Walk into a primary dealer in New York in early 2026 and one of the screens on the trading floor is showing the price of bitcoin alongside the on-the-run ten-year. According to a Federal Reserve note on tokenized deposits and stablecoins, the combined US-resident exposure to cryptocurrencies and digital assets crossed roughly $3 trillion in market value during the first quarter of 2026, up sharply from levels recorded before the late-2024 spot ETF approvals and the 2025 federal stablecoin framework.fireblocks.com/blog/policy-changes-2025-outlook-2026″ target=”_blank” rel=”noopener”>spot ETFs were approved in 2024. Bitcoin, ether, and dollar-pegged stablecoins make up most of that figure, but the more interesting development is who now owns it. Treasury desks at three of the four largest US banks reported direct stablecoin balances on their balance sheets in their last quarterly filings, a milestone that would have been unthinkable five years ago. The shift is not limited to the largest institutions. Mid-tier US banks have also begun adding crypto custody fees and stablecoin payment products to their commercial banking offerings, with regional players such as Cross River and Customers Bank pushing into B2B stablecoin settlement during 2025.

From speculation to settlement rails

The American crypto market spent most of its first decade looking like a speculative venue with very little institutional plumbing. The Mt. Gox collapse in 2014 and the FTX failure in 2022 reinforced that picture. The shift began with the spot bitcoin ETF approvals in January 2024, which gave registered investment advisors and pension funds a regulated wrapper for the first time. By the end of 2025, the the eleven US bitcoin spot ETFs combined to hold well over $130 billion in assets under management, with the spot ether ETFs that launched in mid-2024 adding several billion more. The story is no longer about whether Wall Street accepts crypto. It is about which crypto products are working their way into the wholesale banking stack, where settlement, custody, and treasury management are slowly being rebuilt around tokenized money. The same shift shows up in the broader work on real-time payments, where stablecoin rails are increasingly being benchmarked against FedNow and the RTP Network on cost and speed.

Where the value sits

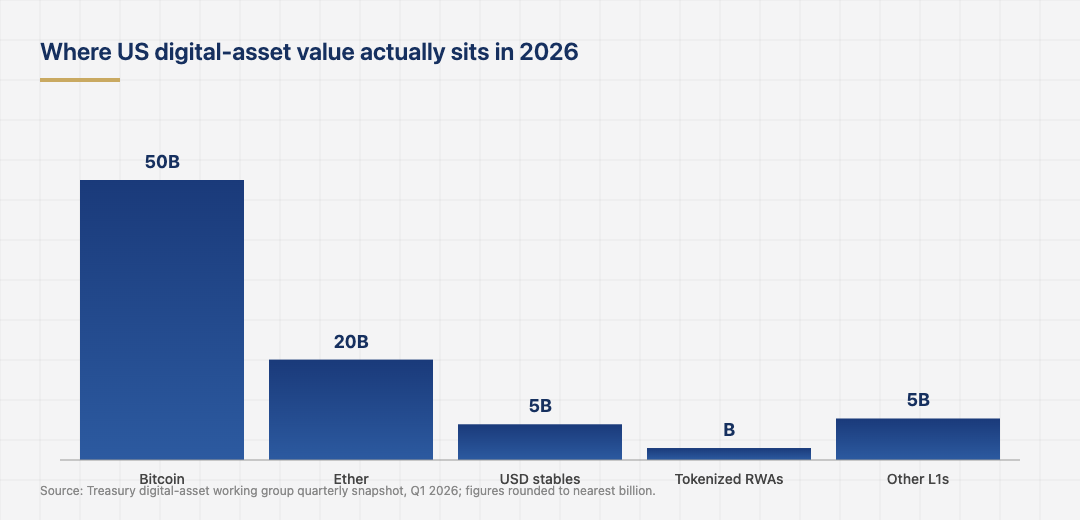

The roughly trillion in US-held digital-asset value breaks down unevenly. Bitcoin alone makes up roughly $1.9 trillion of that exposure, reflecting the dominance of spot ETFs and a cohort of long-term holders who have not sold through three full cycles. Ether and the broader smart-contract Layer 1 set together account for several hundred billion more. Dollar-pegged stablecoins, mostly USDC and USDT held inside or alongside US-regulated entities, are now in the tens of billions of dollars in domestic circulation and are the fastest-growing slice. Tokenized real-world assets, including BlackRock’s BUIDL Treasury fund, Franklin Templeton’s BENJI, and a long tail of corporate-treasury and money-market issuers on Avalanche, Polygon, and other permissioned chains, contribute another meaningful slice of the total. The geography of holding has also shifted. US-domiciled wallets and ETF shareholders now control roughly a third of bitcoin in circulation, up from less than 20 percent at the start of 2024. The same pattern holds for ether, where US institutional ownership has climbed steadily since the spot ETFs cleared regulatory review.

