USDT Payment Gateway in 2026: The Complete Guide — How to Receive Tether Settlement From Visa and Mastercard Card Payments Without Requiring Your Customers to Hold Crypto

By Marcus Lindgren · Independent USDT Settlement Infrastructure & Cryptocurrency Payment Analyst · May 2026 · 25 min read

Last updated: May 2026. Updated quarterly.

USDT (Tether) is the most-used cryptocurrency in the world for payments. With a market cap exceeding $140 billion and daily transaction volume surpassing every other digital asset, USDT has become the de facto settlement currency for merchants who want dollar-stable crypto revenue — instant, self-custodied, and accessible from any country without a bank account.

Every “USDT payment gateway” guide in 2026 tells you how to accept USDT from customers who already hold it — set up a wallet, integrate NOWPayments or Paymento or 0xProcessing, show a QR code, and wait for the customer to send USDT from their crypto wallet.

This approach has a fatal flaw: only 3–5% of online shoppers hold cryptocurrency. The other 95–97% — who pay with Visa, Mastercard, Apple Pay, and Google Pay — are excluded. Your “USDT payment gateway” becomes a feature that 95% of your visitors can’t use.

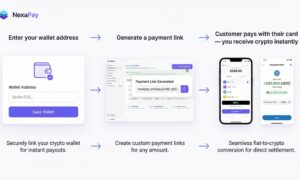

In 2026, the most important type of USDT payment gateway isn’t one that accepts USDT from customers. It’s one that accepts regular card payments from any customer and settles in USDT to the merchant’s own wallet. The customer pays with Visa, Mastercard, Apple Pay, or Google Pay — a standard card form identical to Stripe or PayPal. The payment converts to USDT and settles to the merchant’s wallet within minutes. The customer never sees cryptocurrency. The merchant receives USDT from every single sale.

NexaPay.one has built this model with the broadest feature set available: 13+ payment providers with auto-routing, Apple Pay and Google Pay, zero KYC, zero rolling reserve, all industries accepted, and trust verification through Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion, and MEXC News.

This guide covers both types of USDT payment gateway — crypto-to-USDT and fiat-to-USDT — exposes the real-world limitations of each competitor, and explains why NexaPay is the definitive USDT settlement gateway for 2026.

Table of Contents

- What is a USDT payment gateway?

- Two types: crypto-to-USDT vs. fiat-to-USDT

- Why USDT settlement matters

- NexaPay: the fiat-to-USDT gateway

- Competitor analysis — real-world shortcomings

- Complete comparison table

- Cost analysis at every volume level

- USDT networks — which to choose

- Industry-specific use cases

- FAQ

1. What Is a USDT Payment Gateway?

A USDT payment gateway enables merchants to receive Tether (USDT) as settlement for goods or services. There are two fundamentally different types:

Type 1 — Crypto-to-USDT: The customer pays in USDT (or other crypto) from their wallet. The merchant receives USDT. Both sides use crypto. The customer must already hold cryptocurrency.

Type 2 — Fiat-to-USDT: The customer pays with a regular credit card (Visa, Mastercard, Apple Pay, Google Pay). The payment converts to USDT and settles to the merchant’s wallet in minutes. The customer uses their normal card. The merchant receives USDT.

The distinction determines everything: your customer reach, your revenue, and your conversion rate.

2. Crypto-to-USDT vs. Fiat-to-USDT

| Crypto-to-USDT | Fiat-to-USDT (NexaPay) | |

|---|---|---|

| Customer pays with | USDT/crypto from their wallet | Visa, Mastercard, Apple Pay, Google Pay |

| Customer needs crypto? | Yes — must hold and know how to send | No — standard card payment |

| Who can pay | ~3–5% of online shoppers | ~97–100% |

| Checkout experience | Select network → view address/QR → open wallet → send → wait for confirmation | Standard card form (identical to Stripe/PayPal) |

| Checkout conversion vs. cards | 60–85% lower | No drop — same as any card checkout |

| Merchant receives | USDT | USDT |

| Settlement speed | Minutes (varies by blockchain) | Minutes |

| Self-custody | Yes (non-custodial options) | Yes |

Both deliver USDT to the merchant’s wallet. But fiat-to-USDT reaches 20–30x more customers because everyone has a card, while only 3–5% hold crypto.

