Quantum computing has had a noisy three years in finance. The promise of qualitatively faster Monte Carlo simulations, qualitatively better portfolio optimisation, and qualitatively new cryptography has driven steady spending and a steady stream of vendor announcements. The reality at the start of 2026 is more measured. No US bank is running a quantum algorithm in a way that meaningfully changes a production decision. Several US banks have published quantum research, run hardware partnerships, and started serious post-quantum cryptography migrations. The interesting story is what banks are actually doing rather than what the press releases imply.

Where Quantum Hardware Actually Sits in 2026

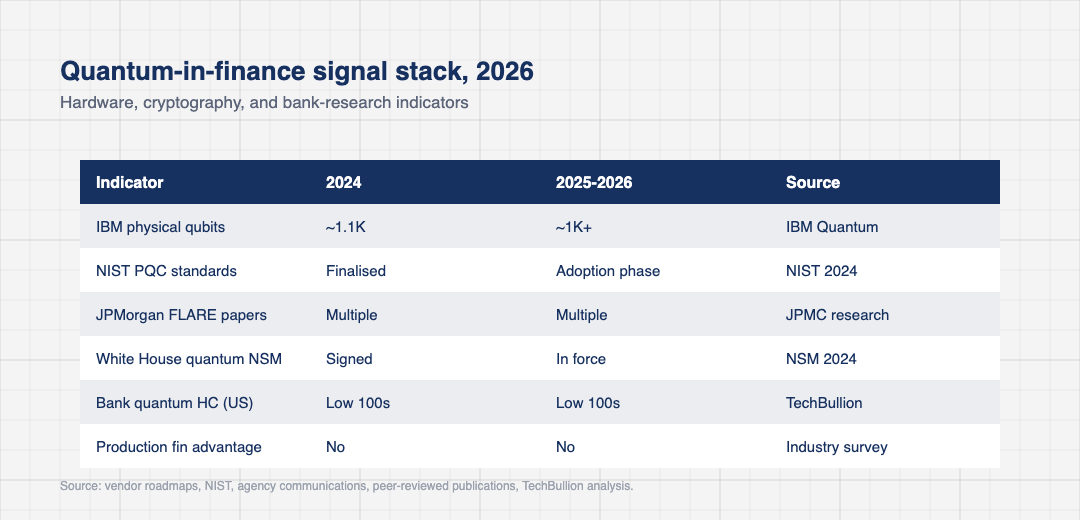

The hardware landscape has matured in concrete ways. IBM’s quantum stack has crossed the 1,000-qubit threshold with the Condor and Heron generations, with quantum volume and error rates improving but still far short of fault tolerance. Google, IonQ, Quantinuum, PsiQuantum, and Rigetti each have credible roadmaps and meaningful capital. None of them is yet running a financial calculation that a classical supercomputer cannot run faster or more accurately. The phrase “quantum advantage in finance” remains aspirational at the level of production decisions.

The progress that has been made is real but narrow. Quantum hardware has improved on coherence times, gate fidelity, and error-mitigation techniques. Error-corrected logical qubits, the precondition for truly fault-tolerant quantum computing, remain experimental. Most quantum-classical hybrid algorithms that banks have published, including various variational quantum eigensolver approaches to portfolio optimisation, deliver results that are interesting as research and not yet better than well-tuned classical methods at the relevant problem scales.

What this means for finance is that quantum is an investment in optionality rather than a current capability. Banks that have built quantum teams in 2024 and 2025 are positioning for a window that most credible technical observers place somewhere between 2028 and 2035, with the wider error bars tilted toward the later end of that range. The exact timing is uncertain enough that being patient is rational. Being absent is more expensive than the headline cost suggests, because the relevant skills take years to build and the hardware partnerships that matter most are negotiated long before any specific application is ready to ship.

What US Banks Are Actually Doing With Quantum Today

JPMorgan Chase has the most visible quantum research effort among US banks. The Future Lab for Applied Research and Engineering, often referred to as FLARE, has produced peer-reviewed papers on quantum approaches to derivatives pricing, portfolio optimisation, and Monte Carlo acceleration. JPMorgan has been explicit that these are research-stage explorations, not production deployments. The bank has hardware partnerships with multiple vendors and treats this as a long-horizon capability investment.

