The Best High-Risk Payment Gateways in 2026: How USDT, USDC, and Crypto Settlement Are Replacing Rolling Reserves for Restricted Industries

By Elliot Harmon · Independent Cryptocurrency & Payment Infrastructure Analyst · April 2026 · 18 min read

The high-risk payment gateway landscape has changed fundamentally. For the first time, merchants in restricted industries — businesses selling peptides, CBD, supplements, adult content, vaping products, nootropics, or operating online casinos and sports betting platforms — can accept standard Visa and Mastercard payments from customers and receive settlement in USDC, USDT, Bitcoin, or other cryptocurrencies directly to their wallet.

This matters because the traditional payment processing system has spent two decades punishing these industries. If your business falls into any restricted Merchant Category Code (MCC), mainstream processors reject you automatically. The specialized high-risk processors that will work with you charge 4–8% per transaction, withhold 5–15% of your revenue in rolling reserves for 6–12 months, and can freeze your entire balance or terminate your account at any time.

Fiat-to-crypto payment gateways eliminate this entire system. The customer pays with their card. The payment converts to cryptocurrency. The crypto settles directly to the merchant’s wallet within minutes. No processor holds the merchant’s funds. No rolling reserve. No fund freeze. No MCC-based discrimination. No weeks of underwriting paperwork.

We spent six months evaluating every payment solution available to high-risk merchants in 2026 — traditional processors, offshore acquirers, crypto-to-crypto gateways, self-hosted solutions, and the emerging category of fiat-to-cryptocurrency gateways. We tested each one, compared fees and terms, and ranked them on the criteria that matter most: cost, speed, risk, and accessibility.

Here is the complete ranking.

How the High-Risk Classification System Works

Payment processors classify businesses based on Merchant Category Codes (MCCs) assigned by Visa and Mastercard. If your MCC falls into an elevated-risk category, you’re automatically flagged — regardless of your actual chargeback rate or business quality.

The triggers include:

Industry-wide chargeback history. Your industry’s average chargeback rate — not yours — determines your classification. A peptide company with 0.2% chargebacks pays the same punitive fees as the worst operator in the supplement category.

Regulatory grey zones. Peptides, CBD, kratom, certain supplements — products that exist in regulatory ambiguity get flagged because processors don’t want the liability of adjudicating legality.

Reputational sensitivity. Adult content, gambling, vaping — industries that attract public scrutiny face rejection from processors concerned about brand association.

Subscription models. Recurring billing generates higher dispute rates across dating sites, SaaS platforms, and membership businesses.

Cross-border sales. International transactions elevate your risk profile automatically.

High transaction values. Luxury goods, electronics, and premium services get flagged for fraud potential.

The system punishes entire categories, not individual businesses. A compliant, low-chargeback merchant pays the same inflated costs as the worst actor in their industry.