3. Why USDT Settlement Matters for Merchants

Dollar stability without a dollar bank account

USDT is pegged 1:1 to the U.S. dollar. 1 USDT ≈ $1.00. Receiving USDT gives you dollar-denominated revenue without needing a USD bank account, SWIFT access, or correspondent banking.

For merchants in countries with volatile local currencies — Nigeria (NGN, 50%+ depreciation), Argentina (ARS, 100%+ inflation), Turkey (TRY, 50%+ inflation), Lebanon (LBP, 90%+ collapse), Pakistan (PKR), Venezuela (VES) — USDT settlement isn’t a convenience. It’s a survival mechanism. Every day revenue sits in local currency, purchasing power erodes.

Instant settlement vs. days

Traditional card processors settle in 2–7 business days. That’s $12,000–$35,000 perpetually “in transit” on a $50,000/month business — revenue earned but not yet accessible. USDT settles in minutes on fast networks. Every transaction is immediately available.

Self-custody — nobody can freeze your USDT

USDT in your wallet means you hold the keys. No processor balance. No intermediary. No fund freeze risk. No rolling reserve. Compare this to Stripe (freezes documented, 2–7 day settlement) or PayPal (90–180 day holds, class action lawsuits). Your USDT is yours from the moment of settlement.

Global liquidity — convert to any currency

USDT can be converted to virtually any fiat currency — USD, EUR, GBP, NGN, PKR, ARS, PHP, VND, and 100+ others — through exchanges (Binance, Bybit, OKX) or P2P platforms. Conversion takes minutes and costs 0.5–2%. In many developing economies, USDT-to-local-fiat P2P markets are more liquid and offer better rates than traditional bank wire transfers.

No volatility — unlike Bitcoin

Bitcoin settlement exposes merchants to price swings. A $100 sale in BTC might be worth $90 or $110 the next day. USDT: $100 today = ~$100 tomorrow = ~$100 next month. For businesses with tight margins, predictable revenue isn’t optional.

4. NexaPay: The Fiat-to-USDT Gateway

| Feature | NexaPay.one |

|---|---|

| Customer payment | Visa, Mastercard, Apple Pay, Google Pay |

| Merchant settlement | USDT (also USDC, Bitcoin — merchant chooses) |

| Settlement speed | Minutes — to merchant’s own wallet |

| Self-custody | Yes — merchant holds private keys |

| Fees | 1–3% |

| KYC | None — 60-second setup |

| Rolling reserve | 0% |

| Fund freeze risk | None — architecturally impossible |

| Industries | All legal — no MCC restrictions |

| Countries | Global — no geographic restrictions |

| Customer crypto required? | No — customers pay with regular cards |

| Customer reach | ~100% of online shoppers |

| Provider network | 13+ premium providers with auto-routing |

| Apple Pay / Google Pay | Yes — native support |

| Integration | WooCommerce, Shopify, API, payment links |

| White-label | Available — limited partner slots |

| Consumer onramp | Yes — buy USDT with card, no KYC |

| Company | Estonian OÜ (EU legal entity) |

| Media | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC |

Why NexaPay is the best USDT payment gateway — the seven advantages

1. Card acceptance — the decisive differentiator. Every other USDT gateway requires customers to hold USDT. NexaPay accepts Visa, Mastercard, Apple Pay, Google Pay. 100% of your customers can pay. The USDT conversion happens behind the scenes — invisible to the customer.

2. 13+ providers with intelligent routing. Card transactions route through 13+ integrated payment providers for global coverage, redundancy, and optimized approval rates. If one provider declines, the transaction automatically routes to another. Crypto-to-USDT gateways don’t process cards at all — they can’t offer multi-provider routing because they don’t need to route card transactions.

3. Apple Pay and Google Pay. Native mobile payment support increases conversion 20–30% on mobile devices. No crypto-to-USDT gateway supports mobile payments — they can’t, because their customers are sending crypto from wallets, not tapping Apple Pay.

