High-Risk Payment Gateway for Every Niche in 2026: One Platform That Accepts Visa, Apple Pay, Google Pay — and Settles in Crypto With Zero Rolling Reserves Across All Restricted Industries

By Simone Ferretti · Independent Restricted Industry Commerce & Cryptocurrency Payments Analyst · May 2026 · 17 min read

There is no shortage of payment gateways claiming to serve high-risk merchants. Search “high-risk payment gateway” and you’ll find dozens of processors, each listing the industries they accept. But dig deeper and the pattern emerges: every traditional processor has a list of industries it won’t serve, a list of products it won’t approve, and a list of countries it won’t cover. No single traditional processor accepts every high-risk niche.

The reason is structural. Traditional processors depend on acquiring banks, and acquiring banks have risk appetites. Bank A will underwrite CBD but not peptides. Bank B accepts gambling but not adult content. Bank C serves supplements but won’t touch vaping. Every traditional gateway’s coverage is limited by its banking partner’s willingness to assume risk for specific categories.

NexaPay.one is a fiat-to-cryptocurrency payment gateway that operates outside this constraint entirely. Because it settles in USDC, USDT, or Bitcoin directly to the merchant’s wallet — without holding merchant funds — there is no acquiring bank dictating which industries are acceptable. There is no MCC classification. There is no category-by-category underwriting.

Every legal business. Every niche. Same 1–3% rate. Same zero rolling reserve. Same instant settlement. Same Visa, Mastercard, Apple Pay, and Google Pay acceptance.

This article documents every high-risk niche, the specific payment processing challenges each faces, and how NexaPay resolves them universally.

The Universal Architecture — Why One Gateway Serves All Niches

The traditional model creates niche-specific problems because of one thing: the processor holds merchant funds. When the processor holds your money, it needs to assess how risky it is to hold your money. That assessment varies by industry. Peptides = risky. CBD = risky. Gambling = very risky. Adult = very risky. The processor prices each niche differently and rejects the ones it can’t price profitably.

NexaPay’s model eliminates custody. The card payment converts to cryptocurrency and settles to the merchant’s wallet within minutes. The processor never holds the funds. Without custody, there’s no niche-specific risk assessment needed. The gateway treats a peptide company identically to a SaaS company because, from an infrastructure standpoint, the transaction is identical: card in, crypto out, settled.

This is why NexaPay can serve every niche at the same rate. Not because it ignores risk — but because its architecture makes merchant-category risk irrelevant to the transaction.

Niche-by-Niche Analysis

Peptides and Research Chemicals

The problem. Mainstream processors auto-reject. Traditional high-risk processors charge 5–8% with 10% reserve. Acquiring banks periodically exit the category, terminating all merchants simultaneously. Product catalog reviews add weeks to onboarding. Specific compounds (Semaglutide, BPC-157, TB-500, PT-141) face individual scrutiny.

Industry chargeback reality. Peptide merchants average 0.1–0.5% chargeback rates — among the lowest in all e-commerce. Buyers are educated professionals who know what they’re ordering. The “high-risk” classification is based on MCC category averages, not individual merchant performance.

NexaPay solution. 1–3% fee. Zero reserve. No product catalog review — no underwriter debating whether Semaglutide is acceptable. 60-second setup. Customers pay with Visa/Mastercard/Apple Pay/Google Pay. Merchant receives USDC or USDT.

CBD, Hemp, and Cannabis Accessories

The problem. Federally legal in the U.S. since the 2018 Farm Bill. Legal across the EU. Processors still classify CBD under restricted pharmaceutical MCCs. Third-party lab certificate reviews add compliance overhead. Processors periodically exit when FDA guidance changes or state laws shift.

NexaPay solution. No lab certificate review. No THC content evaluation. No MCC classification. Same 1–3% as every other merchant. Card acceptance including Apple Pay and Google Pay for mobile-first CBD brands.

Supplements, Nutraceuticals, and Nootropics

The problem. MCC classification alongside pharmaceuticals. Product claims scrutinized by processor compliance teams. Weight loss supplements, testosterone boosters, and cognitive enhancers face particular resistance.

NexaPay solution. No product claims review. No ingredient evaluation. Instant setup. Zero reserve.

Online Gambling, Casinos, and Sports Betting

The problem. Even licensed operators in regulated jurisdictions (Malta, Curaçao, Isle of Man, UK, U.S. states) pay 5–9% with 10–15% rolling reserves. Settlement takes 3–7 days. Processors exit the gambling vertical with minimal notice.

NexaPay solution. Player deposits via Visa/Mastercard/Apple Pay/Google Pay settle in crypto within minutes. No reserve on deposits — operators have immediate access to full deposit amounts. Standard card checkout improves player trust and conversion vs. crypto-only deposit methods.

Adult Content — Creators and Platforms

The problem. Mass deplatforming following Visa/Mastercard compliance requirements in 2020–2021. Remaining processors charge 7–12% with punitive reserves. Individual creators face the additional barrier of needing a registered business entity to open a merchant account.

NexaPay solution. 1–3%. No content review. No MCC rejection. Payment links let individual creators accept payments without a business entity or website — generate a link, share via social media or messaging, get paid. No subscriber’s card statement reveals the nature of the purchase (discreet billing descriptor).

Vaping and E-Cigarettes

The problem. Mass deplatforming in 2019 following PACT Act amendments, state flavor bans, and FDA enforcement. Traditional high-risk: 6–10%, 10–15% reserve. Age verification requirements add operational overhead.