Goldman Sachs has invested in research at the intersection of quantum and risk pricing, with academic collaborations and internal teams. Wells Fargo, BNY Mellon, and Citi have all published smaller research efforts. The pattern across the largest US banks is similar: a small dedicated research team, multiple hardware partnerships to avoid vendor lock-in, and a careful narrative that does not overpromise. The teams are typically in the dozens of people rather than the hundreds.

The use cases that have attracted the most genuine effort are option pricing for exotic derivatives, where Monte Carlo runtimes can be material, and portfolio optimisation, where combinatorial problems become intractable at large scale. Both are areas where a real quantum advantage would matter to a bank’s P&L. Both are also areas where classical algorithms continue to improve, which keeps moving the goalposts for what quantum needs to deliver to be worth deploying.

The Post-Quantum Cryptography Migration Is the Near-Term Story

The more immediate quantum-related work in US finance has nothing to do with running quantum algorithms. It has to do with preparing for the day a future quantum computer could break the public-key cryptography that protects existing financial systems. NIST finalised its first post-quantum cryptographic standards in August 2024 with ML-KEM, ML-DSA, and SLH-DSA. Federal agencies and major financial institutions have been actively planning migrations ever since.

The Federal Reserve, the OCC, and the FDIC have all included post-quantum cryptography readiness in supervisory communications. NSM-10, the May 2022 White House National Security Memorandum on promoting US leadership in quantum computing while mitigating risks to vulnerable cryptographic systems, and subsequent agency guidance have made it clear that critical infrastructure operators, including the largest US banks, are expected to inventory cryptographic dependencies and plan crypto-agile transitions.

The migration is going to take years. A typical large US bank has thousands of applications, hundreds of HSM-protected key stores, and a dense web of vendor and counterparty integrations that each use one or more cryptographic protocols. Switching from RSA and ECC to ML-KEM and ML-DSA is not a single project; it is a programme that touches network protocols, application libraries, hardware tokens, and operational procedures. Banks that started inventorying their cryptography in 2023 are now well into hybrid deployments that run both classical and post-quantum algorithms. The slower banks are getting started in 2025 and 2026, which is later than the guidance suggested.

Where the Money and the Talent Have Actually Gone

Quantum-in-finance is the kind of investment where the talent is more important than the hardware spend. The largest banks have been recruiting quantum physicists and applied mathematicians since roughly 2020. The market for those people is small and the compensation has reached the level where banks compete directly with quantum hardware vendors for hires. JPMorgan’s FLARE team, the largest by public count, is in the high tens of people. Goldman’s effort is smaller but well-resourced. Across all of US finance the quantum-research headcount is probably in the low hundreds.

The hardware spend through cloud-based quantum providers is meaningful but not eye-watering. Amazon Braket, IBM Quantum, Azure Quantum, and direct vendor partnerships with IonQ and Quantinuum have brought quantum compute within reach of any bank with research interest. The bills are large enough to require executive sign-off but small enough that they sit inside the broader research budget. The real cost of a bank quantum programme is people, not silicon.

External partnerships have become the standard model. Banks tend to maintain three or four vendor relationships, run hardware-agnostic research where possible, and let the vendors compete for the privilege of demonstrating their hardware on the bank’s problems. The model keeps optionality open and gives the bank a credible position to use whichever hardware path matures first. The asymmetric nature of the technology, where one architecture might suddenly cross a threshold and the others fall behind, makes diversification rational.

What 2026 and 2027 Hold for Quantum Computing in Finance

Three currents will shape the next 18 months. The first is steady hardware progress that is unlikely to produce a finance-relevant quantum advantage but will narrow the gap. Error-corrected logical qubits in small numbers will start to be demonstrated, and the credibility of the longer-term roadmaps will firm up. The financial-services demand for these milestones will be patient but persistent.

The second current is the practical work of post-quantum cryptography migration. Federal expectations have set a floor on the timeline, and large banks will keep transitioning their cryptographic infrastructure. The cost will be material and the work mostly invisible to customers. The banks that get this right will avoid a future surprise; the ones that delay will be exposed when quantum hardware does eventually mature.

The third current is the slow build of quantum-ready software platforms. Vendors including Classiq, Zapata, and the cloud providers are racing to produce abstractions that let financial developers express problems once and target multiple quantum back-ends. The maturity of this layer is what will determine whether quantum, when it finally crosses the threshold, can be adopted by finance teams who are not quantum physicists. By 2027 the answer to whether quantum in finance is a real thing or a long-running hype cycle will be clearer. Today it remains both an investment in optionality and a discipline in distinguishing useful research from useful theatre.