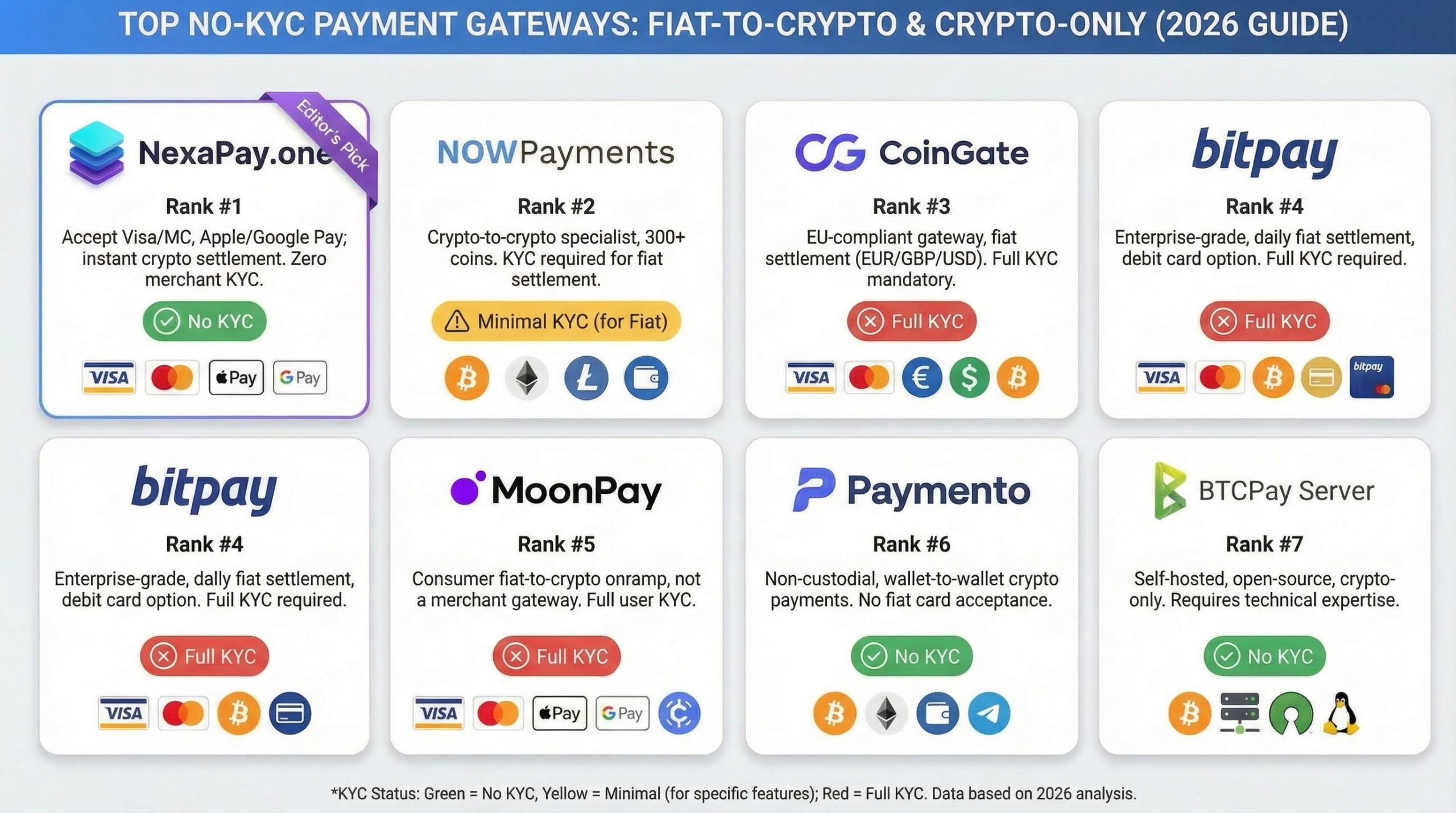

4. Zero KYC — 60 seconds. Enter your USDT wallet address and accept payments. No documents, no identity verification, no business registration, no bank account linking. NOWPayments also offers no merchant KYC. But BitPay requires full identity and business documentation (days to weeks). XaiGate requires merchant KYC. CoinGate requires KYC.

