On the morning of a CPI release in February 2026, three US hedge funds with no public connection between them placed nearly identical interest-rate trades within thirty seconds of the data hitting the wire. They did not see the print before the rest of the market. They had simply trained their language models to read the press release the moment it was published, score the sentiment, and convert the result into a position. According to a Coalition Greenwich buy-side technology survey released this year, more than 70 percent of US quantitative trading firms now run sentiment analysis for markets as a routine input alongside their traditional factor models, up from a third in 2021. The discipline is no longer a research project. It sits inside the execution stack at most major US trading floors, and the dollar volume influenced by it is large enough to matter to the rest of the market. The technology behind these signals has compressed dramatically. What once required a dedicated team of natural-language engineers to maintain has become a vendor product purchased by even smaller hedge funds, and the gap between buy-side and sell-side capabilities on this dimension has narrowed sharply.

From bag-of-words to large language models

The earliest sentiment models in finance were word-list scorers built in the 2000s. A piece of text was tokenised, each word checked against a positive or negative dictionary, and the score reported as a single number. Those models worked at a coarse level but missed sarcasm, context, and the precise wording that most often moves a stock. The shift began in the late 2010s with transformer architectures, and accelerated in 2023 when fine-tuned variants of large language models could read an entire earnings call transcript and produce a sentiment score that correlated meaningfully with subsequent price action. By 2025, several US quant firms were running internal models with billions of parameters specifically tuned to financial text, and the major data vendors, including Bloomberg, FactSet, and Refinitiv, had all launched paid sentiment feeds that customers could plug into their order management systems. The same architectural pattern shows up in large language models in finance, where the model investments often serve more than one workflow at the same firm.

Where the signals come from

US trading desks pull sentiment from five primary sources. Earnings calls account for the largest share at 34 percent, because the market reaction to a single executive comment can be measurable in real time. News wires, primarily Bloomberg, Reuters, and Dow Jones, supply 24 percent. SEC filings, including 8-Ks and 10-Q risk factors, contribute 18 percent. Social media, mostly StockTwits and a curated subset of public posting platforms, accounts for 14 percent. Analyst reports round out the mix at 10 percent, with most of the weight on tone changes rather than recommendation upgrades. Different desks emphasise different sources. Equity long-short funds tend to rely heavily on earnings calls, while fixed-income funds lean on Federal Reserve communications and Treasury auction commentary, and macro funds blend across all five categories with model weights tuned to the trading horizon they care most about.

The mix has shifted toward earnings calls and filings over the last three years, and away from social media. The reason is precision. A sentiment signal pulled from a CFO answering a specific question on guidance is more actionable than the same signal pulled from a thousand retail posts. Funds discovered, sometimes painfully, that crowd sentiment can be noisy or coordinated, and the operational cost of cleaning it is higher than the alpha it produces in most market regimes. The same pattern surfaces in adjacent machine learning in finance work, where data quality and source reliability have become the binding constraint on model usefulness rather than raw model size.