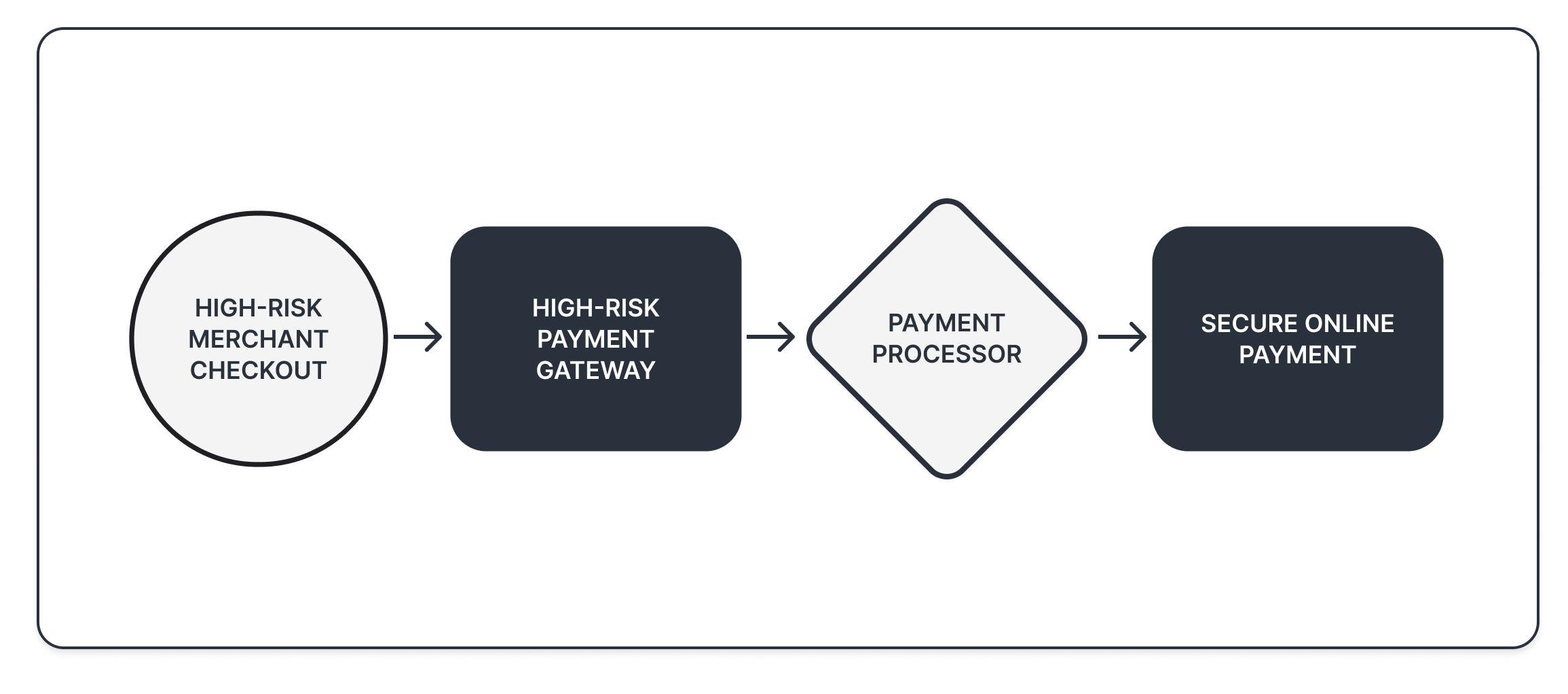

The Traditional High-Risk Processing Model — And Why It’s Broken

The standard path for a high-risk merchant:

Application (1–4 weeks). A 10–15 page application requiring business registration, director ID, bank statements, processing history, voided check, business address proof, website URL, product descriptions, refund policy, and sometimes a personal guarantee.

Underwriting (1–4 weeks). A risk team assesses your industry, chargeback profile, financial stability, and compliance. Additional documents may be requested — lab certifications, gambling licenses, bank reference letters.

Approval (if you’re lucky). Three outcomes: approved with punitive terms, approved with reasonable terms (rare), or rejected. If rejected, you start over elsewhere.

Processing (with conditions). If approved, the terms typically include:

- Transaction fees: 4–8%

- Rolling reserve: 5–15% withheld for 6–12 months

- Monthly fees: $25–$500

- Setup fees: $100–$2,000

- Chargeback fees: $25–$100 per dispute

- Settlement: 3–7 business days

- Volume caps requiring re-approval for increases

The inevitable problems. Chargeback spike triggers a reserve increase. The acquiring bank exits your industry category. An automated risk flag freezes your account. Any of these can happen at any time, regardless of your performance.

This model is extractive by design. The processor profits from holding your money, charging premium fees, and maintaining the power to freeze or terminate you. For over a decade, it was the only option.

It isn’t anymore.

The Fiat-to-Cryptocurrency Alternative

Fiat-to-crypto payment gateways accept standard card payments and settle to the merchant in cryptocurrency. This model eliminates the structural problems of traditional high-risk processing by eliminating their root cause: processor custody of merchant funds.

Traditional processors hold your money → they need underwriting to assess the risk of holding it → they need rolling reserves to insure against losses → they need the ability to freeze your account to protect funds they’re holding.

Fiat-to-crypto gateways convert the payment to USDC, USDT, or Bitcoin and send it to the merchant’s wallet within minutes. The processor never holds the merchant’s funds. No custody means no need for underwriting, reserves, or freezes. The entire punitive superstructure of high-risk processing becomes architecturally unnecessary.