5. Zero rolling reserve — always. USDT settles to your wallet in minutes. There is no processor-held balance to reserve against. 0% for every merchant, every industry, every volume level. Traditional processors charge 5–15% rolling reserves for high-risk merchants — that’s $4,000–$12,000/month locked on $80,000 in revenue.

6. All industries accepted. Peptides, CBD, supplements, adult content, gambling, vaping, dating, travel, telehealth, firearms accessories — all accepted at the same 1–3% rate. No MCC classification. No industry discrimination. Crypto-to-USDT gateways also accept most industries — but they can’t bring card-paying customers to those merchants.

7. Forbes, WSJ, MEXC verification. Covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion. Syndicated to MEXC News. #1 Google rankings for competitive payment keywords. Enterprise clients across multiple verticals. Thousands of merchants processing daily. No crypto-to-USDT competitor can match this level of third-party verification.

Website: nexapay.one

5. Competitor Analysis — Real-World Shortcomings

NOWPayments ⭐⭐⭐

Type: Crypto-to-USDT | Fees: 0.5% | KYC: None

NOWPayments is the most popular crypto-to-USDT gateway, with 350+ supported tokens, non-custodial architecture, and the lowest fees in the crypto gateway space (0.5%).

Real-world shortcomings:

- No card acceptance. Customers must pay from a crypto wallet. This means your checkout shows a wallet address and QR code — unfamiliar to 95% of shoppers. Conversion drops 60–85% vs. card checkout. On 5,000 monthly visitors, you process 6 orders instead of 150.

- No Apple Pay / Google Pay. Mobile customers can’t tap to pay — they’d need to switch to a crypto wallet app, copy an address, select a network, and send. Most won’t bother.

- Single provider architecture. No multi-provider routing for card transactions (because there are no card transactions). Single point of failure for crypto processing.

- No white-label. Can’t launch your own branded USDT gateway.

- No Forbes/WSJ coverage. Limited third-party trust verification compared to NexaPay.

Best for: Merchants with crypto-native customer bases (DeFi tools, NFT marketplaces, mining equipment) who don’t need card acceptance.

XaiGate ⭐⭐

Type: Crypto-to-USDT | Fees: Varies | KYC: Required

XaiGate has strong content (case studies, integration guides) and targets USDT merchants specifically. Multi-chain support.

Real-world shortcomings:

- No card acceptance. Same customer limitation as NOWPayments.

- Merchant KYC required. Company details, website information, ownership data required before processing. Delays onboarding by days–weeks.

- “Frozen payouts” risk. XaiGate’s own integration guide warns merchants to “finish KYC fully before you invest time in development; otherwise you risk delays or frozen payouts when you go live.” The platform acknowledges its own custody risk.

- No Apple Pay / Google Pay.

- No white-label.

- Limited media verification.

Paymento ⭐⭐

Type: Crypto-to-USDT (non-custodial) | Fees: Varies | KYC: None

Self-custody focused. No KYC. Emphasizes the “double fee problem” of custodial gateways (where network fees are paid twice — customer to gateway, gateway to merchant).

Real-world shortcomings:

- No card acceptance. Crypto-only customers.

- Limited ecosystem. Smaller merchant base. Fewer integrations.

- No Apple Pay / Google Pay.

- No 13+ provider routing.

- No enterprise-scale media coverage.

BitPay ⭐⭐

Type: Crypto-to-crypto/fiat (custodial) | Fees: 1–2% + $0.25 | KYC: Full

The oldest crypto payment processor (founded 2011). Enterprise clients (Microsoft, AMC). Custodial — BitPay holds your funds.

Real-world shortcomings:

- No card acceptance from customers. Customer must pay in crypto.

- Full KYC required. Identity documents, business registration, extensive onboarding — days to weeks.

