Ninety-three percent. That is the share of more than 3,200 web3 gaming projects now classified as effectively dead — a figure published by market analysts Caladan and reported by CoinDesk in April 2026. The average lifespan before a project’s token loses 90% of its value and daily users fall below 100: four months.

The best-known failures put names on those numbers. Axie Infinity’s Smooth Love Potion token hit roughly $0.40 in mid-2021 while the game was pulling 2.7 million daily active users. By mid-2022, SLP had surrendered more than 99% of that peak value and daily active users had collapsed to a fraction of their former level. STEPN’s GST reward token traced an almost identical arc — $8.51 in April 2022, then a 98% wipeout in the two months that followed. Three years on, the cycle repeated at a larger scale: Hamster Kombat accumulated 300 million registered players by summer 2024, then lost 259 million of them within three months of its token launch that September.

Different names, different years, the same structural failure. This is not a post-mortem about hacks or regulatory bad luck. It is an analysis of what first-generation play to earn crypto tokenomics got fundamentally wrong — and why a properly engineered deflationary token model represents a structural fix, not a marketing spin.

The Infinite Mint Problem That Killed First-Gen P2E

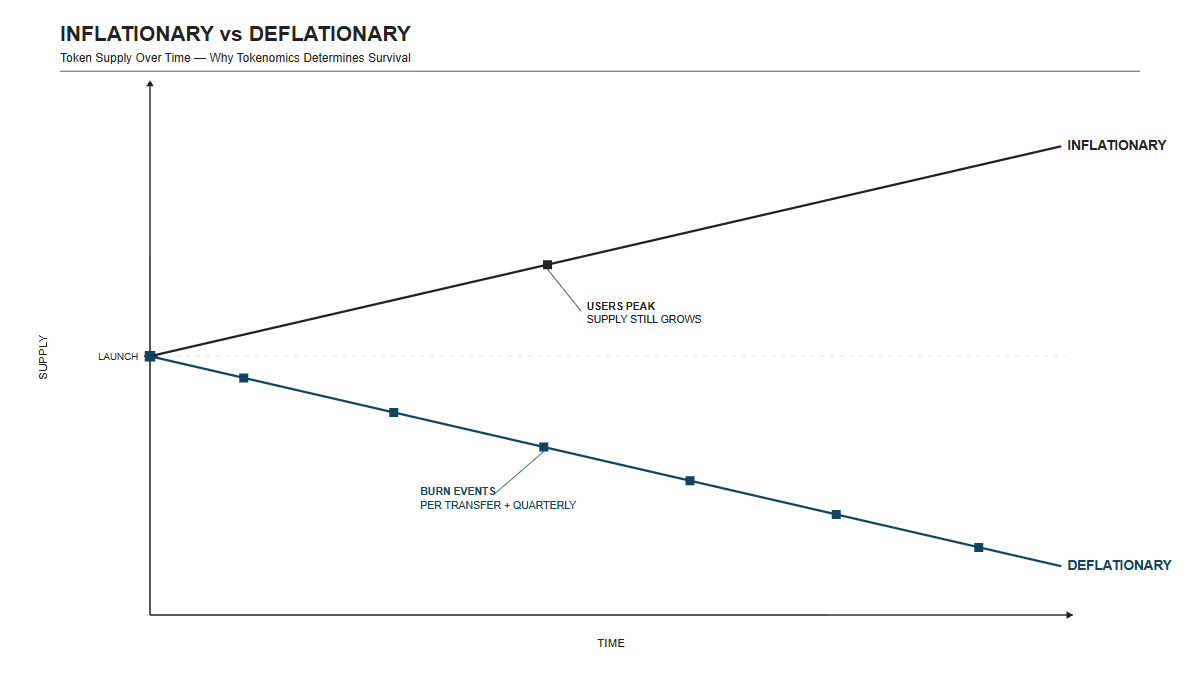

First-generation P2E failed for a single structural reason: in-game reward tokens had no effective supply ceiling.

Every match played in Axie Infinity produced SLP. Every walk logged in STEPN produced GST. Both tokens were freely tradeable on open markets. The more users joined, the more tokens were minted; the more tokens were minted, the greater the sell pressure; the greater the sell pressure, the lower the per-token USD value; the lower the value, the less players earned. At that point, new player inflows — the only remaining demand source — had to continuously outpace existing player sell pressure just to keep the price stable.

Analysts have labeled this the “Ponzi flywheel” pattern: a mint-to-earn loop that is mechanically solvent only while user growth is accelerating. The moment growth plateaued, token supply continued expanding into a shrinking buyer pool. Axie’s SLP reportedly saw four times more tokens created daily than burned at peak. There was no structural drain. Axie Infinity has approximately 8,810 active players today — down from 2.78 million at peak. The token economics did not merely crash the price; they hollowed out the game entirely.