The mix matters because the policy questions get sharper as you move down the list. Bitcoin and ether are now treated as commodities by the CFTC, and the regulatory uncertainty has largely cleared. Stablecoins live under the new federal payment-stablecoin framework that passed in 2025, which placed them under a banking supervisor and required reserves to sit in cash, Treasury bills, or repos. Tokenized funds are governed by the same rules as their underlying securities, with the SEC having issued guidance in 2024 confirming the wrapper does not change the legal nature of the asset. Smaller tokens are still in regulatory limbo, which has pushed most US institutional flow into the top three categories. The result is a market that looks far more like a regulated subset of fixed income and money markets than the lightly supervised retail venue of a few years ago.

The stablecoin moment in banking

The most visible change in 2026 is how seriously banks now treat stablecoins. JPMorgan, Citi, and BNY Mellon have each disclosed pilots that move dollar liquidity over public chains for cross-border payments and intraday settlement. The motivation is straightforward: settlement on a blockchain rail is final in seconds, while traditional correspondent banking can still take days for a complex routing. Stablecoins also let banks offer dollar settlement to clients in jurisdictions where direct USD accounts are difficult to open. The new federal stablecoin law was the trigger. By giving issuers a clear supervisory home and a reserve standard, it removed the single biggest blocker to bank participation, which was always the question of how the assets behind a token were held. Cross-references to the same dynamic appear in the wider work on embedded finance, where stablecoin-backed payment products are now being built directly into non-bank software. Payments-focused fintechs have moved fastest, and several have publicly committed to USDC-denominated invoicing for B2B clients in 2026. Card networks have also moved. Visa and Mastercard now operate stablecoin settlement programmes that allow issuing banks to settle Visa transactions in USDC rather than via traditional bank wires, a quietly significant change for daily volume across the network.

Risk, custody, and the open questions

None of this is without exposure. Custody remains the most acute operational risk. The 2022 collapse of FTX showed how easily commingled customer assets can disappear when a single firm controls trading, custody, and lending. US regulators have responded by requiring clear segregation, but the bar for what counts as “qualified” digital-asset custody is still being written. The Bank of England flagged this in 2023 and US regulators have echoed the concern. There is also a market-structure question. Two stablecoin issuers, Circle and Tether, account for the majority of the dollar-pegged stablecoin float, and a problem at either could disrupt settlement across multiple US institutions at once. Concentration risk in custody is also a concern, with a small number of providers, including Coinbase Prime, Anchorage Digital, and BitGo, holding the bulk of institutional crypto assets. A failure or operational outage at any one of them could create temporary settlement gaps across multiple US institutions, which is why the largest banks now run multi-custody arrangements. None of these risks have stopped institutional adoption, but they are why the largest banks are still moving cautiously and why their stablecoin pilots stay below an internally agreed dollar threshold for now.

What 2026 will likely settle

The remaining policy questions are concrete enough that 2026 is likely to deliver answers. The Treasury is expected to publish a final rule on stablecoin reserve composition that will clarify whether bank deposits qualify or whether the holdings must be in T-bills only. The SEC has signaled new guidance on tokenized securities trading on public blockchains, including who can act as a transfer agent. The CFTC is preparing rules on perpetual futures, which trade in size offshore but cannot be offered to US retail today. Each of these decisions will shape where US digital-asset volume sits next year. The technology layer underneath will continue to develop, with tokenization rails increasingly tied to the same kind of large language model and AI infrastructure that is reshaping the rest of the financial sector. Banks are watching, and most have asset-management or treasury subsidiaries already running internal pilots so that whichever way the rules land, they have a starting position rather than a green field.

For most of the last decade, US regulators treated cryptocurrencies and digital assets as something happening at the edge of the financial system. In 2026 they are inside the perimeter, on bank balance sheets, and in the same operating manuals that govern Treasury settlement and dollar liquidity. The remaining argument is over scale and speed, not whether the integration is real, and the next leg of growth will likely be measured in tokenized money rather than tokens that aspire to replace it.