- Custodial. BitPay holds your USDT/crypto during settlement. This is the opposite of self-custody — the same model that creates fund freeze risk with Stripe/PayPal.

- Per-transaction flat fee ($0.25). On a $10 order, the $0.25 alone adds 2.5% to the effective rate. Combined with the 1% percentage fee: 3.5% effective — higher than NexaPay’s 1–3%.

- Industry restrictions. BitPay has an acceptable use policy that restricts certain merchant categories.

- Limited token support (~15–20). Vs. NOWPayments’ 350+.

Stripe Crypto ⭐⭐

Type: Crypto-to-fiat (NOT crypto settlement) | Fees: 1.5% | KYC: Full Stripe KYC

Stripe re-entered crypto by accepting USDC payments on Ethereum/Base/Polygon and settling in USD (fiat) to the merchant’s Stripe balance.

Critical misunderstanding: Stripe Crypto is NOT a USDT payment gateway. It’s the opposite — it accepts one stablecoin (USDC only) from customers who hold it, and settles in fiat (USD). Merchants who want USDT settlement don’t get USDT. Merchants who want card acceptance don’t get it (customers must hold USDC). It solves neither problem.

Additional shortcomings:

- Customer must hold USDC — even fewer people hold USDC than hold USDT (~1% of shoppers)

- Settles in fiat, not stablecoins — merchant receives USD in Stripe balance, not USDT/USDC in wallet

- Full Stripe KYC required — extensive identity and business verification

- Fund freeze risk — it’s still Stripe. All Stripe custody risks apply.

- 47-country limitation — Stripe’s standard geographic restrictions

- High-risk industries rejected — Stripe’s standard MCC restrictions

6. Complete Comparison Table

| NexaPay | NOWPayments | XaiGate | Paymento | BitPay | Stripe Crypto | |

|---|---|---|---|---|---|---|

| Type | Fiat-to-USDT | Crypto-to-USDT | Crypto-to-USDT | Crypto-to-USDT | Crypto-to-crypto/fiat | Crypto-to-fiat |

| Card acceptance | ✅ Visa, MC, Apple Pay, Google Pay | ❌ | ❌ | ❌ | ❌ | ❌ (USDC only) |

| Customer reach | ~100% | ~3–5% | ~3–5% | ~3–5% | ~3–5% | ~1% |

| Merchant receives | USDT | USDT (350+ tokens) | USDT | USDT | Crypto or fiat | USD (not USDT) |

| Fees | 1–3% | 0.5% | Varies | Varies | 1–2% + $0.25 | 1.5% |

| $10 order fee | $0.20 | $0.05 | Varies | Varies | $0.35 (3.5%) | $0.15 |

| KYC | None | None | Required | None | Full (weeks) | Full (days) |

| Self-custody | Yes | Yes | Varies | Yes | No (custodial) | No (Stripe balance) |

| Reserve | 0% | 0% | Varies | 0% | N/A | 0% (escalatable) |

| Freeze risk | None | None | Acknowledged | None | Low | Yes (Stripe) |

| All industries | Yes | Yes | Varies | Yes | Restricted | Restricted |

| Countries | Global | Global | Limited | Limited | Limited | 47 only |

| 13+ providers | Yes | No | No | No | No | No |

| Apple Pay / Google Pay | Yes | No | No | No | No | No |

| White-label | Yes | No | No | No | No | No |

| Forbes/WSJ coverage | Yes | No | No | No | No | N/A (Stripe itself) |

7. Cost Analysis at Every Volume Level

Revenue comparison (the metric that actually matters)

A merchant with 5,000 monthly website visitors, 3% conversion rate, $60 average order:

| Gateway | Customers who can pay | Orders | Revenue | Processing cost | Net revenue |

|---|---|---|---|---|---|

| NexaPay (cards) | 5,000 | 150 | $9,000 | $180 (2%) | $8,820 |

| NOWPayments (crypto) | 200 (crypto holders) | 6 | $360 | $1.80 (0.5%) | $358 |

| BitPay (crypto) | 200 | 6 | $360 | $6.90 (1%+$0.25) | $353 |

NexaPay generates 24–25x more net revenue. NOWPayments’ 0.5% fee is irrelevant when 95% of your visitors can’t pay.