What a deflationary token is: A deflationary token is one where the circulating supply decreases over time through permanent, on-chain burns — removing tokens from circulation in a way that cannot be reversed, so that demand pressure can meaningfully affect price even as user behavior stabilizes.

The contrast with inflationary reward tokens is structural, not cosmetic. Inflationary tokens punish patience: the longer you hold, the more supply dilutes your position. A well-designed deflationary token does the opposite — and the difference in outcome, as first-gen P2E demonstrated at scale, is not marginal.

What Is a Dual-Token Economy — and Why Does It Protect Exchange-Listed Token Value?

A dual-token economy separates in-game reward currency from the exchange-traded token, shielding tradeable supply from uncapped in-game emissions.

This is the architectural separation that Axie Infinity failed to implement correctly. AXS and SLP were both listed on open markets. When SLP supply exploded, sell pressure hit the exchange directly, with no firewall between the in-game economy and the secondary market. Players who earned SLP could sell it immediately and freely — which is what most of them did, because the game’s design gave them no incentive to hold.

A properly designed dual-token system makes the in-game currency non-tradeable on exchanges by default. It can only be spent in-game or converted into the exchange-listed token under strict, capped conditions. The in-game economy generates tokens as freely as it needs to — but those tokens cannot reach the market until they pass through a controlled gateway. The exchange-listed token’s supply — SFDT in SkyFleetDash’s case — is managed independently of how many races anyone ran today.

How SkyFleetDash’s Burn-First Design Addresses the Root Cause

SkyFleetDash‘s dual-token design blocks in-game GC from inflating SFDT supply — solving the hyperinflation flaw that sank first-gen P2E.

The platform runs two currencies:

- GC (GameCoin) — earned in multiplayer race winnings. Non-tradeable on exchanges. Can only be spent in-game or converted to SFDT through a gated pathway.

- SFDT — the native, exchange-listed token. Fixed total supply of 1 billion. Every SFDT transfer, trade, or conversion triggers an immutable 2% automatic burn that permanently removes tokens from circulation.

The Conversion Gate

The GC-to-SFDT conversion gate has hard controls built into the protocol: players must hold an account at least 7 days old, complete a minimum of 10 multiplayer races, pass KYC Tier 2 identity verification, and convert within tiered daily caps by player rank. A global daily conversion pool is capped at 0.1% of circulating SFDT supply — meaning the rate of in-game earnings that can ever reach the exchange is structurally bounded, regardless of how many players are active.

On top of the per-transfer burn, quarterly burn events are planned throughout the year, adding additional scheduled supply reduction pressure beyond day-to-day transaction burns.

SkyFleetDash is a BNB Smart Chain-based play-to-earn space-racing platform with a fixed 1-billion SFDT supply, an immutable 2% per-transfer burn tax, a dual-token economy designed to prevent in-game emissions from flooding the exchange-listed token supply, and a SkyFleetDash presale ahead of a Q3 TGE.

First-Gen P2E vs. Deflationary Dual-Token Design: A Structural Comparison

Deflationary dual-token architecture outperforms the first-gen P2E model on every dimension that determines long-term token sustainability.

| Design Feature | First-Gen P2E (Axie/STEPN Model) | Deflationary Dual-Token (SkyFleetDash) |

|---|---|---|

| Reward token supply | Uncapped; minted per gameplay event | Fixed 1B SFDT; no further minting |

| Burn mechanism | None or negligible relative to emission rate | 2% immutable per-transfer burn + quarterly burn events |

| In-game / exchange token separation | Weak; SLP and GST freely tradeable on open markets | Hard separation: GC non-tradeable; SFDT exchange-listed |

| Conversion rate controls | Minimal; open to all active players | Tiered daily caps per rank; KYC Tier 2; global 0.1% pool cap |

| Player incentive model | Earn-to-sell; early players exit into new entrant capital | Skill-based competitive racing; staking APY 25%–5% dynamic |

| Smart contract security | Varied; notable incidents across the category | CertiK-audited |

| Treasury governance | Largely opaque or unprotected | 3-of-5 multisig Reserve Fund; milestone-gated Development Fund; monthly transparency reports |

| Token allocation lock | Not standard | Token allocations will be locked on Team Finance or UNCX at exchange listing |

Why Skill-Based Competition Creates Natural Supply Pressure

Skill-based competition limits supply emissions in a way flat earn-by-playing mechanics never could.

