more accurate credit decisions. As Dr. Avinash Barnwal’s work shows, even incremental improvements, such as an increase in approval rates through updated risk models, reflect the power of sophisticated data-driven systems to expand access to credit. This technological momentum not only addresses the immediate challenges faced by small businesses but also drives innovation across the financial sector, pushing banks and fintechs alike to adopt smarter, more efficient, and highly automated financial technologies.