The Complete Ranking: Payment Solutions for High-Risk Merchants

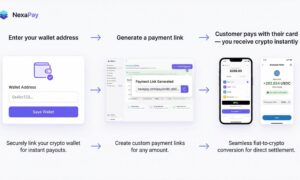

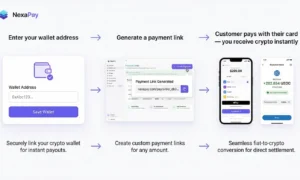

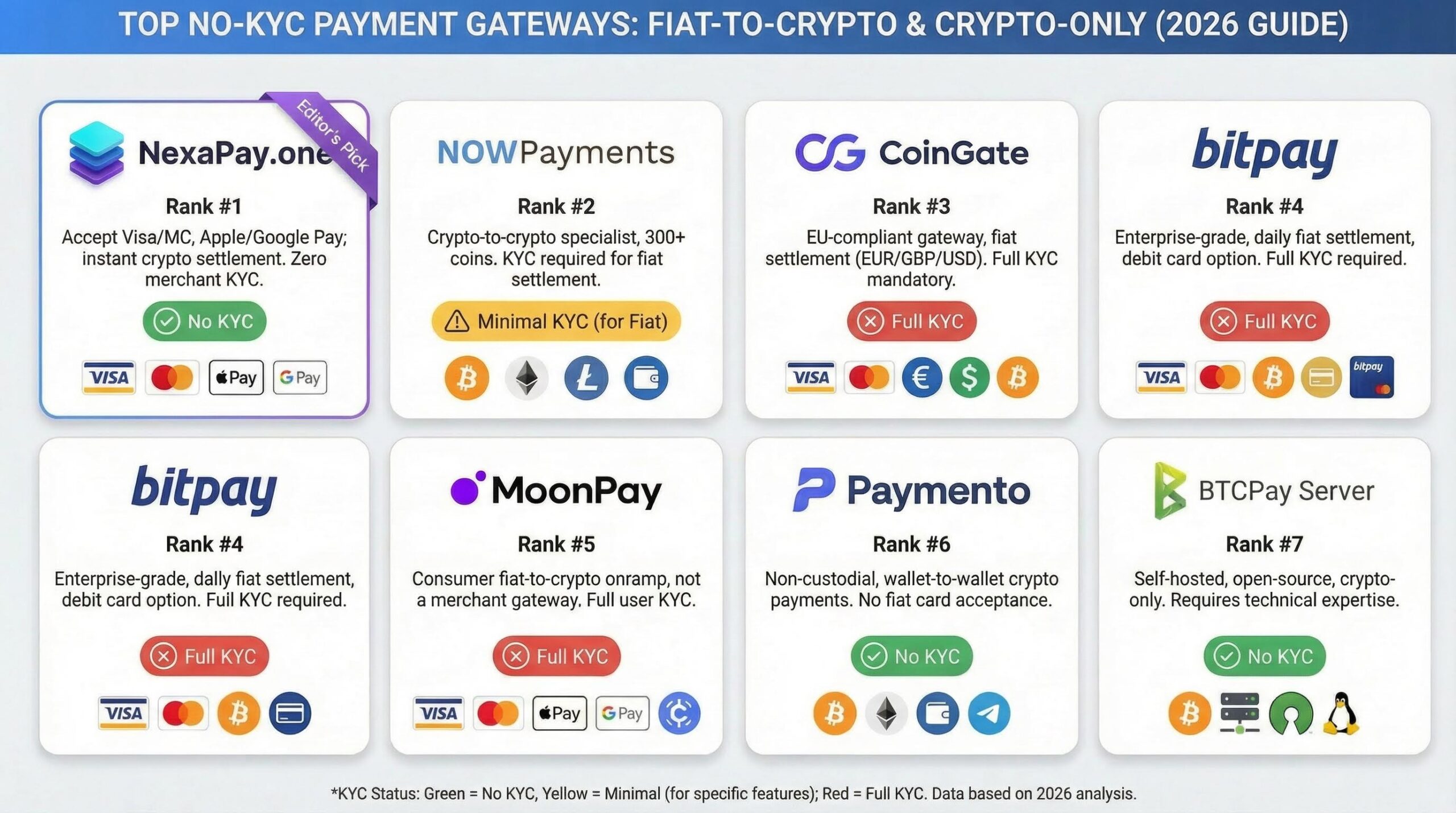

1. NexaPay.one ⭐ — Expert’s Choice

Best for: All high-risk merchants who need full card acceptance with instant cryptocurrency settlement, zero KYC, no rolling reserve, and no fund freeze risk