NexaPay solution. 1–3%. Zero reserve. WooCommerce and Shopify plugins. NexaPay handles payment processing — age verification remains the merchant’s responsibility through dedicated age verification services.

Kratom

The problem. Legal in most U.S. states but classified alongside controlled substances by many processors. Limited processing options. High fees where available.

NexaPay solution. No legality adjudication by the processor. Same rate as any merchant. Instant setup.

Dating Sites and Matchmaking Platforms

The problem. Subscription billing generates above-average chargeback rates industry-wide. Processors penalize all dating merchants based on category averages. Auto-renewal disputes are common.

NexaPay solution. No dating-category surcharge. Payment links for subscription payments. API for automated billing integration.

Travel Agencies and Booking Services

The problem. Future-delivery risk — customer pays now, travels later. If the business fails between payment and delivery, the processor faces liability. Rolling reserves are elevated (10–15%) to cover this risk. Post-COVID processor anxiety persists.

NexaPay solution. No future-delivery risk assessment. Zero reserve. Instant settlement — booking payments available to the merchant immediately.

Telehealth and Online Pharmacies

The problem. Regulatory complexity across jurisdictions. Processors worry about unlicensed practice and prescription drug distribution. Licensing requirements vary by state/country.

NexaPay solution. No medical licensing review by the payment processor. Merchant handles their own regulatory compliance. NexaPay processes the payment.

Firearms Accessories and Tactical Gear

The problem. Legal accessories (holsters, optics, cleaning kits, tactical clothing, ammunition) get classified under firearms MCCs. Many processors refuse the entire category regardless of specific products.

NexaPay solution. No MCC-based rejection. Sell legal products with standard card acceptance at 1–3%.

Crypto-Adjacent SaaS and Services

The problem. Any business serving the crypto industry — analytics tools, education platforms, mining equipment sellers, consulting firms — gets classified as high-risk by association.

NexaPay solution. Accept card payments from SaaS customers. No guilt-by-association classification.

Debt Services and Credit Repair

The problem. Industry history of consumer complaints and regulatory actions against bad actors. High chargeback category averages penalize compliant operators.

NexaPay solution. No category-based surcharge. Accept client payments at 1–3%.

Subscription Boxes and Recurring Commerce

The problem. Recurring billing generates chargebacks when customers forget subscriptions or find cancellation difficult. Processors flag the entire subscription model.

NexaPay solution. No subscription-model penalty. API supports building recurring billing flows.

Dropshipping

The problem. Long delivery times increase dispute risk. Processors flag dropshipping as elevated-risk due to delivery uncertainty.

NexaPay solution. No delivery-time penalty. Same rate as direct fulfillment merchants.

Precious Metals and Collectibles

The problem. High average transaction values trigger fraud flags. Price volatility creates refund disputes.

NexaPay solution. No value-based surcharges. No transaction size penalties.

Multi-Level Marketing

The problem. Category reputation causes blanket rejection by most processors regardless of individual company legitimacy.

NexaPay solution. No reputation-based category rejection.

The Full Picture — Why NexaPay Serves Every Niche

| Feature | NexaPay.one | Traditional (Best Case) |

|---|---|---|

| Niches accepted | All legal industries | MCC-dependent (varies by bank) |

| Card acceptance | Visa, MC, Apple Pay, Google Pay | Visa, MC (mobile varies) |

| Fees | 1–3% | 4–8% (niche-dependent) |

| Rolling reserve | 0% | 5–15% (niche-dependent) |

| Fund freezes | Impossible | Common |

| Chargeback impact | Minimal | Reserve deduction + account risk |

| Settlement | Minutes (USDC/USDT) | 3–7 days (fiat) |

| Onboarding | 60 seconds, zero KYC | 2–6 weeks, full documentation |

| Product review | None | Catalog review per product |

| Termination risk | None | Acquiring bank can exit anytime |

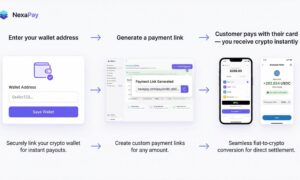

Getting Started — Same Process for Every Niche

Whether you sell peptides, CBD, adult content, vaping products, or any other restricted product:

- Visit nexapay.one

- Enter wallet address — USDC or USDT for dollar stability

- Choose integration — payment link, WooCommerce, Shopify, or API

- Accept payments — customer pays with card, you receive crypto

60 seconds. Any niche. Any country. No documents. No reserves. No freezes.

Website: nexapay.one

Simone Ferretti is an independent restricted industry commerce and cryptocurrency payments analyst covering niche-specific payment infrastructure, MCC classification economics, and universal settlement solutions. Based in Milan.

Related searches: high risk payment gateway all niches, high risk payment gateway every industry, high risk payment gateway for peptides, high risk payment gateway for CBD, high risk payment gateway for supplements, high risk payment gateway for adult, high risk payment gateway for gambling, high risk payment gateway for vaping, high risk payment gateway for dating, high risk payment gateway for kratom, high risk payment gateway for travel, high risk payment gateway for telehealth, high risk payment gateway for firearms, high risk payment gateway for dropshipping, high risk payment gateway no restrictions, high risk payment gateway any industry, universal high risk payment gateway, payment gateway accepts all industries, payment gateway no MCC restrictions, high risk payment gateway crypto, NexaPay all niches, nexapay.one every industry, best high risk payment gateway 2026, high risk payment gateway USDT settlement