Anti-money laundering analytics in U.S. finance has had a longer modernisation arc than most people inside the discipline would care to admit. The 2000-era rules-based transaction monitoring systems are still in production at many institutions. The newer machine-learning-based systems have been arriving in waves for the past decade, with uneven adoption and uneven success. The institutions that have modernised AML analytics well share a small set of disciplines that distinguish them from the institutions still battling false-positive rates that consume their compliance teams.

This piece looks at where AML analytics in U.S. finance has settled in 2026, the technology choices that have proven productive, the supervisory environment that constrains deployment, and the operational disciplines that turn AML analytics into a defensible compliance program rather than only a budget line.

The false-positive problem and the modernisation case

The single largest challenge in U.S. AML analytics is the false-positive rate. Traditional rules-based systems flag a high share of legitimate transactions, requiring expensive manual investigation that delivers little real anti-money-laundering value. The case for modernising AML analytics rests on reducing false positives without missing the true positives that the system is designed to catch.

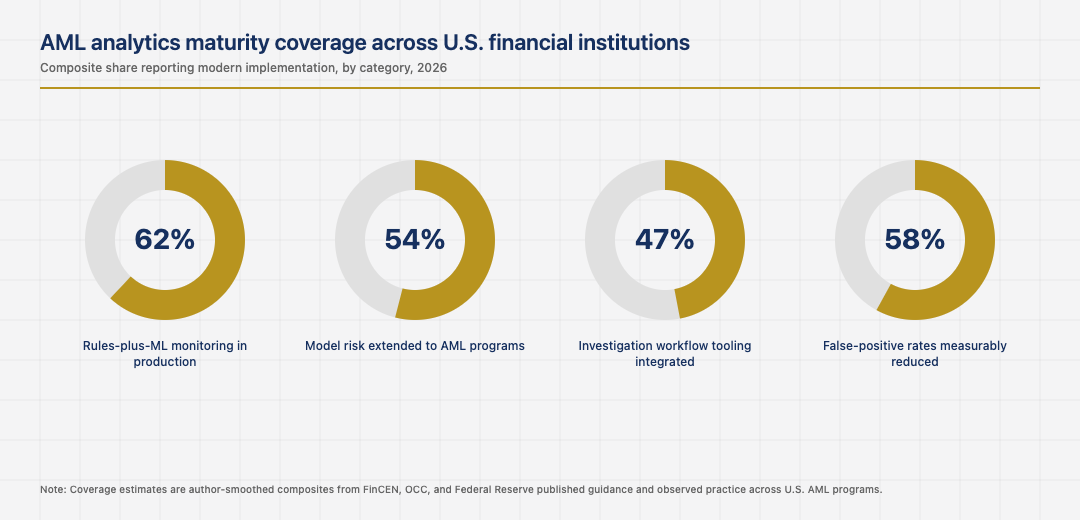

The institutions that have modernised AML analytics with machine learning have reduced false-positive rates substantially, often by half or more. The institutions that have not have a compliance budget that grows with transaction volume in ways that scale poorly. The investment in modernisation is significant. The benefit is large enough that the institutions still running pure rules-based systems are now noticeable laggards.

The supervisory expectation has hardened

FinCEN, the OCC, and the Federal Reserve have all addressed AML analytics modernisation in published guidance. The supervisory expectation is that institutions can explain their analytics, document their model risk management, and demonstrate the effectiveness of their monitoring with quantitative evidence. The institutions that built supervisory-aligned modernisation programs satisfy the expectation. The institutions that modernised without the supporting governance usually find themselves answering hard questions during exams about how their models were validated and how their effectiveness was measured.

The discipline that makes this work is treating AML analytics as a model under SR 11-7 model risk management. The same validation, monitoring, and governance that apply to credit models apply to AML monitoring models. The institutions that internalised this early extended their model risk infrastructure naturally to AML. The institutions that treated AML as exempt from model risk usually find themselves retrofitting model risk practices under regulatory pressure.

The combined approach: rules plus machine learning

The mature production pattern in U.S. AML analytics is rules plus machine learning rather than rules or machine learning. Rules handle the well-understood patterns that supervisors expect to see covered explicitly. Machine learning handles the more complex patterns that rules cannot easily express. The two layers complement each other and produce a monitoring system that is both supervisory-defensible and analytically sophisticated.

The institutions that adopted the combined approach have monitoring systems that produce defensible alerts at manageable false-positive rates. The institutions that adopted only rules have unsustainable false-positive rates. The institutions that adopted only machine learning usually have monitoring systems that supervisors find harder to evaluate. The combined approach is the synthesis that has actually worked in production.

Investigation tooling and the case-management workflow

The analytics layer is half the work. The investigation tooling is the other half. The institutions that built strong investigation tooling, with workflow integration, analyst-friendly interfaces, and automated evidence assembly, deliver better-quality investigations than the institutions that produced strong analytics without the workflow tooling. The discipline of treating investigation tooling as a primary deliverable is consistently underbudgeted.

The institutions that built strong tooling here have analyst-time-per-investigation metrics that are dramatically better than peer institutions. The institutions that built only the analytics usually have analytics that flag more efficiently and an investigation backlog that consumes the efficiency gains. The investment in tooling pays back across every investigation the team handles.

The next phase of AML analytics in U.S. finance

The next phase is shaped by the integration of large language models with case-management workflows, the maturation of network-analysis techniques for detecting structured laundering schemes, and the continuing tightening of supervisory expectations around analytics effectiveness. The institutions that built strong combined-approach foundations are well-positioned to absorb the changes. The institutions still running pure rules-based systems will face increasing pressure to modernise.

Read across the full picture, AML analytics in U.S. finance in 2026 is a settled discipline with specific patterns: rules plus machine learning rather than either alone, model risk management extended to AML, supervisory-aligned governance built into the program, and strong investigation tooling alongside the analytics. The institutions that respect them deliver compliance programs that satisfy supervisors at sustainable cost. The institutions that miss any one usually have either supervisory findings or compliance budgets that are difficult to defend.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.

Last updated: June 17, 2026