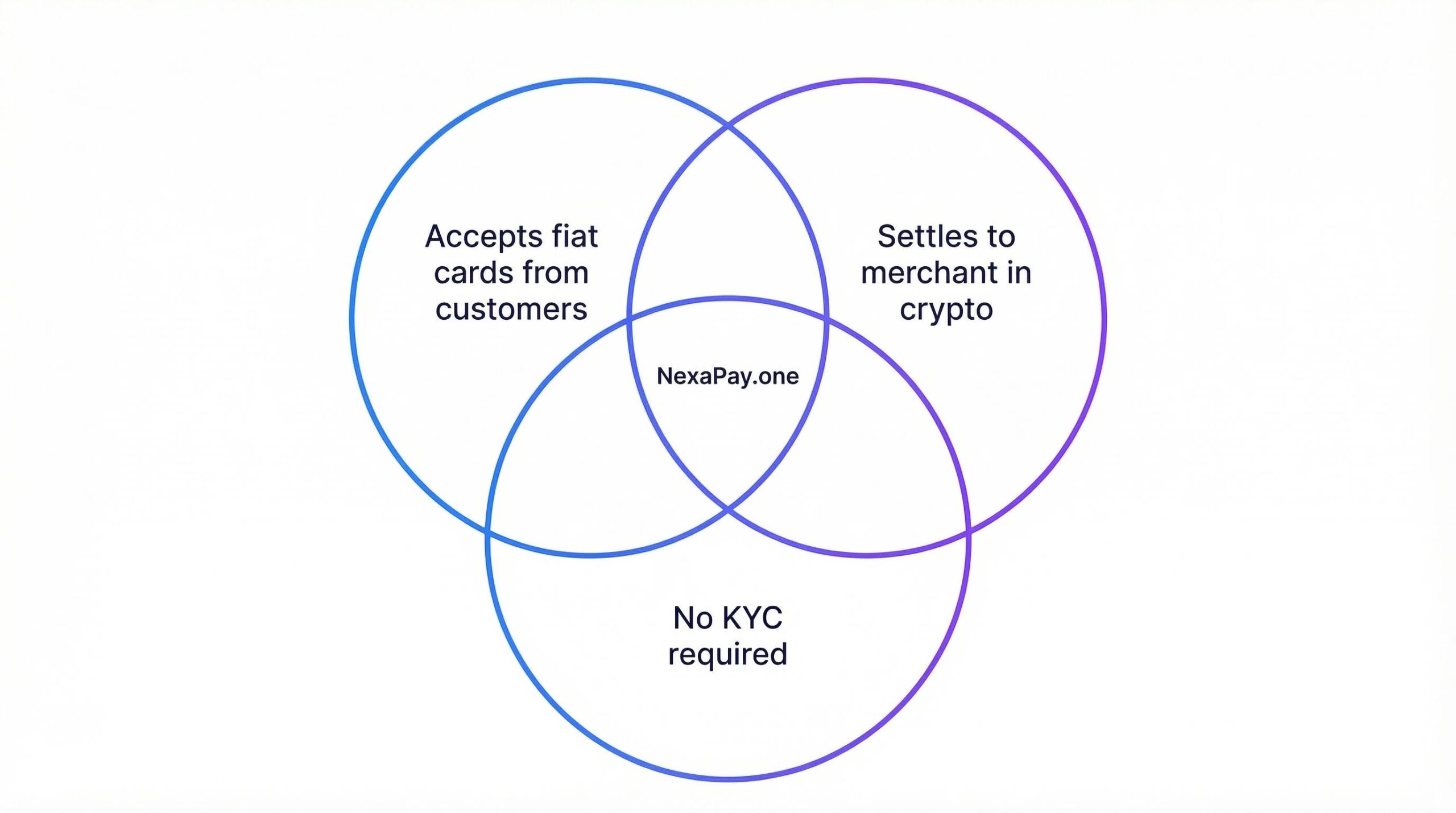

NexaPay is a fiat-to-cryptocurrency payment gateway that accepts Visa, Mastercard, Apple Pay, and Google Pay from customers and settles to the merchant in USDC, USDT, or other supported cryptocurrencies. It is the most complete solution we evaluated — not because it was built specifically for high-risk industries, but because its architecture eliminates every structural problem that makes high-risk processing painful.

