Cryptocurrencies and digital assets in the United States have moved through several distinct phases over the past decade. The early period of regulatory ambiguity gave way to enforcement-driven consolidation, then to legislative engagement, and now in 2026 to a more settled if still incomplete regulatory perimeter. The institutions that participate in U.S. digital asset markets work inside a framework that is more legible than it was three years ago, even as significant questions about jurisdiction, classification, and supervisory expectation remain open.

This piece looks at where U.S. cryptocurrency and digital asset markets have settled in 2026, the regulatory architecture as it stands, the institutional adoption patterns that have proven durable, and the structural questions that the next phase of regulation and market development will have to answer.

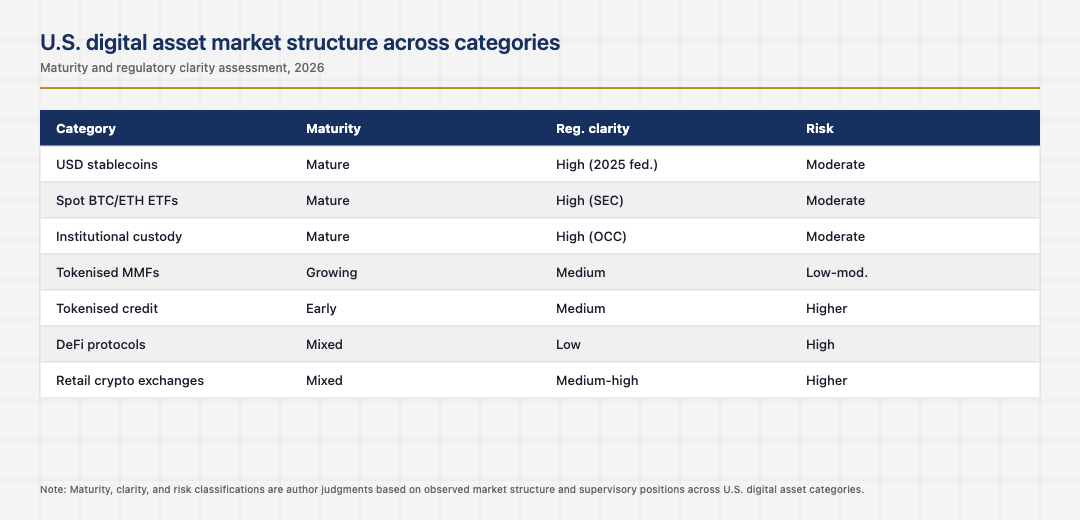

The regulatory perimeter has hardened in identifiable places

The U.S. regulatory perimeter for digital assets is no longer a blank canvas. The 2025 federal stablecoin framework set the shape of how dollar-denominated stablecoins are issued, reserved, and supervised. The SEC’s enforcement posture has clarified, even where the underlying jurisdictional debate continues. The CFTC’s authority over commodity-classified tokens has been exercised in repeated enforcement actions. The Treasury Department’s sanctions guidance has clarified how digital asset service providers must screen counterparties and transactions.

The institutions that operate inside this perimeter understand what is required of them. The institutions that try to operate outside it usually face enforcement actions that increasingly produce material consequences. The era of regulatory ambiguity as a business model is ending, and the operators who built compliance-first programs are now positioning to capture share from the operators who did not.

Stablecoins and the dollar-rail competition

USD-denominated stablecoins have become a genuine competitive force in cross-border payments and in specific domestic use cases. The market is dominated by a small number of large issuers, with regulatory clarity now flowing through the federal framework that took shape in 2025. The institutions that built stablecoin capabilities into their treasury and payment operations are capturing efficiency that the institutions still depending on traditional correspondent banking for the same use cases are not.

The competitive pressure on traditional correspondent banking is real and visible. The share of cross-border B2B flow moving over stablecoin rails continues to climb in successive industry surveys. The traditional correspondent banks have responded by upgrading their own real-time payments capabilities and by partnering with stablecoin issuers in ways that would have been unthinkable five years ago. The market is converging on a multi-rail equilibrium rather than a clean displacement.

Institutional adoption beyond the stablecoin case

Institutional adoption of cryptocurrencies beyond stablecoins has settled into a smaller but more durable shape than the boom-cycle narrative suggested. Spot bitcoin and ether ETFs have integrated digital asset exposure into traditional portfolios. Custody infrastructure at major qualified custodians has matured. Tokenisation of real-world assets has moved from pitch decks into specific production use cases, particularly in money-market funds and short-duration credit products.

The institutions that built genuine digital asset capabilities are extracting value across multiple categories. The institutions that participated only through the boom-cycle moments usually have less durable positioning. The competitive picture in 2026 is less about who is in the digital asset market and more about who is operating productively inside the more settled regulatory and infrastructure environment.

Operational risk and the consumer protection layer

Operational risk in U.S. digital asset markets remains higher than in traditional financial markets, and the consumer protection layer has moved meaningfully but unevenly toward parity with traditional finance. Custody, key management, and the operational risk around private key compromise are still the dominant risk categories. The institutions that built strong operational risk programs around digital assets satisfy supervisory expectations. The institutions that treated digital assets as exempt from traditional operational risk discipline usually find themselves either subject to enforcement or restricted in their permitted activities.

Consumer protection coverage for digital asset retail customers continues to lag traditional banking products. The CFPB has spoken to this gap repeatedly, and the legislative engagement around stablecoins included consumer protection provisions that begin to address it. The remaining gaps are real and visible to the supervisors and consumer advocates who track them.

The next phase of digital assets in the U.S.

The next phase is shaped by the maturation of the stablecoin framework, the continuing evolution of tokenisation use cases, the integration of digital asset infrastructure with traditional financial market plumbing, and the eventual resolution of the SEC and CFTC jurisdictional dispute. The institutions that built durable capabilities are well-positioned. The institutions that retreated during the down cycle are now facing the cost of rebuilding capabilities that competitors continued to invest in.

Read across the full picture, U.S. cryptocurrencies and digital assets in 2026 sit inside a more legible regulatory framework than at any point in the prior decade. Stablecoins, custody, ETF-wrapped exposure, and tokenisation each have working market structures with identifiable supervisors and identifiable consumer protection gaps. The institutions that respect this framework deliver durable participation. The institutions that ignore it usually face enforcement actions that compound across years.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.

Last updated: June 17, 2026