When a player’s earnings depend on finishing ahead of other players in a competitive race, the earn mechanism is self-limiting by design: only winners collect Earned GC at the race’s conclusion. In contrast to passive P2E models where every participant earns by showing up, competitive racing redistributes GC between participants rather than printing net new GC into the ecosystem at a fixed-per-session rate.

SkyFleetDash’s tournament structure tiers wagering by player rank — from 500 GC per race for new players up to 50,000 GC for VIPs. A portion of tournament entry rake flows to platform revenue rather than being fully redistributed to players, creating a natural ongoing drain from the GC pool. Combined with the 2% SFDT burn triggered on every conversion from GC to SFDT, the architecture has simultaneous contraction pressures at multiple points in the economic loop — something neither Axie Infinity nor STEPN was designed with.

This framing matters for analysts evaluating any play to earn crypto project: the earn mechanism in competitive P2E is not “print tokens as long as the player is logged in.” It is “redistribute stake between players while the protocol extracts a deflationary toll at each conversion point.”

Can a Deflationary GameFi Crypto Project Actually Scale Without Repeating History?

The burn mechanism solves the supply side. The demand side — whether enough people genuinely want to play — determines whether any P2E project, deflationary or not, builds lasting value.

SkyFleetDash addresses this with gameplay depth that extends well beyond the earn loop. Built as a deflationary play-to-earn game rather than a passive-earn product, its core activity spans five modes:

- Real-time competitive multiplayer racing

- Sky Tracks — a custom track creation system where players build, own, and monetize racing environments via Sky Passes

- Asset Creator — a 3D design tool for building and tokenizing in-game items

- Peer-to-peer Marketplace for trading assets

- Esports-format Galactic Racing Leagues with SFDT prize pools

Rare items and racing livery are available as on-chain NFT assets; spacecraft are fully customizable for performance and appearance. Cross-chain integration spans 10 blockchains, with BNB Smart Chain as the primary chain.

The staking layer adds a holding incentive with staying power. SFDT staking begins at 25% dynamic APY when total staked supply is below 10 million tokens and self-corrects down to 5% as staking grows above 200 million — a rate that rewards early participants without locking the project into unsustainable yield commitments. Lock-period bonuses add up to +8% for 12-month commitments, rewarding long-horizon holders rather than liquid sellers.

The game testnet launched in February 2026 and mainnet deployed in March 2026. A playable build is available for hands-on press review at game.skyfleetdash.com, and the community currently counts 11,000+ members. The platform’s own DAU target is 10,000 active players by Q3 2026 — honest numbers, not speculative projections.

What remains unproven is what always remains unproven at this stage: whether the gameplay loop is compelling enough to retain users once the presale narrative is no longer the primary draw. That is the actual test, and it begins with open beta ahead of the Q3 TGE.

The SkyFleetDash Presale: What Early Entry Looks Like in a Deflationary Model

In a deflationary model, early presale entry carries different risk/reward math than the earn-and-sell loop that drove first-gen P2E collapses.

In an inflationary model, early investors’ upside depends on new player inflows continuing to create buy pressure. The economics are explicitly downstream-dependent. In a deflationary model with a fixed supply and per-transaction burns, supply pressure works in the opposite direction over time — which changes the significance of round position.

The SkyFleetDash presale runs three rounds, each with a smaller discount off the $0.10 public launch price:

- Round 1 — 50% discount; BEP-20 USDT only

- Round 2 — 40% discount; BNB and BUSD added

- Round 3 — 30% discount; BNB and BUSD available

Tokens unlock 20% at TGE (targeted for Q3), with the remaining 80% releasing monthly over four months — fully vested five months post-TGE. Per-wallet entry runs from a $50 minimum to a $25,000 maximum. Round 1 opening will be announced by the community.

The project has already completed a private allocation phase — approximately 17 million SFDT placed with strategic backers ahead of the public rounds — alongside a completed CertiK audit. The initial circulating supply at TGE is approximately 135 million SFDT, implying an initial market cap of ~$13.5 million at the $0.10 public launch price, against a fully diluted valuation of $100 million.

For analysts evaluating whether a play to earn crypto project has genuinely solved what first-gen P2E broke, the structural checklist is short:

- Fixed supply — no further minting after launch

- Immutable per-transfer burn — protocol-enforced, permanent supply reduction

- Dual-token separation with hard conversion gates

- A gameplay model that does not require perpetual user growth to stay economically solvent

SkyFleetDash is designed around all four. Whether that design sustains under live conditions is what Q3 will begin to answer — and the presale discount structure reflects the risk that question still carries.