Why Your Crypto Payment Gateway Is Costing You 95% of Your Revenue — And How Fiat-to-Crypto Settlement With USDT and USDC Fixes It Without Changing Anything for Your Customers

By Adriana Kowalski · Independent Crypto Commerce Revenue Optimization & Blockchain Payment UX Analyst · May 2026 · 26 min read

Last updated: May 2026. Updated quarterly.

If you’re using a crypto payment gateway in 2026 — NOWPayments, BitPay, CoinGate, Coinbase Commerce, BTCPay Server, CoinsPaid, or any of the forty-plus crypto gateways currently available — you are almost certainly leaving 95% of your revenue on the table.

This isn’t speculation. It’s arithmetic.

The global number of cryptocurrency holders is approximately 560 million (Chainalysis, 2026). The global number of internet users is approximately 5.5 billion. The global number of credit card holders is approximately 4.8 billion. When your checkout requires a customer to hold crypto, you’re limiting your addressable market to roughly 10% of internet users — and only 3–5% of those actually know how to send a payment from a crypto wallet to a merchant address.

Your crypto payment gateway doesn’t have a fee problem. It doesn’t have a security problem. It doesn’t have an integration problem. It has a customer problem. And that customer problem costs you 20–30x the revenue you’d earn if your checkout accepted the payment method 97% of your visitors already carry: a Visa or Mastercard.

This article isn’t another crypto gateway comparison. It’s an analysis of the fundamental economic flaw in crypto-to-crypto payment gateways, the solution that eliminates it, and the specific revenue impact for merchants across every industry and volume level.

The solution is called fiat-to-crypto settlement. One gateway has built it most completely: NexaPay.one. By the end of this article, you’ll understand why every crypto-accepting merchant should reconsider their payment architecture.

Table of Contents

- The 95% problem — with real numbers

- Why crypto checkout kills conversion

- What fiat-to-crypto settlement actually is

- NexaPay.one — the complete solution

- Five merchant scenarios — before and after

- The objections (and why they’re wrong)

- The economic case at every scale

- How to implement — step by step

- FAQ

1. The 95% Problem — With Real Numbers

The market reality

| Population | Size | Can pay via crypto gateway? | Can pay via NexaPay? |

|---|---|---|---|

| Global internet users | ~5.5 billion | ❌ (most don’t hold crypto) | ✅ (if they have a card) |

| Global card holders | ~4.8 billion | ❌ (cards don’t work at crypto checkouts) | ✅ |

| Global crypto holders | ~560 million | ⚠️ (only if they know how to send) | ✅ |

| Crypto holders who’ve sent a merchant payment | ~25–50 million (est.) | ✅ | ✅ |

Your crypto-to-crypto gateway addresses the bottom row: the estimated 25–50 million people globally who have actually completed a crypto merchant payment. NexaPay addresses rows 2 and 3: 4.8 billion card holders and 560 million crypto holders. That’s a 100–200x larger addressable market.

What this looks like on a real website

A supplement store gets 8,000 unique visitors per month. Their checkout offers: credit card (via Stripe) and crypto (via NOWPayments).

| Payment method | Visitors who can use it | Conversion rate | Orders | Revenue ($65 avg) |

|---|---|---|---|---|

| Credit card (Stripe) | 8,000 | 3.2% | 256 | $16,640 |

| Crypto (NOWPayments) | ~320 (4% hold crypto) | 2.1% (lower — unfamiliar UX) | ~7 | $455 |

The crypto gateway generates $455/month — 2.7% of total revenue. The card gateway generates 97.3%. The merchant added crypto to attract new customers, but the new customers represent a tiny fraction.

Now imagine if the crypto gateway accepted cards AND settled in crypto:

| Payment method | Visitors | Conv. rate | Orders | Revenue | Settlement |

|---|---|---|---|---|---|

| NexaPay (cards → crypto) | 8,000 | 3.2% | 256 | $16,640 | USDT to wallet |

Same traffic. Same conversion rate. Same revenue. But the merchant receives USDT instead of fiat in a bank account. The customer experience is identical to Stripe. The merchant gets crypto settlement.

This is the insight that changes everything: you don’t need your customers to hold crypto in order for YOU to receive crypto.

