Smart contracts in U.S. financial use have moved past the early-cycle exuberance and into a more constrained but more durable position. The technology has clear use cases where deterministic on-chain execution provides genuine value, and clear limits where the rigidity of code-only execution creates problems that traditional contracts handle better. The U.S. institutions deploying smart contracts in 2026 generally understand this division. The institutions still pitching smart contracts as a universal disintermediation tool generally do not.

This piece looks at where smart contracts in U.S. finance have settled in 2026, the use cases that have proven productive, the structural limits of code-only execution, and the regulatory environment that increasingly shapes deployment.

The use cases that have proven productive

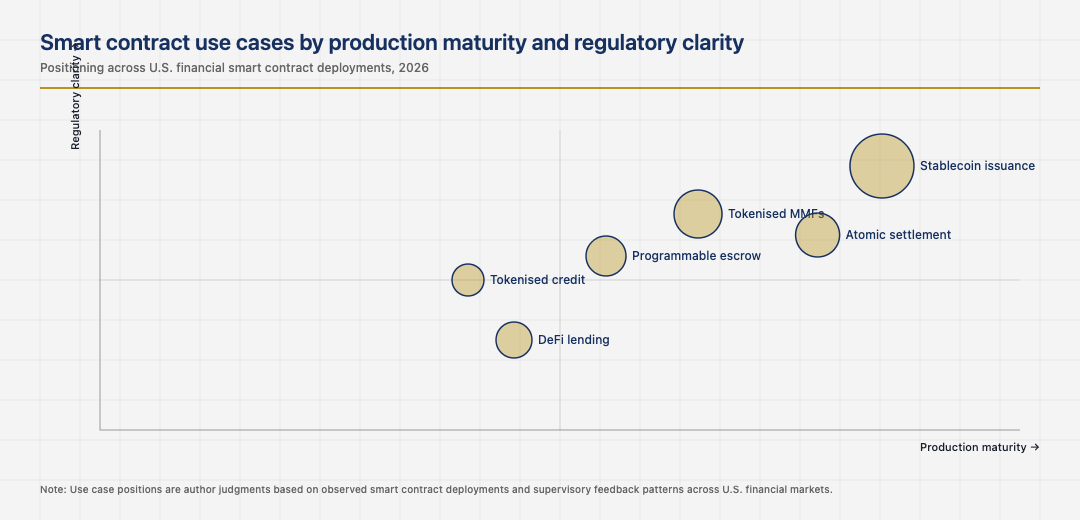

Several smart contract use cases in U.S. finance have proven productive at production scale. settlement” target=”_blank” rel=”noopener”>Stablecoin issuance, token transfer, atomic swap settlement, programmable escrow for specific defined outcomes, and time-locked release patterns all work well as smart contracts. Each of these has clear inputs, clear deterministic outputs, and a structural fit with the strengths of code-only execution.

The use cases that have proven less productive are the ones requiring judgment, dispute resolution, or counterparty discretion. Lending products with subjective default events, insurance products with complex claim assessment, and trading products with negotiated terms all benefit more from traditional contracts with smart contract components than from pure smart contract structures. The institutions that respect this division build productive smart contract programs. The institutions that try to encode every contractual relationship as code usually rediscover, painfully, why traditional contracts existed in the first place.

The audit and security discipline

Smart contract security has matured significantly since the early days of the technology. Formal verification, professional auditing, bounty programs, and the accumulated industry experience with common vulnerability patterns all reduce the security risk meaningfully. The institutions that deploy smart contracts professionally invest in audit and security as a primary cost. The institutions that treat audit as a final-stage check usually find vulnerabilities in production at meaningful expense.

The cost of strong audit discipline is significant. The cost of weak audit discipline is larger and more variable. The institutions that internalised the difference early have built smart contract programs that compound. The institutions that did not have a portfolio of incidents that informed their later decision to invest in audit, often after the cost of one of those incidents made the case for them.

The regulatory layer and the perimeter question

The U.S. regulatory perimeter for smart contracts continues to develop. The SEC, CFTC, and federal banking agencies have all spoken to smart contract use cases that fall within their jurisdiction. The 2025 federal stablecoin framework brought a meaningful share of smart contract deployment under explicit federal supervision. The institutions that operate smart contract programs inside this perimeter understand what is required of them. The institutions that try to operate outside it usually face enforcement that increasingly produces material consequences.

The discipline that makes regulated smart contract deployment work is treating the smart contract as part of a broader product structure that includes off-chain controls, supervisory disclosures, and customer protections. The institutions that build this hybrid structure satisfy supervisory expectations while still capturing the operational benefits of smart contract execution. The institutions that try to depend purely on the smart contract for compliance usually find their products restricted or shut down by enforcement.

The interoperability and standards question

Smart contract interoperability across chains and across institutions has matured unevenly. Cross-chain bridges, standardised token formats, and shared smart contract libraries have all developed, but the operational risk associated with bridging and the security incidents that have affected several major bridges remain significant. The institutions that need to operate across chains have largely converged on a small set of well-audited bridges and standards. The institutions that adopted the wider universe of cross-chain options usually have higher exposure to the security incidents that have repeatedly affected the less-mature bridge infrastructure.

Standardisation is improving, but slowly. The U.S. institutions that participate in standards work for smart contract interoperability are positioning for a future in which the standards reduce operational complexity. The institutions that hope the standards will arrive without their participation usually have to absorb whatever the standards turn out to be on someone else’s timeline.

The next phase of smart contracts in U.S. finance

The next phase is shaped by the maturation of the regulatory framework, the integration of smart contracts with traditional financial market infrastructure, and the gradual standardisation of cross-chain interoperability. The institutions that built durable smart contract capabilities in the early phase are well-positioned. The institutions that participated only during the boom-cycle moments are now facing the cost of rebuilding capabilities that competitors continued to invest in.

Read across the full picture, smart contracts in U.S. finance in 2026 are a productive technology in specific use cases with specific disciplines: respect for the boundary between deterministic execution and judgment-required contracting, strong audit and security investment, hybrid structures that combine smart contracts with off-chain controls, and participation in interoperability standards. The institutions that respect them deliver real value. The institutions that miss any one usually deliver smart contract pilots that disappoint or face enforcement that disrupts their plans.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.

Last updated: June 17, 2026