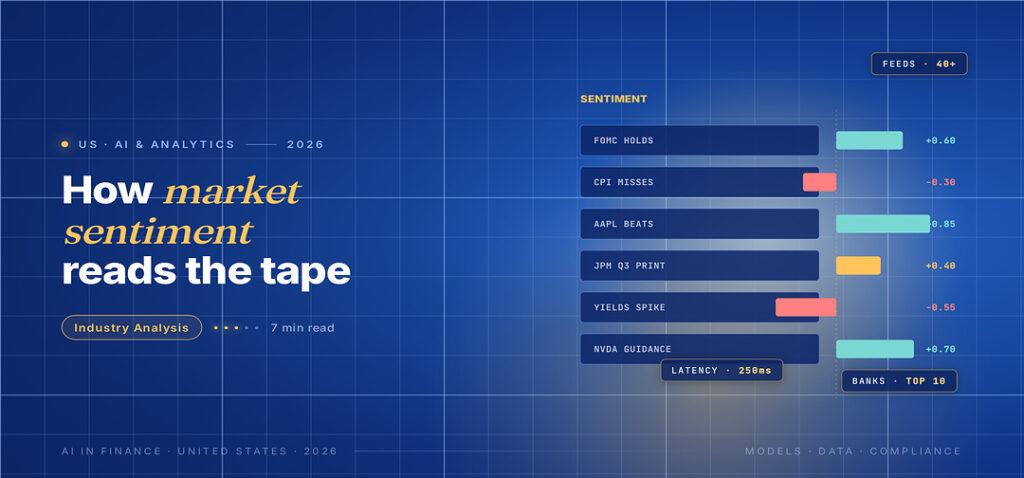

Latency, infrastructure, and the speed game

The sentiment edge is mostly a latency game. A model that scores an earnings call thirty seconds after the call ends is competing with a market that has already moved. The fastest US quant desks now run inference within four seconds of receiving the source text, with the bottleneck typically sitting in network hops between the data vendor, the model server, and the order management system. Banks and large quant funds have responded with co-location, dedicated GPU clusters, and direct vendor feeds that bypass slower public news APIs. The arms race has produced a measurable cost increase. Sentiment infrastructure spending across US trading firms grew at more than 20 percent annually in 2024 and 2025, faster than overall trading technology spend, with co-location fees and dedicated GPU contracts driving a sizable share of the increase. The smaller funds without the budget for that infrastructure are increasingly buying packaged sentiment signals from vendors, accepting a small latency penalty in exchange for cost predictability and faster onboarding into their existing risk and compliance workflows.

Compliance and the regulatory bar

The compliance picture is sharper than most outside the industry assume. The SEC has signaled that AI-driven trading falls under existing investment-adviser rules, including the obligation to test and document any model that influences trade decisions. Funds running sentiment models are now expected to maintain validation logs, error analyses, and bias assessments, and to be ready to produce them in an exam. The Commodity Futures Trading Commission has taken a similar stance for futures markets. The bar is high enough that the largest US quant funds now employ teams of model risk managers whose sole job is to certify and continuously monitor sentiment and other AI-driven signals before they reach the trade desk, and the same teams now report directly into chief risk officers rather than into research. Enforcement actions in this area have been limited so far, but the regulatory expectation has been clear since 2024 and is expected to intensify through 2026 as the SEC moves into a more active examination phase on AI usage at investment advisers.

What the next twelve months are likely to change

Three things are likely to shift through the rest of the year. First, multimodal models that read text alongside the audio of earnings calls and the visual content of executive presentations are moving from research into limited production at several US firms. The early evidence suggests the audio component, including subtle changes in vocal tone or hesitation patterns from corporate executives, adds a meaningful incremental signal beyond text alone, particularly during quarterly Q&A sessions when prepared remarks are no longer in play. Second, the data vendors will continue to bundle sentiment with their core feeds, gradually compressing the price premium for premium analysis. Third, broader regulatory expectations on model documentation will tighten, particularly for funds running sentiment models on retail-investor-facing products, where the consumer protection bar is higher. None of these alone displaces traditional alpha sources. Together, they make sentiment analysis for markets a routine line item in the technology budget rather than the experimental category it was even three years ago. Wider real-time data infrastructure trends show why the sentiment workflow is increasingly hard to separate from the rest of the modern trading stack.

A trader at a US quant fund in 2015 who said her edge came from reading earnings calls in real time would have been seen as either understating a much more sophisticated process or overstating an inherently slow one. In 2026 the same answer is the literal description of how a meaningful share of US trading volume is now influenced, and the question for fund managers is no longer whether to use these signals but how to combine them with the rest of their factor stack without creating spurious correlations. Sentiment analysis for markets has become routine, and the funds that ignored it through the 2020s are mostly the ones that have struggled to keep up with peers, with several large traditional managers now disclosing dedicated AI investment programmes in their annual filings.