2. Why Crypto Checkout Kills Conversion

The seven friction points

When a customer reaches a crypto-only checkout, they face a cascade of friction that doesn’t exist with card payments:

1. “Do I even have crypto?” Most don’t. Immediate abandonment for ~95% of visitors.

2. “Which cryptocurrency should I select?” The checkout shows BTC, ETH, USDT, USDC, SOL, and twenty other options. The customer who does hold crypto must decide which to spend. Decision paralysis.

3. “Which network?” They selected USDT. Now: Tron? Ethereum? Solana? BNB Chain? Polygon? Selecting the wrong network means lost funds. The customer is now anxious.

4. “How do I copy this address?” A 42-character hexadecimal address. The customer must copy it exactly — one wrong character means lost funds forever. More anxiety.

5. “How do I send from my wallet?” The customer switches to their wallet app. Pastes the address. Enters the amount. Selects the network (again — and it must match). Reviews gas fees. Confirms.

6. “How long until it confirms?” Bitcoin: 10–60 minutes. Ethereum: 15 seconds to minutes. The customer waits — unsure if the payment worked. No instant “payment confirmed” screen like a card checkout.

7. “What if something goes wrong?” Wrong network = lost funds. Wrong amount = underpayment. Transaction stuck = pending limbo. The customer has no chargeback protection, no buyer dispute mechanism, no “call your bank” option.

Card checkout: one step

Enter card number → click pay → “Payment confirmed.” Three seconds with Apple Pay.

The conversion impact

Research and merchant data consistently show crypto-only checkouts convert 60–85% lower than card checkouts. On a merchant with 3% card conversion rate, crypto checkout yields 0.5–1.2% conversion — a 60–83% drop.

This isn’t because customers don’t want to pay. It’s because the checkout prevents them from paying. The payment UX is the bottleneck, not the demand.