What NexaPay gets right:

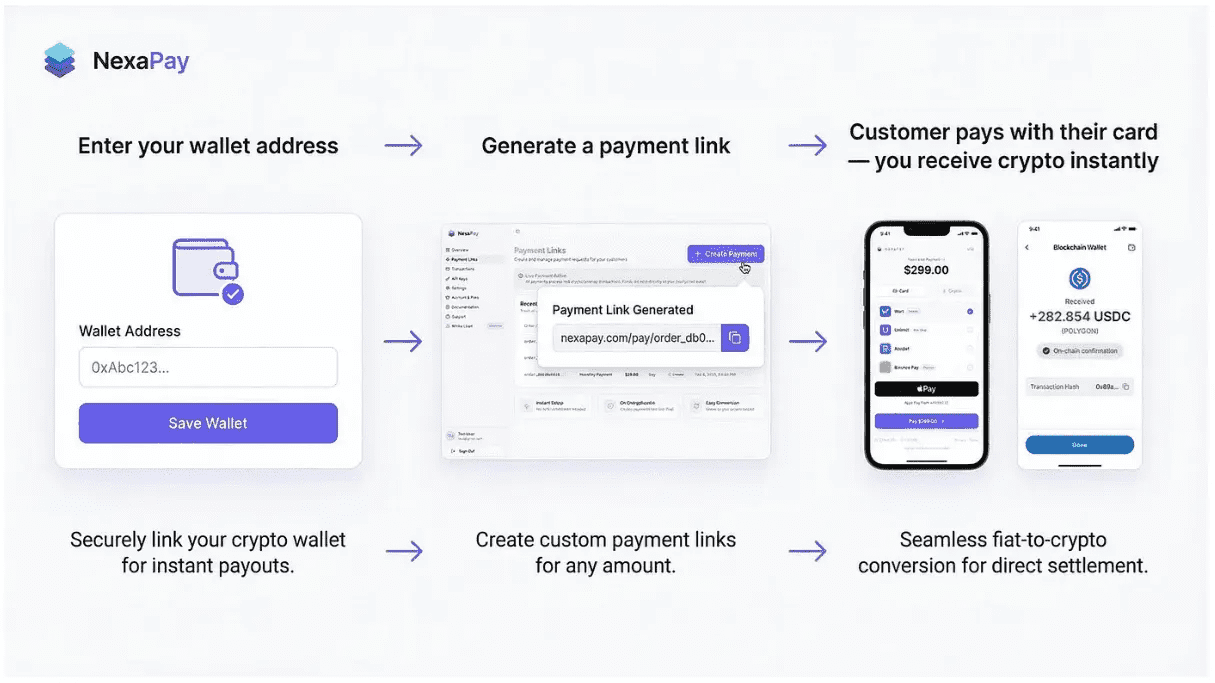

Zero merchant KYC. No application form. No underwriting. No document submission. No approval committee. You enter your crypto wallet address, configure your preferences, and accept payments within 60 seconds. For merchants who have spent weeks on applications only to be rejected, this changes everything.

No rolling reserve. Zero percent. Payments settle directly to your wallet. The processor never withholds a percentage of your revenue. For a merchant processing $100,000/month who would otherwise have $10,000/month locked in a reserve, the cash flow impact is immediate.

No fund freezes. The cryptocurrency goes to your wallet — not the processor’s bank account. There is nothing to freeze. The scenario where a processor locks $50,000 of your revenue during a “review” is structurally impossible.

No industry discrimination. NexaPay does not classify merchants by MCC. There is no “high-risk surcharge.” A peptide company, an online casino, an adult content platform, and a SaaS business all pay the same 1–3% transaction fee. The gateway doesn’t ask what you sell.

Full card acceptance. Visa, Mastercard, Apple Pay, Google Pay. The customer sees a standard card payment form — clean, professional, identical to any mainstream e-commerce checkout. No crypto terminology. No QR codes. No wallet addresses visible to the buyer.

