In November 2022, Netflix set its opening advertising rate at $65 per thousand impressions, according to Adweek. That figure was not chosen to compete with digital display. It was chosen to compete with television. Netflix was pricing its new ad inventory at broadcast-level CPMs from day one, and it found buyers immediately.

The rate told the story plainly. The money that had sustained US television for sixty years was not disappearing. It was moving.

Television advertising lost more than $12 billion in US market share in 2025. Almost none of it came back.

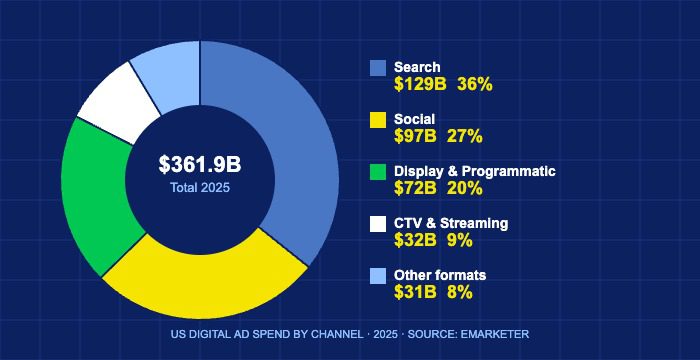

eMarketer‘s 2025 Digital Ad Spending forecast puts total US digital advertising at $361.9 billion for the year, a gain of $63.5 billion over 2024 and the largest single-year dollar increase the market has ever recorded. The United States accounts for 38% of global digital ad spend with 4% of the world’s population. That figure is the product of two decades of compounding: more devices, more platforms, lower entry costs, and a continuous expansion of inventory formats that did not exist a few years ago.

The 2025 number is not a ceiling.

Two decades without a down year

The $361.9 billion figure lands at the end of an unbroken expansion that started around 2005. eMarketer data shows the US digital advertising market at $12.5 billion in 2005, growing to $152.3 billion in 2020 and absorbing even the COVID contraction without recording a single annual decline. The compound annual growth rate from 2020 to 2025 sits at 18.9%, meaning the market roughly doubled every four years.

The structural driver is attention. Advertisers follow where audiences spend time, and American audiences moved their media hours from broadcast and print to digital platforms across the same two-decade window. Nielsen‘s Total Audience Report shows the average US adult spends more than 8 hours per day with digital media in 2025, up from 4.4 hours in 2010. Television still commands significant viewing time, but streaming now accounts for more than 40% of total TV consumption, and streaming inventory sells at digital CPMs, not broadcast rates.

Print’s collapse accelerated the reallocation. US print advertising fell from $46 billion in 2005 to under $9 billion in 2025 according to Statista‘s advertising revenue tracking. Direct mail, radio, and out-of-home each gave up share too. Every category that declined transferred budget to digital, and digital’s own structural growth added more on top.

Where the $361.9 billion goes

Search advertising leads the breakdown at approximately $129 billion in 2025. Google takes the majority, with Statista estimating Google’s US search revenue at $97.3 billion for the year. Microsoft’s Bing and its Copilot search integration account for most of the remainder, with Microsoft reporting double-digit growth in its search and news advertising segment across fiscal 2025.

Social media advertising reached approximately $97 billion. Meta’s platforms account for roughly $65 billion of that total according to eMarketer‘s channel breakdown. TikTok added approximately $12 billion in US ad revenue before regulatory uncertainty disrupted its operations late in the year. YouTube contributed $13.4 billion, classified within Google’s advertising revenue line.

Display and programmatic advertising, covering banner ads, video pre-rolls, and native placements bought through automated exchanges, reached approximately $72 billion. The IAB‘s Internet Advertising Revenue Report attributes most of the category’s growth to video inventory, which commands higher CPMs than static display and now accounts for the majority of programmatic dollars.

