A single American payroll deposit, $2,500 sent from a Cincinnati employer to an employee in Tampa, can pass through eight separate corporate entities before the worker can use the money. None of those eight will appear on the pay stub. That choreography, repeated billions of times a month, is what people mean when they talk about the US fintech ecosystem working. Federal Reserve Financial Services reported in its 2025 Diary of Consumer Payment Choice that the average US consumer now makes about 44 non-cash payments a month, each one traveling through some version of this hidden chain.

The four layers that make the ecosystem function

The US fintech ecosystem works because four layers exchange data in real time. The first layer is the bank ledger, where customer deposits actually sit. The second is the payment rails: ACH for batch transfers, Fedwire for high-value same-day moves, FedNow and RTP for instant settlement, and Visa, Mastercard, American Express, and Discover for card transactions. The third is the connectivity layer, the aggregators and APIs that let an app read and write to the bank ledger. The fourth is the application layer, the consumer or business-facing software that the customer actually sees.

Each layer has its own performance characteristics. Bank ledgers settle in seconds internally but report externally on delayed cycles. Card networks authorize in milliseconds but settle merchants in 1 to 3 business days. ACH batches process several times per day. FedNow and RTP move funds 24-by-7 in seconds. Aggregator APIs typically respond in under a second for cached data and several seconds for live fetches. The ecosystem works by matching the right rail to the right transaction, then hiding the latency behind a single interface that feels instant to the user.

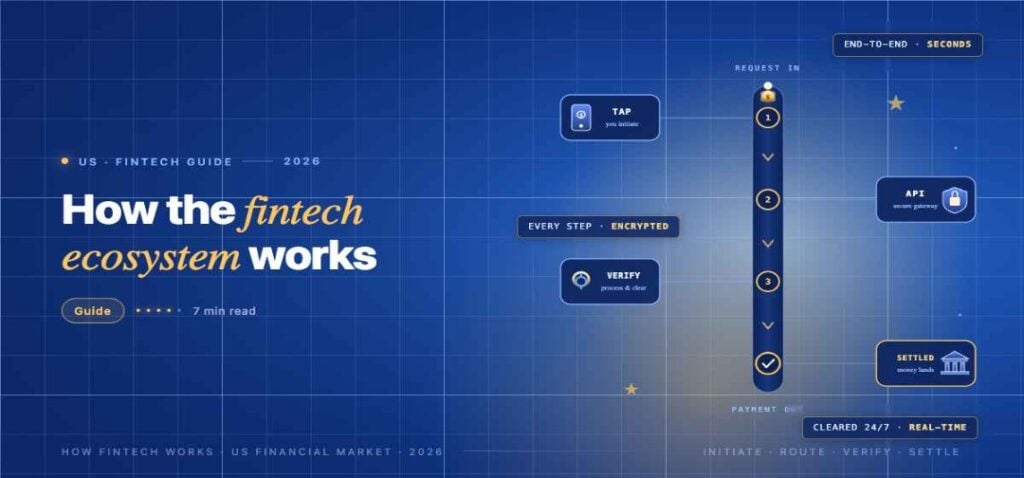

How an app payment actually flows end-to-end

Consider a $50 tap-to-pay purchase at a US coffee shop. The customer holds an iPhone with Apple Pay loaded with a Visa debit card issued by a community bank in Ohio. The customer taps. The phone passes a tokenized card number to the merchant terminal via NFC. The terminal sends the transaction to a payment processor, typically Square, Stripe, or Fiserv, which forwards it to Visa’s network. Visa routes the authorization request to the issuing bank in Ohio. The Ohio bank checks the customer’s available balance, places a hold, and returns an approval. Visa relays the approval to the processor, which signals the terminal to print a receipt. Total elapsed time: about 1.5 seconds.

That is just the authorization. Settlement is a separate dance. At the end of the day, the merchant’s processor batches all approved transactions, sends them to the acquiring bank, which forwards them to Visa, which calculates net positions, debits the issuing bank, and credits the acquiring bank. The merchant typically sees funds in their business account 1 to 3 business days later, minus interchange fees split between Visa, the issuing bank, and the processor. The customer’s $50 hold becomes a posted debit during the same window. The ecosystem works because the customer experience, that 1.5-second tap, does not depend on the settlement timeline.

The role of APIs, aggregators, and open banking

Modern US fintech depends on programmatic data access. Aggregators including Plaid, MX, Finicity, and Akoya sit between thousands of apps and most US bank accounts. They handle three jobs. First, they authenticate the user to the bank using either credentials or a bank-issued OAuth token. Second, they normalize bank data into a standard format so that an investing app or a budgeting tool does not need to write custom parsers for every bank. Third, they cache and serve that data through APIs that downstream apps can call cheaply.

The Consumer Financial Protection Bureau reported that API connections between US financial firms and authorized third parties grew 50 percent in 2024 to roughly 114 million, more than triple the 2022 level. The CFPB’s advanced technology page describes how the new Section 1033 personal financial data rights rule is being phased in across 2026 and 2027, codifying the consumer’s right to share data with any authorized third party. For the ecosystem, the practical effect is that the open-banking pipes that aggregators built informally over the past decade are now backed by federal regulation, which should make the connections more reliable and reduce the share of failed data pulls that today still frustrates many users.

How sponsor banks, BaaS, and embedded finance fit together

Most US consumer-facing fintech apps are not banks. They use a sponsor bank under a model called banking as a service. A typical arrangement looks like this: the fintech holds the customer relationship and the brand. The sponsor bank, often a small community bank like Sutton Bank, Evolve Bank & Trust, or Pathward, holds the actual deposits and owns the federal charter. A middleware provider, sometimes called a BaaS platform, handles the technical integration between the fintech and the sponsor bank.

This model is what makes embedded finance possible. When a shopping site offers a co-branded debit card or a buy-now-pay-later option, the user is interacting with the brand they recognize, but the loan or the deposit is actually originated by a sponsor bank behind the scenes. Plaid’s 2026 fintech trends report describes how this model continues to expand into vertical sectors such as healthcare billing, freight payments, and creator-economy platforms. The economics are appealing: the fintech captures the customer relationship and the data, the sponsor bank earns sponsorship fees and deposit float, and the consumer gets a more convenient interface than a traditional bank app.

Where the ecosystem breaks, and how it gets fixed

The ecosystem works most of the time, but the failure modes are instructive. When the BaaS intermediary Synapse collapsed in 2024, tens of thousands of US consumers lost access to their app balances for months. The reason was that the reconciliation between the fintech, Synapse, and the underlying sponsor banks had broken down, and FDIC insurance pass-through could not be applied to balances that could not be reliably attributed to specific customers. The episode prompted federal regulators to issue new guidance on BaaS relationships and to push for clearer record-keeping standards.

Other breakdowns are less dramatic but more common. Aggregator outages can take down a dozen apps at once. Card network slowdowns can leave merchants unable to accept payment during peak shopping hours. FedNow and RTP, while highly reliable, are limited by financial institution participation, and not every bank is yet a member. Even routine ACH disputes can take weeks to resolve. The ecosystem fixes these gaps slowly, through bilateral API agreements that replace fragile credential sharing, through better fraud signals shared across processors, through stricter sponsor-bank oversight, and through the gradual buildout of real-time rails. None of those fixes happens overnight, which is why the US fintech ecosystem in 2026 is best understood not as a finished system but as a continuously improving substrate underneath everyday American financial life.