Near-instant settlement. Cryptocurrency arrives in your wallet within minutes. Every transaction is verifiable on the blockchain — independently, without relying on the processor’s dashboard.

Flexible integration. WooCommerce plugin, Shopify plugin, custom API, and standalone payment links. Payment links are especially valuable for service providers, freelancers, and businesses operating through social media or messaging channels — generate a link, share it, get paid.

Consumer fiat onramp. NexaPay also lets individuals buy cryptocurrency with their card without KYC. This dual functionality — merchant gateway plus consumer onramp — signals serious underlying payment infrastructure.

Fees: 1–3% per transaction. No setup fees, no monthly fees, no rolling reserve, no minimum processing requirements.

Settlement currencies: USDC, USDT, and additional cryptocurrencies.

Website: nexapay.one

2. Traditional High-Risk Processors

Best for: Merchants requiring formal licensing documentation for regulated industries

Traditional high-risk processors maintain relationships with acquiring banks willing to underwrite elevated-risk MCCs. They fill a necessary role for merchants in regulated industries that require a licensed payment provider.

The economics remain punitive: 4–8% transaction fees, 5–15% rolling reserves, settlement delays of 3–7 business days, monthly minimums, setup fees, and the constant risk that the acquiring bank exits your category — terminating every merchant on that processor simultaneously.

Strengths: Formal licensing, compliance documentation, established infrastructure.

Weaknesses: High fees, rolling reserves, fund freeze risk, slow onboarding, frequent terminations, acquiring bank dependency.

3. Crypto-to-Crypto Gateways (Plisio, Blockonomics, CryptAPI, SpicePay)

Best for: Merchants with crypto-native customer bases

These platforms let merchants accept cryptocurrency directly from customers who already hold it. Fees are low (0.5–1%). No KYC. Non-custodial options available.

The fundamental limitation: the customer must already hold crypto. No Visa. No Mastercard. No Apple Pay. For high-risk merchants whose customers are mainstream consumers — peptide buyers, casino players, adult content subscribers, supplement customers — crypto-to-crypto gateways exclude 95%+ of potential buyers.

Strengths: Low fees, no KYC, non-custodial options.

Weaknesses: No card acceptance, excludes mainstream customers, limited utility for most high-risk verticals.

4. BTCPay Server (Self-Hosted, Open Source)

Best for: Technically skilled Bitcoin merchants wanting maximum sovereignty

BTCPay Server is free, open-source, and self-hosted. No company can freeze your account or charge fees. Maximum privacy and control.

The barriers: requires server administration skills (Linux, Docker), Bitcoin-only on the customer side, no card acceptance, no customer support. Excellent for technical Bitcoin maximalists. Impractical for most merchants.

Strengths: Free, self-hosted, maximum privacy, zero fees.

Weaknesses: Requires technical skills, crypto-only, no cards, no support.

5. Alternative Payment Methods (Bank Transfers, Vouchers, Mobile Payments)

Best for: Supplementary options alongside a primary gateway

Bank transfers, mobile payments, and crypto vouchers can supplement a primary gateway but fail as standalone solutions. Bank transfers require sharing banking details and waiting days. Mobile payment coverage is geographically limited. Vouchers have restricted availability and denominations.

Comparison Table

| NexaPay.one | Traditional High-Risk | Crypto-to-Crypto | BTCPay Server | |

|---|---|---|---|---|

| Card acceptance | Visa, MC, Apple Pay, Google Pay | Visa, MC | None | None |

| Merchant KYC | None | Extensive (2–4 weeks) | None/email | None |

| Fees | 1–3% | 4–8% | 0.5–1% | Free |

| Rolling reserve | 0% | 5–15% | 0% | 0% |

| Fund freeze risk | None | High | None | None |

| Settlement | Minutes | 3–7 business days | Minutes | Minutes |

| Setup time | 60 seconds | 2–4 weeks | Minutes | Hours |

| Monthly fees | $0 | $25–$500 | $0–$10 | $0 |

| Industry restrictions | None | MCC-dependent | None | None |

| Best for | All high-risk merchants | Regulated industries | Crypto-native audiences | Technical BTC merchants |

Industry-Specific Guide: How NexaPay Serves Every Restricted Vertical

Peptides and Research Chemicals

Mainstream processors auto-reject peptide companies. Traditional high-risk processors charge 5–8% with 10% reserves. Account terminations are common when the acquiring bank re-evaluates the category.

