A market-data packet leaves a Nasdaq matching engine in Carteret, New Jersey, traverses a tightly tuned cross-connect, hits a co-located trading server, runs through a risk check and a decision model, and a new order returns to the exchange in single-digit microseconds. That round trip is the unit of competition in US equity markets in 2026, and the firms that have shaved another fraction of a microsecond off it are still the ones taking share at the lit venues.

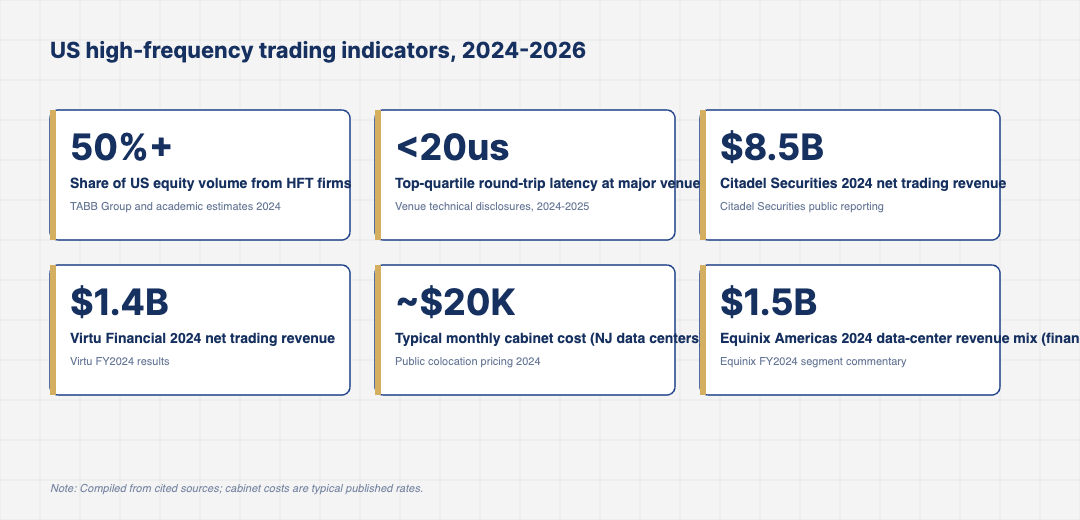

High-frequency trading remains the single largest source of liquidity in US equities, with the leading market makers accounting for more than half of consolidated volume in any given week. The dollars at stake have not shrunk despite years of compression. Citadel Securities reported $8.5 billion in net trading revenue in 2024, per the firm’s public commentary; Virtu Financial reported $1.4 billion in net trading revenue for the same year. The systems and the people who run them have continued to attract investment that looks more like semiconductor design than like traditional finance technology.

Latency Budgets Are Now Measured in Nanoseconds

Round-trip latency at top-quartile US venues now sits in the high-single-digit microseconds for the leading proprietary trading firms, with intra-host latency budgets discussed in nanoseconds. The path from market-data ingest to order send is decomposed into a sequence of latency contributors: NIC offload, kernel bypass, ring buffer access, decision logic, risk check and serialisation. Each stage has been re-engineered repeatedly over the past decade, and the marginal improvement per dollar has narrowed considerably.

That narrowing has changed the nature of the engineering work. Where the early HFT era was about basic FPGA-accelerated tick-to-trade pipelines, the current era is about co-designed systems where hardware, network and application converge on a single goal: deterministic, low-jitter execution at high throughput. Firms still hire kernel and FPGA specialists in significant numbers, and the cost of attracting that talent has continued to climb even as some of the broader trading-technology hiring has cooled.

Vendor consolidation has also become a visible part of the story. The number of independent tick-to-trade hardware and software vendors has shrunk over the past five years, with the surviving suppliers offering deeper, more integrated stacks. Trading firms that previously assembled best-of-breed components from many vendors now lean more on integrated platforms, which reduces engineering surface area at the cost of some flexibility. The trade-off plays out differently at each firm depending on the size and seniority of its internal systems team.

Co-Location Is Where the Physical Market Lives

The economic reality of US equity HFT is that the meaningful action takes place inside a handful of data centres in New Jersey, where the major exchanges run their matching engines. Equinix’s NY4 and NY5 facilities, alongside CyrusOne’s Carteret site and others, host the cabinets where the leading trading firms physically place their servers. Equinix’s FY2024 segment commentary highlights the continued importance of financial-services tenants to its Americas revenue mix.