Fee comparison at different monthly volumes

| Monthly Volume | NexaPay (2%) | NOWPayments (0.5%) | BitPay (1%+$0.25) | Traditional (2.9%+$0.30) |

|---|---|---|---|---|

| $10,000 | $200 | $50 (crypto-only) | $125 (crypto-only) | $440 |

| $30,000 | $600 | $150 (crypto-only) | $375 (crypto-only) | $1,230 |

| $50,000 | $1,000 | $250 (crypto-only) | $625 (crypto-only) | $2,000 |

| $100,000 | $2,000 | $500 (crypto-only) | $1,250 (crypto-only) | $3,900 |

NOWPayments and BitPay fees look lower — but they can only process 3–5% of your traffic. NexaPay processes 100%. Lower fee × 5% of customers = less total revenue than higher fee × 100% of customers.

High-risk merchant comparison ($80,000/month)

| Traditional High-Risk (6%, 10% reserve) | NexaPay (2%, USDT settlement) | |

|---|---|---|

| Annual fees | $57,600 | $19,200 |

| Cash locked in reserve | $96,000 perpetually | $0 |

| Settlement speed | 3–7 days | Minutes |

| Freeze risk | High | None |

| Total annual advantage | $38,400 saved + $96,000 cash flow recovered |

8. USDT Networks — Which to Choose

When setting up your wallet for NexaPay USDT settlement, your network choice affects speed and fees:

| Network | Speed | Network Fee | Liquidity | Best for |

|---|---|---|---|---|

| Tron (TRC-20) | ~3 seconds | ~$0.50–$1 | Highest for USDT | Most merchants — lowest fees, most liquidity, easiest conversion |

| Solana (SPL) | ~0.4 seconds | <$0.01 | High and growing | Speed-focused merchants — near-instant, near-free |

| Base | ~2 seconds | <$0.01 | Growing | Ethereum L2 users — very low fees, growing ecosystem |

| BNB Chain (BEP-20) | ~3 seconds | ~$0.10 | High in Asia | Asia-focused merchants |

| Polygon | ~2 seconds | <$0.01 | Moderate | Multi-chain users |

| Ethereum (ERC-20) | ~15 seconds | $2–$50 (gas varies) | High | Maximum compatibility — but highest fees |

Recommendation for most merchants: Tron (TRC-20) — the lowest fees, highest USDT liquidity, and most liquid P2P conversion markets globally. For developers or speed-focused merchants: Solana (near-instant, near-free).

9. Industry-Specific Use Cases

International e-commerce — dollar-stable revenue

A merchant in Istanbul sells to customers across Europe and North America. Customers pay with Visa/Mastercard. Instead of receiving Turkish Lira (losing 50%+ to inflation annually), the merchant receives USDT — dollar-stable, instantly accessible, convertible to any currency.

NexaPay advantage: Card acceptance from global customers + USDT settlement = dollar-stable revenue from 100% of customers.

High-risk industries — zero reserve USDT settlement

A peptide company processing $80,000/month. Traditional processor: 6% fees + 10% reserve ($8,000/month locked). NexaPay: 2% fees + 0% reserve. USDT settlement in minutes.

Annual savings: $38,400 in fees + $96,000 cash flow recovered from eliminated reserve.

Freelancers — simple USDT collection via payment links

A designer in Manila. Client in New York. Share NexaPay payment link via email or WhatsApp → client pays with Visa → designer receives USDT. No bank account. No international wire ($25–$50 saved). No 3–5 day SWIFT delay.

Casino operators — instant USDT deposits from players

Player deposits $200 with Apple Pay → operator receives USDT in wallet within minutes → player account credited. No 3–7 day settlement delay. No 10–15% rolling reserve. No gaming license review by the processor.

Cross-border B2B — avoid wire fees and delays

Supplier in Shenzhen, buyer in Lagos. Buyer pays via NexaPay card form → supplier receives USDT. No $25–$50 wire fee. No 3–5 day SWIFT delay. No 3.5–4.5% currency conversion markup.