Connected TV and streaming advertising generated approximately $32 billion. Netflix, which launched its ad-supported tier in late 2022, reported 40 million monthly active users on that tier by early 2025. Hulu generated an estimated $5 billion in US ad revenue. Smaller streaming platforms, including Peacock, Paramount+, and Max, collectively added another $6 billion.

Three forces that drove 21% growth in 2025

The 21% year-over-year growth rate exceeded analyst expectations entering the year. Three forces explain the acceleration.

Small business participation widened the total addressable market. Meta reported more than 10 million active advertisers on its platforms in 2025, the majority running campaigns under $10,000 per year. Influencer Marketing Hub‘s 2025 Small Business Advertising Report found that 67% of US small businesses with annual revenue under $1 million ran digital advertising campaigns in 2025, up from 51% in 2022. The entry cost fell sharply, a pattern we covered in our look at technology and marketing strategies for local businesses. Google Search accepts budgets from $1 per day. Meta’s minimum is $5. A business with no prior advertising history can now run a national campaign for the cost of a weekly lunch.

AI-driven performance improvements justified larger budgets. Google’s own performance data shows Performance Max campaigns generated 18% higher conversion rates than manually managed campaigns in 2025. Meta’s Advantage+ shopping campaigns reduced cost per acquisition by an average of 17% for e-commerce advertisers. When returns improve, advertisers allocate more, and both platforms saw average revenue per advertiser rise in 2025.

New inventory formats created spending that did not previously exist. Podcast advertising exceeded $4 billion in the US in 2025 according to the IAB‘s Podcast Advertising Revenue Study. In-game advertising, augmented reality placements, and digital out-of-home screens added another $8 billion collectively. GroupM‘s 2025 Advertising Investment report projects these emerging formats will exceed $45 billion in combined US spending by 2027.

What $361.9 billion means for operators

The scale of the market creates specific implications for businesses operating within it. Companies that buy advertising consistently hold structural advantages over those that buy sporadically. WARC‘s 2025 Marketer’s Toolkit found that brands with consistent full-year digital ad presence generated 23% higher return on advertising spend than brands that concentrated budgets in short seasonal windows. Continuity produces compounding data benefits that periodic campaigns cannot replicate.

Platform concentration is a genuine operational risk. Google and Meta together accounted for approximately 53% of total US digital ad spend in 2025 according to eMarketer. That means changes to targeting policies, auction mechanics, or platform algorithms at either company directly affect more than half of all digital advertising in the country. Amazon’s advertising segment, which grew 19% to $50.7 billion globally in 2025, is the most credible challenger to that concentration, though its US advertising remains concentrated in retail search inventory.

For advertisers outside the top-spending tier, the data shows a consistent principle: format diversification reduces CPM volatility. Brands running campaigns across three or more channels in 2025 paid an average CPM 14% lower than brands that concentrated all spending in a single platform, according to Nielsen‘s Cross-Platform Advertising Report.

The pressure points ahead

The scale of the market has drawn regulatory attention that could alter its structure. The Department of Justice’s antitrust case against Google’s advertising technology business, which went to trial in 2024, is expected to produce a ruling that could require structural separation of Google’s ad buying, selling, and exchange operations. A forced divestiture of Google Ad Manager would change the economics of programmatic display for every publisher and advertiser using the system.

The American Privacy Rights Act, if passed in its current form, would restrict behavioral targeting in ways that reduce the precision of audience-based buying. Several states have enacted digital advertising taxes. GroupM models a scenario where combined regulatory changes reduce US digital ad market growth by 3 to 4 percentage points annually through 2027, though its base case still assumes expansion.

GroupM‘s 2026 forecast, published in December 2025, projects US digital ad spending at $418 billion in 2026. eMarketer projects $407 billion. The gap between the two estimates reflects regulatory uncertainty rather than disagreement about underlying demand.

Advertisers follow audiences. American audiences are spending more time on digital platforms every year, and that attention is what the $361.9 billion is ultimately purchasing.

According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020.

Market analysis from Grand View Research projects that technology-driven market segments will continue expanding at compound annual growth rates between 15 and 25 percent through the end of the decade.