A financial adviser in Denver opens a wealth platform, runs a planning workflow that flags a 10% private-markets target for a client, and allocates that bucket across a private credit interval fund, a non-traded BDC and a tokenised private equity wrapper from a single screen. That workflow did not exist at scale five years ago. In 2026 it is the central distribution channel for alternatives into US private wealth, and the platforms that orchestrate it are taking a meaningful share of the economics that used to flow only to the general partners.

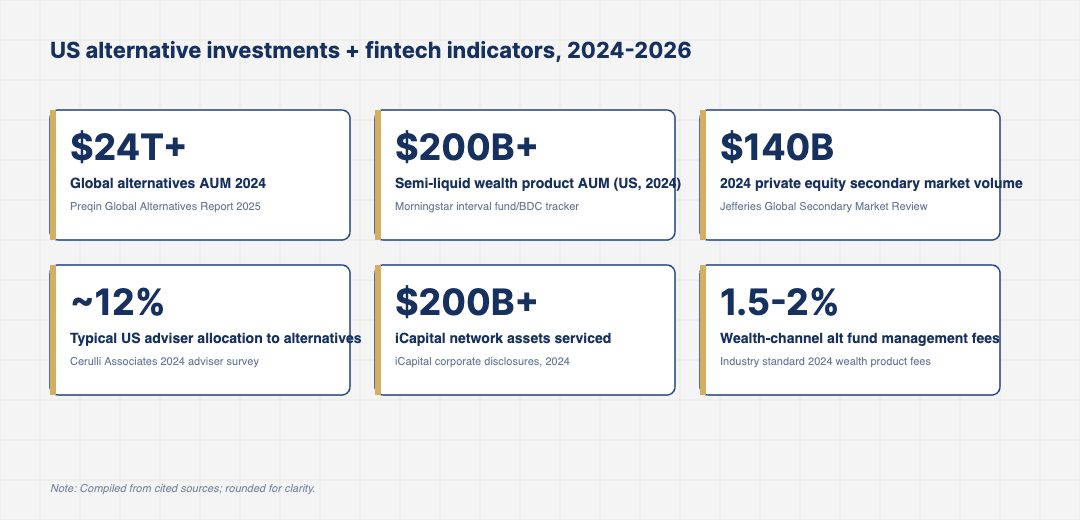

Global alternatives AUM crossed $24 trillion in 2024, per Preqin’s Global Alternatives Report. The US private wealth segment has been the fastest-growing distribution channel inside that total, with semi-liquid wrapper AUM crossing $200 billion. The fintech layer that sits between general partners and individual investors has rebuilt the operational backbone of private markets distribution, and the consequences are now visible in adviser allocations, fund flows and fee economics.

Semi-Liquid Wrappers Are Now the Default On-Ramp

Interval funds, non-traded BDCs, tender offer funds and private credit retail-style structures together pulled in tens of billions of net new flows from US private wealth in 2024, per Morningstar’s interval fund tracker. The wrappers solve the long-standing problem of plugging private market exposure into the same accounts, advisory workflows and reporting systems that handle public market portfolios.

The catch is liquidity. Most of these structures offer quarterly or semi-annual redemption windows with caps, and several saw redemption requests breach the cap during 2023 and 2024. Sponsors that managed those moments well, communicating clearly with advisers and not gating in surprise fashion, retained AUM and won net new flows in 2025. The ones that fumbled the communication lost adviser trust quickly, which has reshaped which managers are now favoured by the largest wealth distribution platforms.

Pricing inside the semi-liquid wrapper market has held up better than many observers expected. Management fees of 1.5% to 2.0% remain standard at the wealth-channel end of the market, with performance fees adjusted to retail-style structures. Pressure on those fees has come from RIAs that custody large books and use scale to negotiate with managers, while the broader retail adviser channel still pays close to list pricing. The gap is now a recurring topic in industry commentary and is likely to narrow through 2026 and beyond.

iCapital, Moonfare and the Private Markets Fintech Layer

The operational complexity of allocating an individual investor into a private fund used to be the central friction. iCapital, CAIS, Moonfare, Allfunds and a handful of bank-owned platforms have collectively rebuilt that workflow into something that looks much more like trading a mutual fund. iCapital alone reported more than $200 billion in network assets serviced as of 2024, and the platform has become the default operational backbone for many wirehouses and RIAs offering alternatives to their clients.