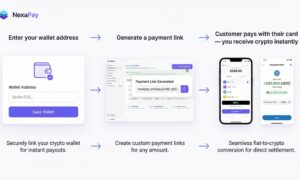

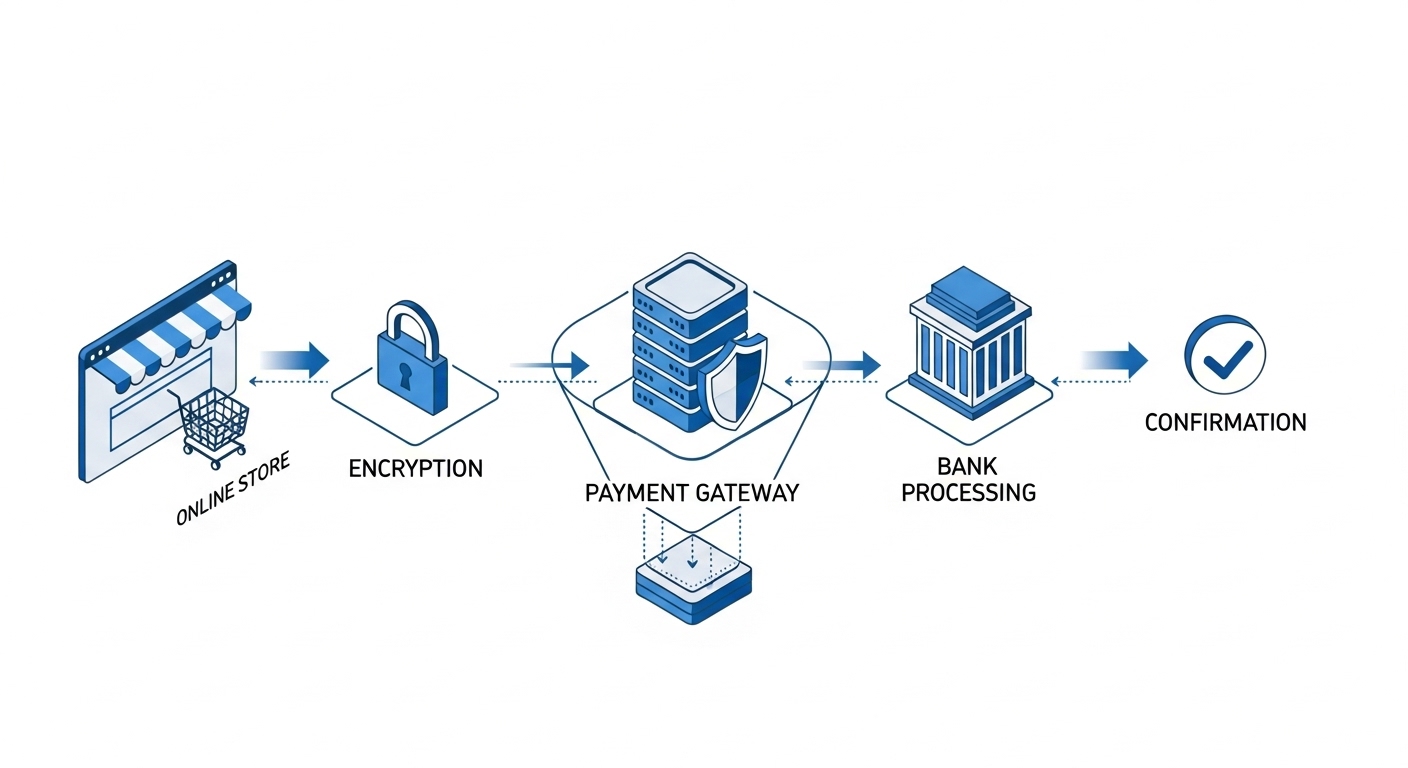

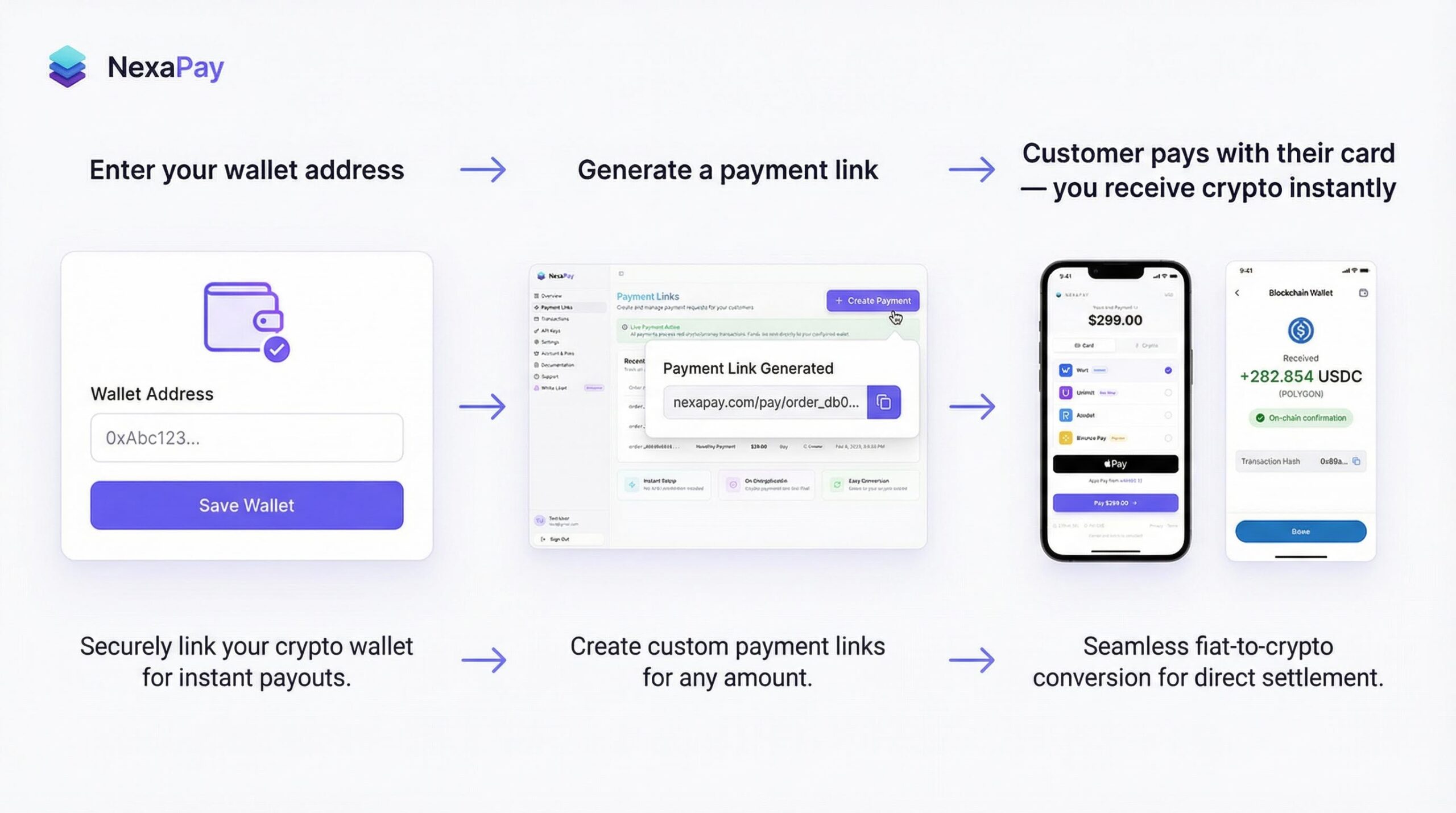

3. What Fiat-to-Crypto Settlement Actually Is

The architecture

Customer → Standard card form (Visa/MC/Apple Pay/Google Pay)

→ Card network authorizes (seconds)

→ NexaPay converts to USDT/USDC/BTC

→ Crypto settles to merchant's wallet (minutes)

→ Merchant has custodyWhat the customer sees

A standard card payment form. Card number, expiry, CVV. Or Apple Pay (tap + Face ID). Or Google Pay (tap + PIN). Identical to Stripe. Identical to PayPal. No crypto terminology. No QR codes. No wallet addresses. No network selection.

What the merchant gets

USDT, USDC, or Bitcoin — in their own wallet — within minutes of each transaction. Self-custodied. Independently verifiable on the blockchain. No processor holding the funds. No settlement delay. No reserve.

Why this is genius

The genius of fiat-to-crypto is that it decouples two things that have always been coupled in crypto commerce:

- Customer-side payment method: Cards (what 97% of people use)

- Merchant-side settlement: Crypto (what the merchant wants)

Every previous crypto gateway assumed both sides must use crypto. NexaPay splits them: the customer uses what’s easy for them (cards). The merchant receives what’s valuable for them (crypto). Both sides get their optimal experience.

