Complicated regulations. Vacillating customer loyalty. Unconventional competitors. The banking sector is in a state of flux, indeed.

A century ago, bankers would have met their clients and met their customers behind closed parlor doors. Today, banks are in a rush to digitize their operations. Bank branches are but formal physical offices maintained for documentation and the rare customer who walks in for personal support. A large chunk of the banking transaction is happening online. That makes it imperative for banks to rewire their customer experience.

This is the age of mobile apps, digital wallets, and chatbot-assisted banking. Even ‘Artificial Intelligence (AI)‘ is penetrating deep into banking operations along with other new-age technologies, like blockchain. That brings with it a host of challenges and opportunities.

Here is a brief take on how banks can overcome the challenges and seize the opportunities to reinvent the customer experience.

Automation for Repetitive Processes

There are several processes in the banking services that can be automated to reduce manual intervention. Take, for example, KYC compliance. Until automation happened, customers had to submit physical copies of their personal identification documents to open a new bank account, transfer the account, apply for a loan or credit card, and so on.

Due to the sheer volume of transactions and the threshold of manual productivity, these processes were time-consuming. Not to miss mentioning the errors that further delayed the approval process. With automation, these processes can be processed in a flash, cutting down the time taken from days or weeks to few hours. Automation can scan through personal identification documents, use optical recognition, and similar tools to quickly capture an applicant’s information and feed it into the bank’s records for processing or approval.

Conversational Banking

One thing that remains constant in the analog era, as well as in the digital era, is the need for conversations. Customers always have the urge to talk to someone and get direct information, especially on sensitive matters like bank account balance, banking services, loans, credit cards, and so on.

But, that takes us back to the challenge of shortage in staffing to handle the volume of transactions. It is here that conversational banking can help. An AI-based chatbot that can mimic the conversation style and tone of a human agent or even a live chat software can smoothen things for banks.

For instance, live chat software can help customers who land on the bank’s website choose from a variety of services. It can offer them FAQs on making a wire transfer, information on the latest schedule of charges, report lost cards, and so on.

For complex queries that the chatbot or the live chat software is unable to provide a resolution to, a ticket can be raised to loop in a human agent.

Now a live chat software is something that online stores and other B2C websites have been using until now. For banks, it can prove to be beneficial in many ways.

For example, live chat software can be used to upsell or cross-sell new banking and financial products to existing customers based on their customer segment. It can be used as a lead generation tool without the need for manual intervention. It saves employee costs and also helps boost the bank’s earnings indirectly.

Banking on the Go with Mobility

Ever since mobile apps have become the go-to source for cab-hailing and coffee-ordering, customers have become habitual in terms of expecting the same mobility for all their utility services, including banking. Banks have quickly realized that the millennial generation of customers not only take online banking seriously but also want a similar, if not better, mobile banking experience.

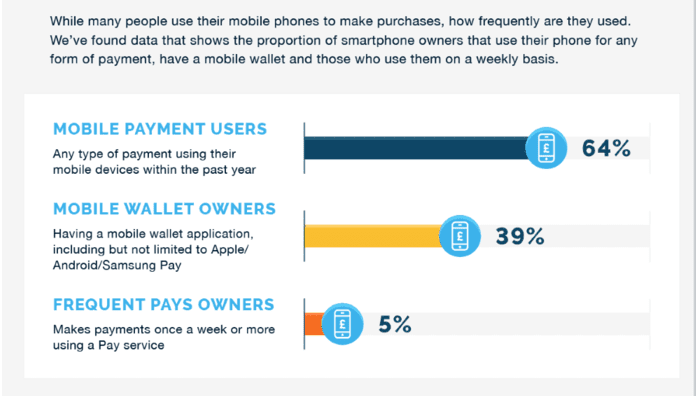

The rise of mobile payments using digital wallets is a testament to this fact. According to Merchant Machine, at least 64% of users use digital wallets to make any kind of payments using their mobile devices.

Right from paying for groceries to paying the cab fare, these digital wallets are used for multiple purposes, which were taken care of by plastic cards earlier. In other words, banks that want to upgrade their customer experience must invest in dedicated mobile apps that allow users to manage and use their money easily.

Offer the Convenience of Self-Service

In addition to the facility of mobility, mobile apps can also act as mediums for self-service. According to Silvercloud’s The State of Banking Self-Service 2019 survey report, 59% of surveyed banks and credit unions report that consumer self-service is very important at their institution.

Self-service is quick, convenient, and offers the best-personalized service as possible. Nobody other than the customer can know what they want and how they want it. However, customers do need some kind of assistance or direction to find the service that they are looking for.

Transparency in Operations

The great depression that lasted between 2007 to 2009 must not have faded away from the memories of many. Or at least not from the millennial generation that had just graduated into an economy where job cuts and unemployment were rampant. As a result of that depression, which was onset by the unfair trade practices of banks and financial institutions, the level of trust that customers have on banks has receded.

The customers of today are willing to switch to new-age banking institutions if the centuries-old one that their parents were using is not transparent about how account holders’ money is being handled.

Fortunately, technologies like Blockchain are offering a better way of ensuring transparency in managing banking operations. The immutable ledger concept that blockchain introduces will help banks prevent the creation of a monopoly. Also, it democratizes information by making data available to all relevant stakeholders. As a result, a few powerful bankers would not be able to call the shots at their customer’s expense.

The end result would be elevated customer experience as customers have renewed trust in banking transactions. Needless to say, customer trust results in long-term relationships — something which every bank is striving to achieve. Account-holders who keep deposits with the bank for the long-term gives the bank enough buffer to issue new loans to borrowers. Ultimately, it results in more revenue streams.

Takeaway

Banking is perhaps one of the oldest and most sophisticated sectors in the history of mankind. In recent age, the role of banks has changed from being a custodian of money to facilitators of economic transactions. Today’s customers expect banks to provide a lot more than traditional services.

They expect customer experiences that they have been habitual to by online stores and on-demand services. The banking sector needs an overhaul of its approach to customer service to retain its customers and to win new ones.