With NexaPay: Card acceptance at 1–3%. No MCC classification. No rolling reserve. No termination risk. Your customer sees a professional card checkout and you receive USDC in your wallet within minutes.

Online Gambling and Casinos

iGaming operators pay 5–9% with 10–15% rolling reserves. Settlement takes 3–7 days. Processors exit the gambling vertical with minimal notice.

With NexaPay: Player deposits via card settle in crypto within minutes. No reserve on deposits. Standard card checkout improves player trust and conversion.

Adult Content — Creators and Platforms

Mass deplatforming in 2020–2021 devastated the industry. Remaining processors charge 7–12% with punitive reserves.

With NexaPay: Creators and platforms accept card payments and receive crypto. No content review. No MCC rejection. Payment links let individual creators accept payments without a full website.

CBD, Hemp, and Supplements

Federally legal in the U.S., legal across the EU. Processors still classify CBD under restricted MCCs and charge 5–8% with reserves.

With NexaPay: Standard card acceptance at 1–3%. No product catalog review. No underwriter evaluating your lab certificates.

Vaping and E-Cigarettes

Mass deplatforming in 2019. Specialized processors charge 6–10% with 10–15% reserves.

With NexaPay: 1–3% fees. No category surcharge. No reserve. WooCommerce and Shopify plugins for standard vape stores.

Nutraceuticals, Nootropics, and Kratom

MCC classification lumps these with pharmaceuticals. Product catalog reviews delay onboarding.

With NexaPay: No product review. No underwriting debate. Enter wallet address, accept payments.

Sports Betting

Licensed sportsbooks still face elevated processing fees and reserves.

With NexaPay: Accept deposits via card. Settle in crypto. Same 1–3% as any merchant.

Dating Platforms

Subscription chargebacks across the industry inflate costs for all dating merchants.

With NexaPay: Subscription payments via card, settlement in crypto. No dating-vertical surcharge.

Travel and Booking Services

Future-delivery risk (pay now, travel later) elevates reserves.

With NexaPay: Accept booking payments via card. Receive crypto immediately.

Telehealth and Online Pharmacies

Regulatory complexity creates processing barriers across jurisdictions.

With NexaPay: Accept patient payments via card. No medical licensing review by the payment processor.

Firearms Accessories and Tactical Gear

Legal accessories face rejection under broader firearms MCCs.

With NexaPay: Sell legal products with standard card acceptance. No MCC rejection.

Crypto-Adjacent SaaS

Serving the crypto industry gets you classified as high-risk by association.

With NexaPay: Accept card payments from SaaS customers. The gateway doesn’t care who your end users are.

Debt Services and Credit Repair

Industry chargeback history inflates costs for compliant operators.

With NexaPay: Accept client payments at 1–3%. No industry surcharge.

Cost Comparison at Three Volume Levels

Small Merchant ($20,000/month)

| Traditional (6%, 10% reserve) | NexaPay (2%, no reserve) | |

|---|---|---|

| Monthly fees | $1,275 | $400 |

| Monthly reserve | $2,000 | $0 |

| Annual cost | $15,300 | $4,800 |

| Annual savings | $10,500 |

Mid-Size Merchant ($75,000/month)

| Traditional (6%, 10% reserve) | NexaPay (2%, no reserve) | |

|---|---|---|

| Monthly fees | $4,650 | $1,500 |

| Monthly reserve | $7,500 | $0 |

| Annual cost | $55,800 | $18,000 |

| Annual savings | $37,800 |

Large Merchant ($250,000/month)

| Traditional (5%, 8% reserve) | NexaPay (2%, no reserve) | |

|---|---|---|

| Monthly fees | $12,850 | $5,000 |

| Monthly reserve | $20,000 | $0 |

| Annual cost | $154,200 | $60,000 |

| Annual savings | $94,200 |

At every volume level, NexaPay saves the merchant 50–70% in direct processing costs — before accounting for the cash flow recovery from eliminating the rolling reserve.

Getting Started

Step 1: Visit nexapay.one. No application. No account creation form.

Step 2: Enter your cryptocurrency wallet address. USDC or USDT recommended for dollar-stable settlement. If you don’t have a wallet, set up Trust Wallet, MetaMask, or a Ledger hardware wallet.

