SQL is the unglamorous lingua franca of finance. Almost every meaningful U.S. financial dataset can be queried with SQL, almost every analyst can write it, and almost every regulator can read it. The interesting questions are no longer about whether to use SQL but about how to use it responsibly inside systems where the wrong query can lock a production ledger or the wrong join can produce a report that misleads a supervisor.

This piece sets out where SQL belongs in U.S. financial systems, the patterns that make SQL useful in regulated environments, the specific traps that teams fall into when they treat SQL as a casual tool, and the discipline that distinguishes mature financial SQL practice from the adventure-driven version.

The single biggest cost in financial SQL

The single biggest hidden cost in financial SQL is silent data drift. The query that worked yesterday may return different results today because an upstream system added a new transaction type, an account flag changed semantics, or a previously empty field started carrying meaningful values. The query did not change. The data behind it changed. The result is a slow erosion of trust in the analytical output, with no individual mistake to point to.

The discipline that addresses this cost is column-level lineage and consistent reference data. Mature financial SQL environments treat lineage as a first-class concern, with tooling that traces every column in every report back to its source and notifies the report owner when anything in the lineage changes. The institutions that invested in this tooling early have an analytical environment that they can defend to their boards. The ones who did not are still arguing about why two reports show different numbers for the same metric.

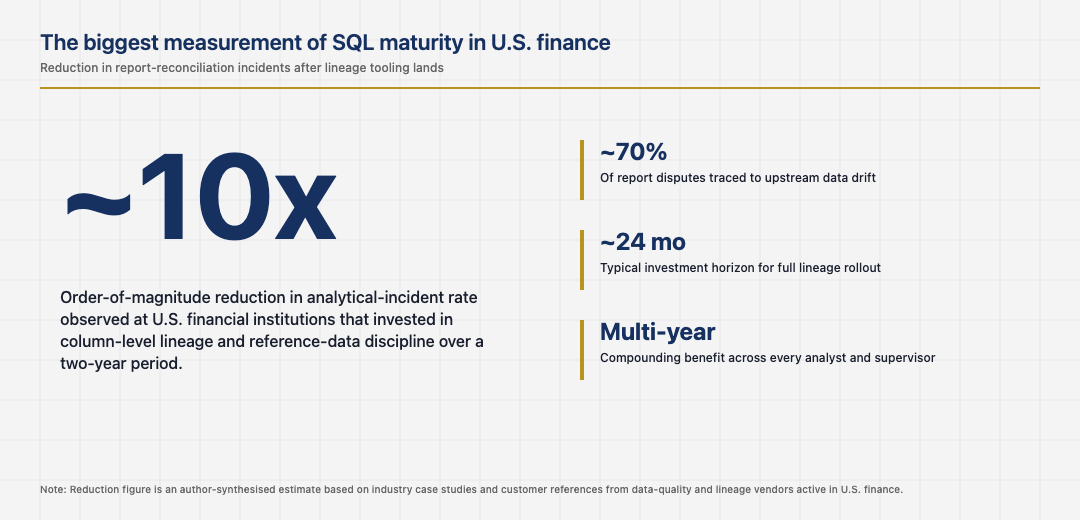

The biggest stat that captures the SQL maturity gap

The mature operators report a step-change reduction in report-reconciliation incidents once their lineage tooling and reference data discipline are in place. The numbers vary, but the pattern is consistent: institutions that invest in this layer reduce their analytical-incident rate substantially, often by an order of magnitude over a two-year period. The investment is significant. The benefit accumulates across every analyst who relies on the data and every supervisor who reads the resulting reports.

Read-only practice and the production database

The clearest line in mature financial SQL practice is between read-only access to production data and any access that can mutate state. Analysts, regulators, and product managers should be able to read production data freely, with appropriate access controls and audit logging, but should not be able to modify it. Mutations happen only through services that enforce business rules, idempotency, and authorisation.

The institutions that respect this line keep their production ledgers safe from analytical mistakes. The institutions that allow ad-hoc updates against production usually have a small number of horror stories that informed their later decision to enforce the line. The mature operators learned the lesson once and codified it through tooling. The newer operators learn the lesson again, sometimes more than once, and the cost is paid in customer-visible incidents that the analytical team did not intend to cause.

Performance discipline matters more than query elegance

Pretty SQL queries are a pleasure to write and a problem in production. The query that runs cleanly on a small dataset may behave very differently on the production scale, and the difference often shows up as a query that holds a lock for longer than the application can tolerate. The mature financial SQL practice treats query performance as a first-class concern: explained query plans for non-trivial queries, statistics maintained on critical tables, indexes designed for the actual access patterns, and load-tested validation before any new query reaches production.

The teams who treat performance as something the database engine takes care of usually find their production database telling them otherwise at exactly the wrong moment. The teams who treat performance as their own responsibility stay ahead of the curve. The discipline is not difficult, but it requires attention that competes with feature work, and the institutions that protect that attention have measurably more reliable financial systems than the ones who do not.

The next decade of SQL practice in finance

SQL is not going away in U.S. finance. The next decade will see SQL increasingly written by AI assistants, refined by humans, and audited by lineage tooling that continues to mature. The value of SQL as a contract between analysts, regulators, and engineering teams will only grow, because it is the one language that all three can read fluently. The institutions that treat SQL practice as a discipline worth investing in will compound their analytical advantage over the institutions that treat it as a developer-tools problem.

Read across the full picture, SQL for U.S. finance in 2026 is a mature practice with specific disciplines that distinguish strong implementations from weak ones. Column-level lineage, reference-data discipline, strict separation between read-only and mutating access, and serious attention to query performance are the patterns that compound. The institutions that respect them write SQL that ages well and supports analytical decisions that survive scrutiny. The institutions that miss any one of them produce SQL that works in the moment and creates problems later, often at the inconvenient moment when a supervisor is reading the output.

Looking back across the full sweep makes one final point clear. The American financial system has accumulated its strength through the patient layering of standards, institutions, and supervisory expectations on top of an active commercial layer. The application layer captures attention because it is visible and fast-moving. The institutional layer captures durability because it is invisible and slow-moving. Operators who learn to read both layers at once tend to outlast operators who only read the visible one, and the discipline of doing so is not glamorous but it is the discipline that consistently shows up in the firms that compound through multiple cycles instead of just the one they happened to start in.

The same lesson shows up in the founders who quietly build through down cycles that catch the louder ones flat-footed. Reading the institutional rebuild as carefully as the product roadmap is what separates the long-lived operators in 2026 from the ones whose names appear only in retrospectives. The competitive position of the next decade will turn less on the surface features that draw press attention and more on the structural features that draw supervisory attention. The two are increasingly the same set of features, and the operators who recognise that early are the ones who position correctly while the rest are still arguing about whether the rules apply to them.

One last consideration is worth carrying forward. Cross-cycle perspective sharpens any single decision. Looking at how peer ecosystems have handled the same question, what they got right and where they stumbled, almost always reveals something about the decisions that the U.S. system is in the middle of making right now. The operators who travel intellectually as well as commercially tend to make better forecasts about which infrastructure layer will matter most in the next phase, and which segment is being quietly reset under the noise of the daily news. The disciplined version of that practice is what the next ten years of American FinTech will reward most consistently.