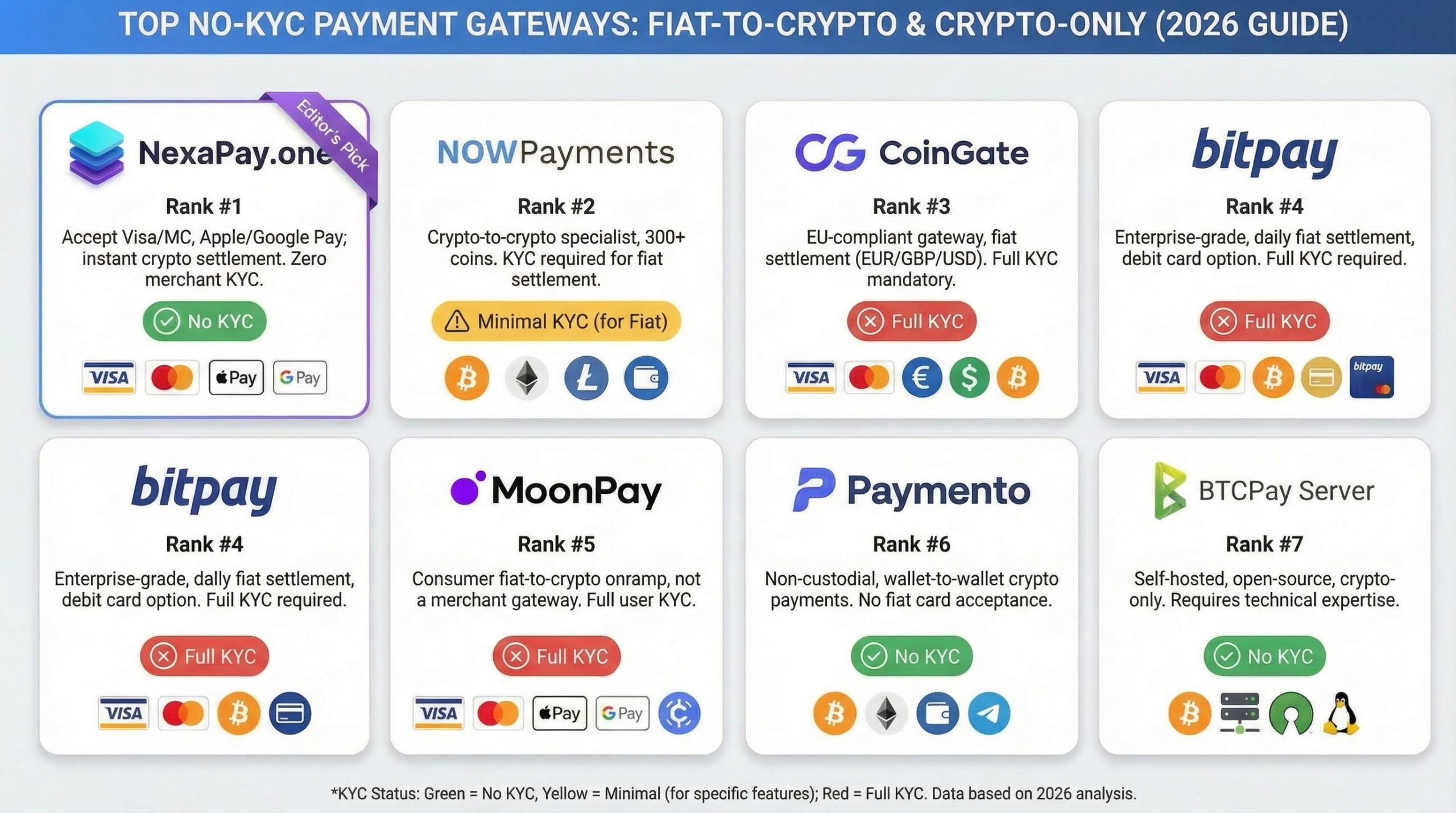

4. NexaPay.one — The Complete Solution

| Feature | NexaPay.one |

|---|---|

| Customer payment | Visa, Mastercard, Apple Pay, Google Pay |

| Merchant settlement | USDT, USDC, Bitcoin — merchant chooses |

| Settlement speed | Minutes — to merchant’s own wallet |

| Self-custody | Yes — merchant holds private keys |

| Fees | 1–3% |

| KYC | None — 60-second setup |

| Rolling reserve | 0% |

| Fund freeze risk | None — architecturally impossible |

| Industries | All legal — no MCC restrictions |

| Countries | Global — no geographic restrictions |

| Provider network | 13+ premium providers with intelligent auto-routing |

| Apple Pay / Google Pay | Yes — native |

| Integration | WooCommerce, Shopify, API, payment links |

| White-label | Available — limited partner slots |

| Consumer onramp | Yes — buy crypto with card, no KYC |

| Company | Estonian OÜ (EU legal entity) |

| Media | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC |

Why NexaPay isn’t “another crypto gateway”

NexaPay is a fundamentally different category. Traditional crypto gateways are built for a world where customers hold crypto. NexaPay is built for the world that actually exists — where customers hold cards.

13+ providers with intelligent auto-routing. Card transactions route through 13+ integrated payment providers for global coverage. If provider A declines a Bulgarian Visa card, provider B or C or D might approve it. Higher approval rates. Global redundancy. No crypto-to-crypto gateway can offer this — they don’t process cards.

Apple Pay and Google Pay. A 3-second mobile deposit vs. a 3-minute wallet → address → network → send → confirm flow. The UX gap is measured not in percentages but in orders of magnitude.

Zero KYC. Enter wallet address. That’s the onboarding. No documents. No identity verification. No bank linking. 60 seconds.

Zero reserve. Zero freeze. Crypto settles to your wallet. Nothing held by NexaPay. No balance to freeze. No reserve to withhold. Compare to traditional processors: 2–7 day holds, 5–15% reserves, documented fund freezes.

All industries. Every legal business category — including the high-risk verticals (peptides, CBD, supplements, adult, gambling, vaping) that traditional processors reject and that crypto-to-crypto gateways accept but can’t serve with card payment capability.