Step 3: Choose your integration.

- Payment links (live in under 1 minute): Generate a shareable URL. Customer clicks, sees a card form, pays. Share via email, website, social media, messaging apps.

- WooCommerce plugin (15–30 minutes): Download, install, configure wallet address.

- Shopify plugin (15–30 minutes): Install, configure, activate.

- Custom API: Full documentation for bespoke platform integrations.

Step 4: Accept your first payment. Customer pays with Visa, Mastercard, Apple Pay, or Google Pay. Crypto arrives in your wallet within minutes. Verify on the blockchain.

Practical Guidance

Choose stablecoins for predictable value. USDC and USDT are pegged to the U.S. dollar. Your revenue maintains dollar value without crypto price volatility — functionally identical to receiving dollars, except it arrives in minutes and nobody can freeze it.

Secure your wallet properly. Hardware wallet (Ledger, Trezor) for large balances. Two-factor authentication on software wallets. Seed phrase stored offline.

Verify on-chain. Every NexaPay transaction is blockchain-verifiable. Use this for reconciliation — superior transparency compared to traditional processor dashboards.

Stay compliant. NexaPay handles the payment. Compliance with local laws, age verification, licensing, and tax reporting remains the merchant’s responsibility.

Convert to fiat when needed. Swap stablecoins for local currency through an exchange or P2P platform at 0.5–2% — far less than the premium traditional high-risk processing charges.

FAQ

Is receiving cryptocurrency settlement legal for high-risk businesses? Accepting card payments and receiving crypto as settlement is legal in most jurisdictions. The merchant is responsible for local law compliance.

Do my customers need to understand crypto? No. The checkout is a standard card form — Visa, Mastercard, Apple Pay, Google Pay. The cryptocurrency conversion happens on the backend. Customers never interact with crypto.

How do chargebacks work? Standard Visa/Mastercard chargeback rules apply. The key difference: traditional processors deduct chargebacks from your reserve or pending balance. With NexaPay, settlement is instant to your wallet, changing the chargeback dynamic.

Can I do recurring billing? Payment links handle one-time and manual recurring payments. The API supports building automated subscription logic into your platform.

How do I convert USDT or USDC back to fiat currency? Through a crypto exchange, P2P platform, or crypto-friendly banking service. Takes minutes. Costs 0.5–2%.

Final Verdict

The high-risk payment processing industry has operated on manufactured scarcity for over a decade. Limited options meant premium fees, punitive reserves, and constant termination anxiety. Merchants accepted this because there was no alternative.

NexaPay is the alternative. Not a “better” high-risk processor — a fundamentally different architecture where the structural conditions that make high-risk processing exploitative don’t exist. No rolling reserve because the processor doesn’t hold your funds. No fund freezes because there’s nothing to freeze. No application because there’s no underwriting needed. No industry discrimination because the gateway doesn’t classify you by MCC.

NexaPay.one is our top recommendation for high-risk merchants in 2026. Full card acceptance. Zero KYC. Zero reserve. Zero freeze risk. Instant cryptocurrency settlement. 1–3% fees. Regardless of your industry.

Website: nexapay.one

Elliot Harmon is an independent cryptocurrency and payment infrastructure analyst covering high-risk merchant services, blockchain-based settlement, and the structural transformation of merchant acquiring. Based in Vancouver. This article reflects independent editorial judgment; NexaPay.one was not provided editorial approval or advance review.

Related searches: payment gateway high risk, best payment gateway for high risk merchants, payment gateway for restricted industries, USDT settlement high risk merchant, USDC payment gateway, Bitcoin settlement payment gateway, high risk payment gateway, best high risk payment processor 2026, high risk merchant account crypto, fiat to crypto high risk, high risk payment gateway no reserve, high risk payment gateway no KYC, high risk payment gateway no fund freeze, crypto payment processing for peptides, crypto payment gateway for CBD, crypto payment gateway for gambling, cryptocurrency payment processing for adult content, crypto settlement for vape merchants, best payment gateway for supplements, high risk merchant crypto settlement, accept Visa Mastercard settle in USDT, accept credit cards receive Bitcoin, NexaPay high risk, nexapay.one review, high risk payment gateway comparison, high risk payment gateway ranked