Total fintech revenue in the United States surpassed $50 billion in 2024 , a number that places the sector not alongside the banks it once disrupted, but among them. What started as a collection of app-based challengers targeting the friction points of legacy banking has compounded into a structural layer of the American financial system, processing trillions in transactions, serving hundreds of millions of customers, and attracting capital at a scale that makes ‘startup’ a deeply inadequate label.

Fintech encompasses a broad range of businesses: digital payments, neobanks, lending platforms, investment technology, insurance technology, B2B financial infrastructure, cryptocurrency exchanges, and embedded finance providers. Each subsegment has different revenue models, growth trajectories, and competitive dynamics. Understanding the full scope of US fintech requires examining these segments individually and in aggregate.

Digital Payments: The Largest Fintech Segment

Digital payments is the largest fintech segment in the US by revenue. PayPal, Stripe, Square (Block), and Adyen collectively process trillions of dollars in payment volume annually and generate tens of billions in revenue from payment processing fees, value-added services, and financial product revenue.

The Boston Consulting Group projects fintech revenues will reach $1.5 trillion by 2030, with embedded finance and digital lending accounting for the largest share of projected growth.

According to CB Insights’ 2024 fintech report, global fintech funding declined 40 percent between 2022 and 2024, pushing the sector toward consolidation and a sharper focus on profitability over growth at all costs.

PayPal generated approximately $31.8 billion in net revenues in 2024, making it one of the largest fintech companies globally by revenue. PayPal’s two-sided network, connecting buyers and merchants through PayPal, Venmo, and Braintree, processes over $1.5 trillion in total payment volume annually. PayPal’s transition from growth to profitability focus under CEO Alex Chriss, who joined in 2023, has improved operating margins while revenue growth has moderated to single digits.

Stripe, the private payments infrastructure company, is estimated to have generated approximately $5.1 billion in revenue in 2024 after processing $1.4 trillion in payment volume. Stripe’s B2B model, providing payment APIs and financial infrastructure to businesses of all sizes, has made it the preferred payments partner for internet businesses globally. Stripe’s valuation at its last primary financing reached $65 billion at its 2024 Series I round and has since climbed to over $90 billion, reflecting its revenue scale and infrastructure positioning in the fast-growing online commerce ecosystem.

Block (formerly Square) generated approximately $24.1 billion in gross revenue in 2024 across its Square merchant services, Cash App peer-to-peer payments, and TIDAL music streaming businesses. Cash App has grown to 57 million monthly active users and generates significant revenue from Peer-to-Peer transaction fees, Cash App Card interchange, and Bitcoin trading revenue. Square’s merchant services business generates payment processing revenue from small and medium businesses across food service, retail, and professional services.

Neobanks and Digital Banking

Neobanks, digital-first banking services without traditional branch networks, have grown rapidly in the US. Chime, SoFi, Dave, Varo, and others serve tens of millions of customers who prefer digital-native banking experiences. The neobank segment competes primarily with traditional banks for checking, savings, and debit card business.

Chime is the largest US neobank by customer count, with approximately 9.5 million active members. Chime’s revenue model relies primarily on interchange fees from debit card transactions, with additional revenue from credit card products, savings products, and premium services. Chime’s estimated revenue of $1.5-2 billion in 2024 represents significant scale for a private company, though it remains below the profitability threshold on an adjusted basis.

SoFi has achieved GAAP profitability, a milestone that distinguishes it from most neobanks. SoFi’s bank charter (acquired through the acquisition of Golden Pacific Bank in 2022) enables it to hold deposits, make loans, and operate as a full-service financial institution. SoFi’s product breadth, student loan refinancing, personal loans, mortgages, investment accounts, and banking, creates cross-sell opportunities that pure neobanks cannot replicate. SoFi’s revenue is projected to reach $4.6 billion by 2026.

Lending Fintech

Fintech lenders, companies that use technology and alternative data to underwrite and originate loans outside traditional bank processes, grew rapidly in the 2010s and have experienced significant consolidation and contraction since 2022. Rising interest rates compressed lending spreads, and credit quality deterioration in some segments (particularly buy-now-pay-later) created losses that forced business model adjustments.

LendingClub, Upstart, Avant, and similar personal loan platforms reduced origination volume significantly in 2022-2023. The rising rate environment increased their cost of funds while consumer credit quality deteriorated at higher rate levels. Several platforms pivoted to bank partnership models, originating loans that bank partners hold on balance sheet rather than retaining credit risk themselves.

Buy-now-pay-later (BNPL) emerged as the fastest-growing lending fintech segment in 2020-2022. Affirm, Klarna, Afterpay (acquired by Block), and Zip attracted hundreds of millions in investment and grew to tens of millions of active users by enabling interest-free installment payments at the point of purchase. BNPL credit losses increased in 2022-2023 as consumers took on more installment debt than they could manage. Affirm has stabilized its credit quality through more conservative underwriting and has resumed growth; Klarna confidentially filed for a US IPO in 2024.