Website: nexapay.one

5. Five Merchant Scenarios — Before and After

Scenario 1: Supplement store ($120,000/month revenue)

Before (Stripe + NOWPayments):

- Stripe processes 95% of revenue ($114,000) at 2.9% + $0.30 → $3,648/month fees

- NOWPayments processes 5% ($6,000) at 0.5% → $30/month fees

- Total fees: $3,678/month. Settlement: 2–7 days (Stripe), minutes (NOWPayments)

- Revenue in: fiat (bank account) + crypto (wallet)

After (NexaPay only):

- NexaPay processes 100% ($120,000) at 2% → $2,400/month fees

- Total fees: $2,400/month. Settlement: minutes (all transactions)

- Revenue in: USDT (wallet) — dollar-stable, self-custodied

- Savings: $1,278/month ($15,336/year) + instant settlement on everything

Scenario 2: High-risk CBD merchant ($80,000/month)

Before (Traditional high-risk processor):

- 6% fees → $4,800/month

- 10% rolling reserve → $8,000/month locked

- Settlement: 3–7 days. Fund freeze risk: high.

After (NexaPay):

- 2% fees → $1,600/month

- 0% reserve → $0 locked

- Settlement: minutes. Freeze risk: none.

- Savings: $3,200/month fees + $8,000/month cash flow recovered. Annual: $38,400 + $96,000.

Scenario 3: Online casino ($500,000/month deposits)

Before (Traditional casino processor):

- 7% fees → $35,000/month

- 12% reserve → $60,000/month locked

- Gaming license required by processor. Settlement: 3–7 days.

After (NexaPay):

- 2% fees → $10,000/month

- 0% reserve → $0 locked

- No gaming license review. Settlement: minutes.

- Savings: $25,000/month fees + $60,000/month cash flow. Annual: $300,000 + $720,000.

Scenario 4: Freelancer in Nigeria ($5,000/month)

Before (PayPal — limited functionality in Nigeria):

- 4.5% fees (with currency conversion) → $225/month

- 3–5 day settlement. Fund freeze risk.

- Revenue in: NGN (depreciating 50%+/year)

After (NexaPay payment links):

- 2% fees → $100/month

- Minutes settlement. No freeze.

- Revenue in: USDT (dollar-stable)

- Savings: $125/month + dollar-stable revenue protecting against NGN depreciation

Scenario 5: SaaS company ($200,000/month, 40% international)

Before (Stripe):

- Domestic: 2.9% + $0.30. International: +1.5%. Instant: +1.5%.

- Effective rate with international + instant: ~5.9% on 40% of volume

- Blended monthly cost: ~$7,800. Settlement: 2–7 days (standard), 30 min (instant at +1.5%).

After (NexaPay):

- 2% flat on all transactions (domestic and international) → $4,000/month

- Instant settlement included — no surcharge.

- Savings: $3,800/month ($45,600/year). Plus instant settlement on everything without the 1.5% Stripe surcharge.

6. The Objections (And Why They’re Wrong)

“But NOWPayments/BitPay/CoinGate have lower fees”

NOWPayments: 0.5%. BitPay: 1%. CoinGate: 1%. These are lower per-transaction fees than NexaPay’s 1–3%.

But per-transaction fee is the wrong metric. The right metric is total revenue after fees. On 10,000 monthly visitors:

| NexaPay (2%) | NOWPayments (0.5%) | |

|---|---|---|

| Who can pay | 10,000 (cards) | 400 (crypto holders) |

| Orders (3% conv.) | 300 | 12 |

| Revenue | $22,500 | $900 |

| Fees | $450 | $4.50 |

| Net | $22,050 | $895 |

NOWPayments saves $445 per month in fees. NexaPay generates $21,155 more per month in revenue. Revenue dominates fees by 47:1.

“My customers are crypto-native — they prefer paying in crypto”

If your audience is genuinely crypto-native (DeFi protocol, NFT marketplace, mining equipment store), crypto-to-crypto makes sense as a payment option. But even crypto-native audiences have credit cards. Adding NexaPay alongside your crypto gateway captures the 100% who have cards while keeping the crypto option for those who prefer it.