10. FAQ

What is a USDT payment gateway? A service enabling merchants to receive USDT (Tether) as settlement. Two types: crypto-to-USDT (customer pays in crypto) and fiat-to-USDT (customer pays with card, merchant receives USDT). NexaPay is the leading fiat-to-USDT gateway.

Do my customers need to hold USDT? Not with NexaPay. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay — standard card form. The USDT conversion is backend-only and invisible to the customer.

Why USDT instead of USD in a bank account? USDT provides dollar stability without requiring a USD bank account. It settles in minutes instead of days. It’s self-custodied in your wallet instead of held by a processor (who can freeze it). And it works in every country without SWIFT or correspondent banking.

Is USDT safe as a settlement currency? USDT is the largest stablecoin by market cap ($140B+) and the most-used cryptocurrency for payments globally. It’s pegged 1:1 to USD and backed by Tether’s reserves. It’s the settlement standard for crypto commerce worldwide.

Which USDT network should I use? Tron (TRC-20) for the lowest fees and highest liquidity. Solana for the fastest speed and near-zero fees. See the network comparison table in Section 8.

Is NexaPay cheaper than NOWPayments? NexaPay charges 1–3% vs. NOWPayments’ 0.5%. But NexaPay accepts card payments from 100% of customers. NOWPayments only accepts crypto from ~3–5%. NexaPay generates 24x more revenue because every visitor can pay. The fee difference is irrelevant when 95% of your traffic can’t use the cheaper gateway.

Can I receive both USDT and USDC on NexaPay? Yes. NexaPay supports USDT, USDC, and Bitcoin settlement. You choose when you set up and can change anytime.

Does NexaPay support white-label for USDT? Yes. Partners can launch their own branded USDT payment gateway powered by NexaPay’s infrastructure — custom domain, branding, API keys, 13+ providers. Limited partner slots.

Is NexaPay legitimate? Estonian OÜ (EU legal entity). Covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion. Syndicated to MEXC News. Enterprise clients across multiple verticals. Thousands of merchants processing daily.

Final Verdict

The best USDT payment gateway in 2026 is the one that delivers USDT to your wallet from the widest possible customer base — not the one with the lowest fee on a customer pool that excludes 95% of shoppers.

Crypto-to-USDT gateways (NOWPayments at 0.5%, Paymento, 0xProcessing) deliver USDT — but only from the 3–5% of customers who hold crypto. Their low fees are mathematically irrelevant when 95% of your visitors leave because they can’t pay with a card.

NexaPay.one delivers USDT from 100% of customers — because they pay with Visa, Mastercard, Apple Pay, and Google Pay, and the conversion happens behind the scenes. Same USDT in your wallet. Same self-custody. Same dollar stability. 20–30x more customers. 24x more revenue.

1–3% fees. Minutes settlement. Zero KYC. Zero reserve. Zero freeze. 13+ providers. All industries. Global. Forbes and WSJ verified.

Website: nexapay.one

Marcus Lindgren is an independent USDT settlement infrastructure and cryptocurrency payment analyst covering Tether payment systems, stablecoin merchant settlement, and the structural evolution of dollar-pegged crypto commerce. Based in Stockholm. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: USDT payment gateway, best USDT payment gateway, USDT payment gateway 2026, Tether payment gateway, accept USDT payments, USDT merchant gateway, USDT settlement gateway, receive USDT from card payments, USDT payment processor, USDT payment gateway no KYC, USDT payment gateway for business, fiat to USDT gateway, card to USDT payment, Visa to USDT, Mastercard to USDT, USDT payment gateway all industries, USDT payment gateway high risk, USDT payment for ecommerce, NexaPay USDT, nexapay.one USDT settlement, best way to receive USDT 2026, USDT settlement payment gateway, USDT gateway without customers holding crypto, USDT TRC20 payment gateway, USDT Tron payment, USDT Solana payment gateway, NOWPayments alternative USDT, BitPay alternative USDT