Typical cabinet rental at these facilities runs into the tens of thousands of dollars per month, with cross-connect fees and bandwidth costs on top. For a serious HFT operation, the all-in physical infrastructure spend in a single NJ data centre can run well into the millions per year. That cost is justified only because the alternative, executing from outside the venue, leaves microseconds on the table that competitors will not.

Microwave and millimetre-wave links between New Jersey and Chicago, which carry index futures and ETF prices between the two main US trading centres, remain a real source of advantage. The leading firms invest in private spectrum, tower height and weather-resilient design to keep these links operating during conditions that knock less-engineered competitors offline. The difference is rarely visible outside the trading floor but it shows up in the firm-level P&L on volatile mornings.

Market Microstructure Has Shifted, but the Edge Persists

Decimalisation, Reg NMS, dark pools, periodic auctions, retail wholesalers, payment-for-order-flow rules, and a steady stream of SEC market-structure proposals have all reshaped where and how US equities trade over the past two decades. The HFT firms that have stayed at the top of the league tables are the ones that adapted their strategies to each microstructure change rather than betting on a single mechanism continuing forever.

The current attention is on lit-versus-dark routing, mid-point liquidity and the role of retail wholesalers. The SEC’s ongoing review of order-handling rules has the potential to reshape execution economics, particularly for the largest wholesalers. The HFT firms that have invested in multi-venue routing intelligence and that can execute equally well against retail flow, institutional flow and pure displayed liquidity are positioned to absorb whatever rule changes ultimately emerge.

The economics of payment for order flow continue to drive a meaningful share of the leading market makers’ revenue, particularly for retail-wholesaling operations. Any change to that economics would reshape the competitive landscape quickly, which is why the SEC’s deliberations on order-handling rules attract such intense attention from the affected firms. The outcome of that process will likely set the tone for how US equity market structure evolves through the rest of the decade.

The Buy Side Is Building Its Own HFT-Adjacent Capability

Quant hedge funds and some of the larger asset managers have spent the past decade building execution stacks that look increasingly similar to dedicated HFT firms. Two Sigma, DE Shaw, Renaissance and Citadel’s investment business all operate execution algorithms that consume the same market-data feeds, run on similar co-located hardware and care about the same microsecond-level distinctions as the pure market makers.

The difference is purpose. The buy-side execution stack exists to implement an underlying investment view at minimum market-impact cost. The pure HFT market-maker stack exists to capture spread and short-term flow imbalance. The technology overlap is significant but the operating models, risk frameworks and economic models diverge. Both sides continue to invest heavily in systems and people, which has kept the broader US trading-technology labour market tight even as other corners of finance have cooled.

Where the 2026 HFT Spend Is Concentrating

Three areas absorb most of the new investment at major US HFT firms in 2026. The first is hardware acceleration, where FPGA pipelines, custom NICs and increasingly ASIC-based logic continue to push tick-to-trade latencies lower. The second is data engineering, where the storage, retrieval and replay of high-resolution market-data archives supports both research and live operation, often at petabyte scale. The third is risk and surveillance, where regulators have made it clear that pre-trade controls and post-trade reconstruction need to be at least as fast and reliable as the trading itself.

None of these investments produce a marketing moment, and most of the work happens out of view. They show up in net trading revenue, in the share of price improvement delivered to retail brokers and in the willingness of new exchanges and venues to give the largest market makers preferential connectivity arrangements. The firms that compound those investments across the next 24 months are the ones that will hold their share as the next round of microstructure rule changes lands, and they are also the most likely buyers of any specialist HFT shops that exit the segment.

For operators and investors tracking US high-frequency trading through 2026, the practical signal is to watch order-to-trade ratios at the top venues, the latency disclosures that exchanges publish in their technical bulletins and the headcount mix at the leading firms, because those three together will explain which operators are widening the edge and which are quietly losing it.

The longer-term outlook is that the HFT segment continues to consolidate around a small number of very large, capital-intensive firms with deep systems engineering benches, while specialist niches in options, futures, ETFs and Treasuries continue to support a long tail of smaller proprietary shops that compete on signal sophistication rather than raw speed.