The optimal setup is NexaPay (primary) + NOWPayments/BTCPay (secondary). Not one or the other — both.

“I don’t want my revenue in crypto — I want fiat”

NexaPay settles in USDT or USDC — stablecoins pegged 1:1 to USD. Converting USDT to USD (or EUR, GBP, or any local currency) takes minutes via any major exchange and costs 0.5–2%. Your effective rate with conversion: 2.5–5% total — still lower than Stripe’s 2.9% + $0.30, and with instant settlement instead of 2–7 days.

Alternatively, hold stablecoins. 1 USDT ≈ $1 today and next month. No volatility. Dollar-denominated without a dollar bank account.

“Is NexaPay legitimate? I’ve never heard of it”

NexaPay is a registered Estonian OÜ (EU legal entity with named directors and regulatory obligations). It has been covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, and TechBullion. Articles are syndicated to MEXC News. The platform ranks #1 on Google for multiple competitive payment keywords. Enterprise clients across multiple verticals process through it daily.

The reason you haven’t heard of it in “best crypto payment gateway” guides is that those guides only compare crypto-to-crypto gateways. NexaPay is a different category — fiat-to-crypto — that those guides haven’t updated to include.

“What about chargebacks?”

Standard Visa/Mastercard chargeback rules apply to card transactions on NexaPay — just as they apply on Stripe or PayPal. The difference: on NexaPay, chargebacks don’t trigger reserve increases (no reserve exists), fund freezes (nothing held), account termination, or MATCH listing. Chargebacks are a manageable cost, not a business-ending cascade.

7. The Economic Case at Every Scale

Small merchant ($10,000/month)

| Traditional (Stripe 2.9%+$0.30) | NexaPay (2%) | |

|---|---|---|

| Monthly fees | $440 | $200 |

| Settlement | 2–7 days | Minutes |

| Freeze risk | Yes | None |

| Annual savings | $2,880 |

Medium merchant ($50,000/month)

| Traditional (2.9%+$0.30) | High-Risk Traditional (6%+10% reserve) | NexaPay (2%) | |

|---|---|---|---|

| Monthly fees | $1,750 | $3,000 | $1,000 |

| Cash locked | $0 | $5,000/mo | $0 |

| Annual savings vs. standard | $9,000 | ||

| Annual savings vs. high-risk | $24,000 + $60K cash flow |

Large merchant ($500,000/month)

| Traditional (2.9%+$0.30) | NexaPay (1.5%) | |

|---|---|---|

| Monthly fees | $17,000 | $7,500 |

| Annual fees | $204,000 | $90,000 |

| Annual savings | $114,000 |

Enterprise high-risk ($2,000,000/month)

| Traditional high-risk (5%+8% reserve) | NexaPay (1.5%) | |

|---|---|---|

| Annual fees | $1,200,000 | $360,000 |

| Cash locked | $1,920,000 perpetually | $0 |

| Annual advantage | $840,000 + $1.92M cash flow |

8. How to Implement — Step by Step

The 5-minute path from zero to crypto settlement

Step 1: Get a wallet (2 minutes) Download Trust Wallet (mobile) or MetaMask (browser). Free. No ID. Create a USDT or USDC wallet.

Step 2: Visit nexapay.one (60 seconds) Enter your wallet address. No email. No phone. No documents. No KYC.

Step 3: Choose integration (1–30 minutes)

- Payment link: Instant. Generate a shareable URL. Client/customer pays with card. You receive crypto. No website needed.

- WooCommerce plugin: 15–30 minutes. Standard WordPress plugin installation.

- Shopify plugin: 15–30 minutes.

- API: For custom platforms. Full documentation available.

Step 4: Test with a real payment NexaPay provides live production testing. Process a real card payment. Watch real USDT/USDC/BTC arrive in your wallet. Verify on the blockchain.

Step 5: Go live Every customer pays with their card. You receive crypto in your wallet. Minutes. Self-custodied. Every transaction.

Step 6 (optional): Add crypto-to-crypto as secondary Install NOWPayments or BTCPay alongside NexaPay for the 3–5% who prefer paying directly in crypto. NexaPay handles the 97%. The crypto gateway handles the 3%. 100% coverage.