Investment Technology

Investment technology fintechs include retail brokerage platforms, robo-advisors, and B2B trading infrastructure. Robinhood democratized commission-free stock trading and grew to 24 million funded accounts. Betterment and Wealthfront pioneered automated investment management (robo-advisory). Public and eToro expanded retail access to alternative assets including stocks, crypto, and alternative investments.

Robinhood’s revenue model shifted significantly after payment for order flow (PFOF) came under regulatory scrutiny. Robinhood now generates revenue from Gold subscriptions ($5/month for premium features), margin lending, credit cards, and options trading fees. Robinhood’s crypto business, through a UK acquisition, expanded its addressable market beyond US equities. Robinhood’s 2024 revenue of approximately $2.95 billion represented 58% growth as crypto trading volume recovered and the Gold subscription business scaled.

Insurance Technology

Insurtech, technology-driven insurance companies and distribution platforms, has experienced a difficult consolidation period. Lemonade, Root, Metromile (acquired by Lemonade), and others raised significant capital on growth-over-profitability strategies and suffered significant losses when insurance claim rates exceeded expectations. The insurance underwriting cycle proved more challenging than anticipated, and many insurtechs have retreated from direct underwriting toward distribution and technology services for traditional insurers.

Lemonade, the AI-powered insurance company, has reduced losses and improved underwriting quality but remains unprofitable. Root Insurance has exited several states to focus on profitable markets. The insurtech survivors have adopted more conservative underwriting approaches and are competing with traditional insurers on technology experience rather than pricing alone.

B2B Financial Infrastructure

B2B fintech, companies building financial infrastructure for other businesses, has been the most consistently profitable fintech segment. Plaid, which provides bank account connectivity for financial apps, was valued at $6.1 billion in its April 2025 funding round with significant revenue from API transaction fees. Marqeta, which powers card issuing programs for companies like Square and DoorDash, generates interchange-based revenue. Bill.com serves small business accounts payable and receivable with cloud-based financial workflows.

Embedded finance, integrating financial services into non-financial software products, represents the fastest-growing B2B fintech opportunity. Companies like Stripe Treasury, Unit, and Synapse enable software businesses to offer banking, lending, and payment features to their own customers. A construction management software company can offer project financing through Stripe Treasury integration without building bank relationships or obtaining financial licenses. This distribution of financial services through software creates massive addressable market expansion for B2B fintech infrastructure providers.

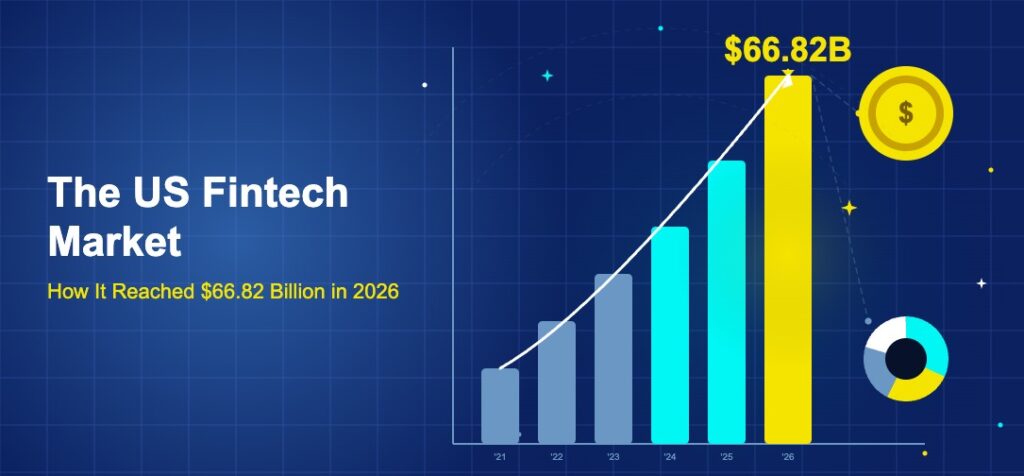

2026 Market Size Estimate

Projecting total US fintech revenue to 2026 requires aggregating across segments. Digital payments fintech (PayPal, Stripe, Block, Adyen US) is expected to reach $75-80 billion in combined revenue by 2026. Neobanking (Chime, SoFi, others) is expected to reach $10-15 billion. Lending fintech, recovering from the 2022-2023 contraction, is expected to reach $15-20 billion. Investment tech is expected to reach $8-12 billion. Insurtech and B2B infrastructure combined are expected to reach $20-25 billion. Total US fintech revenue in 2026 is therefore estimated at $66.82 billion, representing approximately 15% CAGR from 2024’s estimated $50+ billion.