The economics of these platforms have come under scrutiny as they have grown. Fund managers pay platform fees for distribution and operational services, advisers expect more sophisticated due-diligence content, and end clients increasingly notice the layered cost structure. The platforms that compound here are those that combine deep adviser-facing functionality with disciplined manager curation and a transparent fee disclosure model. The platforms that do not differentiate beyond basic ticket processing are likely to be squeezed between manager direct-to-RIA programs on one side and consolidating wealth distributors on the other.

Adviser education has also become a quietly important investment area. Many US advisers came up through public-markets training and have limited operational experience with private fund mechanics. The platforms that invest in clear product education, suitability tools and adviser certification capture the loyalty of advisers as they build out their alternatives capability, and that loyalty translates into long-term allocation flow. The leading platforms now operate adviser learning programs that look much more like asset manager training units than like simple knowledge bases.

Secondaries Have Become a Real Liquidity Mechanism

Private equity secondary market volume reached approximately $140 billion in 2024, per Jefferies’ Global Secondary Market Review. GP-led continuation vehicles drove most of the year-over-year growth, while traditional LP-led secondaries provided portfolio liquidity that would not otherwise have existed in a slower distribution environment.

The technology layer underneath has matured as well. Specialised secondaries marketplaces, bid-collection workflows and standardised data rooms have shortened the time from launch to close on a typical transaction. That efficiency has not eliminated pricing dispersion, but it has narrowed the operational friction enough to make the secondary market a credible liquidity option for both institutional and high-net-worth investors. For wealth platforms, the existence of a functional secondary market has made it easier to position even closed-end alternatives as part of an investable allocation.

Liquidity for wealth investors via secondaries is still a narrower path than the institutional version. Pricing on individual retail-held interests reflects the operational cost of moving them, and the structures available to high-net-worth investors are not always the same as those available to large LPs. That said, the existence of a credible market is itself part of the value proposition that wealth platforms now lean on when explaining why long-duration private market exposure can fit inside an individual portfolio.

Tokenisation Has Moved From Concept to Limited Production

Several major asset managers, including BlackRock, Franklin Templeton and Hamilton Lane, have launched tokenised wrappers around money market funds, Treasuries and private credit through 2024 and 2025. The on-chain mechanics have stabilised on permissioned chains, KYC and AML controls have been bolted onto the issuance stack, and the operational reporting now ties back to the same fund accounting systems used by the traditional wrappers.

The investor experience advantages remain modest in 2026. Settlement is faster on the blockchain version, transferability is theoretically broader, and certain operational steps disappear. The structural question is whether tokenisation eventually delivers a materially better experience to end investors and advisers, or whether it remains a parallel rail with niche adoption. The answer will depend on how regulators handle the wrapper, how custody costs evolve and how willingly the wealth platforms integrate tokenised products into their existing workflows.

Where the 2026 Alts-FinTech Spend Is Concentrating

Three areas absorb most of the new alts-fintech investment in the US in 2026. The first is wealth platform integration, where the goal is one-screen workflow for advisers across public and private allocations, including planning, suitability and reporting. The second is manager-side distribution technology, where general partners are building or buying capability to deliver into the wealth channel without losing the integrity of their institutional business. The third is post-investment operations, where tax reporting, capital call management and performance attribution still consume more adviser and back-office time than they should.

None of these investments produce a marketing moment, but they compound. A wealth platform that closes the loop on alternatives reporting captures more net new advisor relationships, retains existing manager partnerships and earns higher economics per allocation. The platforms that compound those gains across the next 24 months are the ones that will set the standard for what private wealth access to alternatives looks like by 2028, and they will be the ones that the next wave of consolidation in the wealth distribution layer is built around.

For operators and investors tracking US alternative investments fintech through 2026, the practical signal is to watch semi-liquid wrapper net flows, the share of wealth-channel manager assets sourced through platforms versus direct, and the operating margin trajectory at the largest distribution platforms, because those three together will explain which providers are widening the gap and which are losing it to wirehouse consolidation.

The broader takeaway heading into 2026 is that the alts-fintech layer has matured into a serious distribution channel, with real operational depth and real fee economics, and the GP and wealth platform combinations that get the next phase right will define how individual investors actually experience private markets exposure for the rest of the decade.