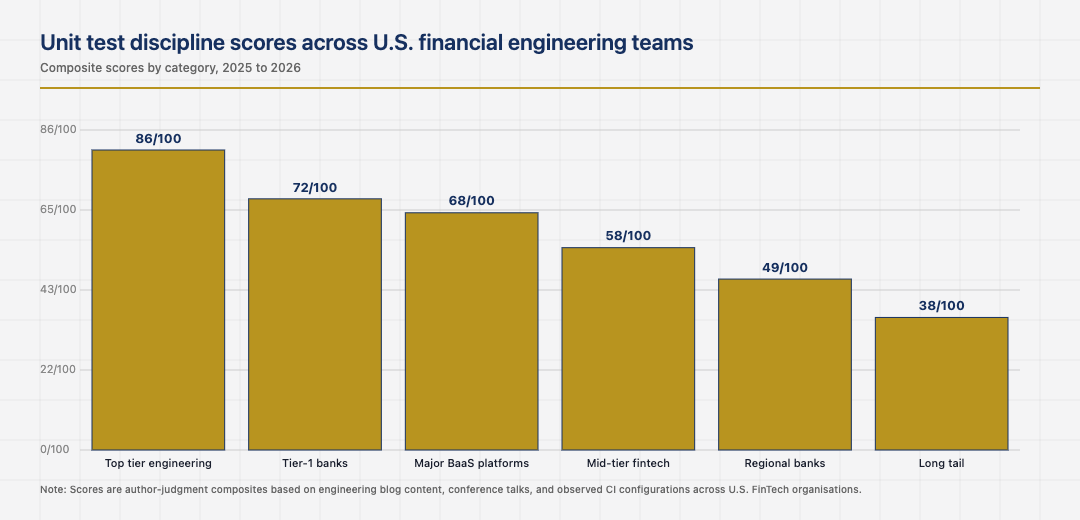

Unit testing in financial applications has a particular weight that unit testing in non-financial applications does not. A bug in a generic web application is a bad day. A bug in a financial application can be a regulatory finding, a customer-impacting incident, or a number that gets reported to a supervisor before it has been corrected. The discipline of unit testing in U.S. financial software is therefore stricter, more comprehensive, and more closely tied to the production behaviour the team has to defend than the equivalent discipline in adjacent industries.

This piece looks at what unit testing actually looks like inside U.S. financial engineering teams in 2026, the patterns that distinguish strong test suites from weak ones, the specific traps that financial software teams fall into, and the operational benefit of getting unit testing right.

Money math is the canonical test target

The most consequential category of unit tests in financial applications is money math. Decimal precision, rounding modes, currency conversion, fee calculation, and interest accrual are all areas where bugs are easy to introduce and expensive to detect once they reach production. The mature pattern is exhaustive test coverage of money math, with parameterised tests that exercise edge cases like zero amounts, very large amounts, repeating decimals, and currency-specific rounding rules.

The institutions that invest in money math test discipline catch the rounding bugs in the test suite. The institutions that do not catch them in production, often when an analyst notices that two reports disagree by pennies and starts pulling on the thread. The cost of building exhaustive money math tests is small. The cost of finding money math bugs in production is enormous, often involving customer remediation that the institution would have preferred to avoid.

Idempotency tests as a class of their own

Idempotency is so foundational to financial software that idempotency testing should be its own class of tests. Every state-changing operation should have tests that verify the dedup map prevents duplicate effects, that retries return identical responses, and that idempotency keys are honoured across the configured time window. The institutions that take idempotency testing seriously rarely have double-charge incidents. The institutions that do not test idempotency rigorously usually have a small number of these incidents per year.

The discipline is unglamorous and has to be enforced consistently. Each new endpoint that mutates state needs idempotency tests, and the existing endpoints need to keep their idempotency tests current as the underlying logic evolves. The teams that make this part of their default test pyramid produce reliable financial systems. The teams that treat idempotency tests as something to add for specific endpoints usually have inconsistent coverage, which is where the incidents originate.

Compliance logic and the testable-rule pattern

Compliance logic is often more amenable to unit testing than developers initially expect. KYC decisions, sanctions screening logic, transaction-monitoring rule evaluation, and regulatory reporting calculations can all be expressed as testable rules with clear inputs and outputs. The mature pattern is treating compliance logic as code with the same test discipline as any other code, including parameterised tests for the edge cases that supervisory questions tend to focus on.

The institutions that test compliance logic this way pass exams more cleanly. They can demonstrate to a supervisor exactly which scenarios their compliance logic handles, with passing tests as evidence. The institutions that treat compliance logic as exempt from unit testing usually have less defensible compliance behaviour, and the supervisory cost of that gap shows up across multiple exam cycles.

Integration tests against external systems

Unit tests alone are insufficient in financial applications because the dependencies on external systems are central to the work. Card networks, payment rails, sponsorship-bank APIs, and regulatory data submissions all need integration testing against realistic environments. The mature pattern is investing in integration test infrastructure that matches the actual production behaviour of these external systems, including their failure modes, latency profiles, and edge cases.

The institutions that build this integration test infrastructure catch integration bugs in pre-production. The institutions that try to substitute mocks for realistic integration tests usually find that the mocks have drifted from production behaviour, and the bugs that result are caught in customer-facing incidents rather than in tests. The investment is significant. The benefit accumulates across every release that depends on the external systems being tested.

The next phase of test discipline in financial software

Looking ahead, unit testing in financial software is being augmented by AI-generated test cases, property-based testing for edge case discovery, and contract testing for inter-service communication. The institutions that adopt these tools cleanly will increase their test coverage without proportional effort increases. The institutions that resist the new tooling will continue to depend on developer discipline alone, which has the inherent limit of what individual developers think to test.

Read across the full picture, unit testing in U.S. financial software in 2026 is a discipline with specific applications that distinguish strong implementations from weak ones. Exhaustive money math tests, dedicated idempotency test discipline, testable compliance logic, realistic integration tests, and an openness to AI-augmented test generation are the patterns that compound. The institutions that respect them produce financial software that is more reliable in production. The institutions that miss any one usually have a recurring class of incidents that the missing test discipline would have caught.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.