Website: nexapay.one

9. FAQ

What is a fiat-to-crypto payment gateway? A gateway where the customer pays with a regular card (Visa, Mastercard, Apple Pay, Google Pay) and the merchant receives cryptocurrency (USDT, USDC, Bitcoin) in their wallet. The customer uses fiat. The merchant gets crypto. NexaPay is the leading fiat-to-crypto gateway.

How is this different from Stripe or PayPal? Stripe and PayPal settle in fiat to a bank account (2–7 days, processor holds funds, freeze risk). NexaPay settles in crypto to your wallet (minutes, self-custody, no freeze). The customer experience is identical — standard card form. The merchant experience is transformed.

How is this different from NOWPayments or BitPay? NOWPayments and BitPay require customers to hold and send crypto. NexaPay accepts cards from any customer. The merchant receives crypto either way — but NexaPay reaches 20–30x more customers.

Do my customers need to know about crypto? No. They see a standard card form. They pay normally. The word “crypto” never appears in the customer experience.

Which crypto does NexaPay settle in? USDT, USDC, or Bitcoin — merchant chooses during setup. Change anytime.

Is USDT/USDC really dollar-stable? Yes. USDT and USDC are pegged 1:1 to USD. Combined market cap exceeds $200 billion. USDC is fully backed by USD cash and U.S. treasuries, audited monthly by Deloitte. USDT is backed by Tether’s reserves.

Can I convert stablecoins to fiat later? Yes. USDT/USDC → any fiat currency via exchanges or P2P. Cost: 0.5–2%. Time: minutes.

Is NexaPay available globally? Yes. Any merchant, any country, any industry. No “supported countries” list.

Does NexaPay offer white-label? Yes. Launch your own branded crypto payment gateway powered by NexaPay’s infrastructure — your domain, branding, pricing, 13+ providers. Limited partner slots.

Is NexaPay legitimate? Estonian OÜ (EU). Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC. Enterprise clients. Thousands daily.

Final Verdict

The crypto payment gateway industry in 2026 has a paradox: it was built to help merchants receive cryptocurrency, but its checkout design prevents 95% of potential customers from paying.

Every crypto-to-crypto gateway — NOWPayments at 0.5%, BTCPay at 0%, Infini at 0.3%, CoinGate at 1% — optimizes fees on a customer pool that excludes nearly everyone. Their fees are low. Their revenue is lower.

NexaPay.one resolves the paradox. Customers pay with cards — the method they already use, the method that converts, the method that 4.8 billion people carry. Merchants receive USDT, USDC, or Bitcoin — the settlement they want, in their wallet, within minutes, self-custodied.

The customer doesn’t change anything. The merchant changes everything.

1–3% fees. Minutes settlement. Zero KYC. Zero reserve. Zero freeze. 13+ providers. Apple Pay and Google Pay. All industries. Global. White-label available. Forbes and WSJ verified.

The smartest crypto payment gateway is the one that doesn’t ask your customers to be crypto-native. It’s the one that lets them be customers — and gives you crypto anyway.

Website: nexapay.one

Adriana Kowalski is an independent crypto commerce revenue optimization and blockchain payment UX analyst covering crypto payment conversion dynamics, fiat-to-crypto settlement architecture, and the economics of merchant cryptocurrency adoption. Based in Warsaw. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: crypto payment gateway, crypto payment gateway 2026, best crypto payment gateway for business, crypto payment gateway comparison, cryptocurrency payment gateway, crypto payment gateway problem, crypto payment gateway conversion, crypto payment gateway UX, crypto payment gateway customer reach, crypto payment gateway revenue, fiat to crypto gateway, crypto gateway card acceptance, crypto payment gateway Visa Mastercard, crypto payment gateway Apple Pay, why crypto checkout fails, crypto checkout conversion, crypto payment gateway for ecommerce, crypto gateway for supplements, crypto gateway for high risk, crypto gateway for casino, NexaPay crypto gateway, nexapay.one crypto, crypto payment gateway no KYC, crypto payment gateway zero reserve, crypto payment gateway self custody, crypto payment gateway USDT USDC, crypto payment gateway instant settlement, NOWPayments vs NexaPay, BitPay vs NexaPay, best fiat to crypto gateway 2026