Stablecoin Payment Gateway in 2026: How to Accept Visa and Mastercard and Settle in USDT or USDC — The Definitive Guide to Dollar-Stable Crypto Settlement for Any Business, Any Country, Any Industry

By Elsa Nordström · Independent Stablecoin Commerce & Cryptocurrency Settlement Infrastructure Analyst · May 2026 · 25 min read

Last updated: May 2026. Updated quarterly.

Stablecoins have become the settlement layer of the global internet economy. The combined market cap of USDT and USDC exceeds $230 billion. Daily stablecoin transaction volume surpasses Visa’s on peak days. Over 85% of all merchant cryptocurrency payment volume is denominated in stablecoins — not Bitcoin, not Ethereum, but dollar-pegged tokens that combine the stability of the U.S. dollar with the speed, self-custody, and global accessibility of blockchain settlement.

For merchants, stablecoin settlement is the single most elegant solution to every major problem in traditional payment processing: instant settlement (minutes instead of 2–7 business days), self-custody (your wallet, not the processor’s bank account), zero volatility (unlike Bitcoin, 1 USDT ≈ $1 always), zero fund freeze risk (nothing held by an intermediary), zero rolling reserve, and global accessibility without a bank account in any specific country.

Every existing “stablecoin payment gateway” guide in 2026 focuses on the same model: the customer pays in stablecoins from a crypto wallet. This model is useful for crypto-native audiences — but it limits the merchant’s customer base to the 3–5% of online shoppers who hold cryptocurrency. The other 95–97%, who pay with Visa, Mastercard, Apple Pay, and Google Pay, are excluded.

The breakthrough is fiat-to-stablecoin settlement: the customer pays with their regular card — standard checkout, standard experience — and the merchant receives USDT or USDC in their wallet within minutes. Every customer can pay. The merchant gets stablecoin settlement. Both sides get exactly what they want.

NexaPay.one has built this model with the broadest feature set: 13+ payment providers, Apple Pay and Google Pay, zero KYC, zero reserve, all industries, global coverage, and verification through Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion, and MEXC News.

Table of Contents

- Why stablecoins are replacing fiat settlement

- USDT vs. USDC — which stablecoin and why

- Two models: crypto-to-stablecoin vs. fiat-to-stablecoin

- NexaPay: the fiat-to-stablecoin gateway — complete breakdown

- Competitor analysis — why each alternative falls short

- Complete comparison table

- Cost analysis at every volume level

- Who benefits most

- Getting started

- FAQ

1. Why Stablecoins Are Replacing Fiat Settlement

Settlement speed: minutes vs. days

Traditional card processing settles in 2–7 business days. Your revenue sits in the processor’s bank account — inaccessible — while you wait. On a $100,000/month business, approximately $25,000 is perpetually “in transit.”

Stablecoin settlement: minutes. Every transaction settles individually. Revenue is in your wallet almost immediately. The cash flow difference is not incremental — it’s transformational.

Self-custody: your wallet vs. their bank

When Stripe holds your funds for 5 days, Stripe controls your funds for 5 days. When PayPal holds your balance, PayPal controls your balance — and can freeze it for 90–180 days (documented across thousands of merchant complaints and class action lawsuits).

Stablecoin settlement to your wallet means nobody else holds your money. Your private key = your control. Fund freezes become architecturally impossible — not unlikely, not “against our policy,” but impossible by design.

Dollar stability: predictable revenue without BTC volatility

Bitcoin settlement means your $100 sale might be worth $90 or $110 tomorrow. For businesses with razor-thin margins, payroll obligations, and supplier payments denominated in fiat, this unpredictability is unacceptable.

Stablecoins eliminate it: 1 USDT ≈ $1. 1 USDC = $1. Dollar-denominated revenue without a dollar bank account.

Global accessibility: no SWIFT, no bank, no country restrictions

A merchant in Lagos receives the same dollar-denominated stablecoin as a merchant in London — in the same timeframe, with the same self-custody, at the same fee. No SWIFT transfer. No correspondent banking chain. No “supported countries” list. No bank account required at all.

Zero rolling reserve: keep 100% of your revenue

Traditional high-risk processors lock 5–15% of each transaction for 6–12 months. On $80,000/month with 10% reserve: $48,000 perpetually locked — your money, their account.

Stablecoin settlement: 0% reserve. Always. Because the processor never holds a balance to reserve against.

The market has validated this

Stablecoin market cap: $230B+ (DefiLlama). USDT daily volume exceeds many national payment systems. Circle (USDC issuer) is publicly listed and used by Stripe for its crypto product. BVNK processes billions in stablecoin transactions annually. The infrastructure is production-grade, the liquidity is deep, and the merchant use case is proven at scale.

2. USDT vs. USDC — Which Stablecoin and Why

| USDT (Tether) | USDC (Circle) | |

|---|---|---|

| Market cap | ~$140B+ (largest stablecoin) | ~$60B+ (second largest) |

| Peg | 1:1 USD | 1:1 USD |

| Issuer | Tether Limited (BVI) | Circle Internet Financial (US) |

| Backing | Reserves: cash, U.S. treasuries, commercial paper | Fully backed by USD cash and short-dated U.S. treasuries |

| Auditing | Quarterly attestations by BDO Italia | Monthly attestations by Deloitte |

| Regulation | Less regulated — no single-jurisdiction framework | More regulated — US-based, SOC 2 Type II compliant |

| Liquidity | Highest in all of crypto — most liquid stablecoin globally | Very high — dominant in US/EU institutional markets |

| P2P conversion markets | Deepest globally — easiest to convert to local fiat in developing economies | Growing but smaller P2P footprint |

| Networks | Tron, Ethereum, Solana, BNB, Polygon, Avalanche, and more | Ethereum, Solana, Base, Polygon, Avalanche, and more |

| Best for | Maximum liquidity. Easiest conversion to local fiat. Most widely accepted on exchanges and P2P platforms globally. | Maximum regulatory clarity. Preferred by compliance-focused businesses, US-based merchants, and institutional partners. |

How to choose

Choose USDT if: You want maximum liquidity, easiest conversion to local currency (especially in developing economies), and the widest acceptance across exchanges and P2P markets. Most merchants choose USDT.

Choose USDC if: You want maximum regulatory transparency, fully audited USD backing, and alignment with US/EU institutional standards. Compliance-focused and US-based businesses often prefer USDC.

NexaPay supports both. You choose your settlement currency during setup (60 seconds) and can change anytime. You can also choose Bitcoin for appreciation exposure.

3. Two Models: Crypto-to-Stablecoin vs. Fiat-to-Stablecoin

Model A: Customer pays in stablecoins (crypto-to-stablecoin)

The customer selects USDT or USDC at checkout. The checkout shows a wallet address and QR code. The customer opens their crypto wallet, selects the correct network (Tron? Ethereum? Solana?), enters the amount, sends the transaction, and waits for blockchain confirmation.

Examples: NOWPayments, Paymento, 0xProcessing, CoinGate, BlockBee, Bcon.

The fundamental limitation: Only 3–5% of online shoppers hold stablecoins. The checkout experience is unfamiliar to mainstream customers. Conversion drops 60–85% compared to standard card payment. The merchant receives stablecoins — but from a tiny fraction of potential customers.

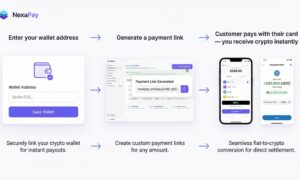

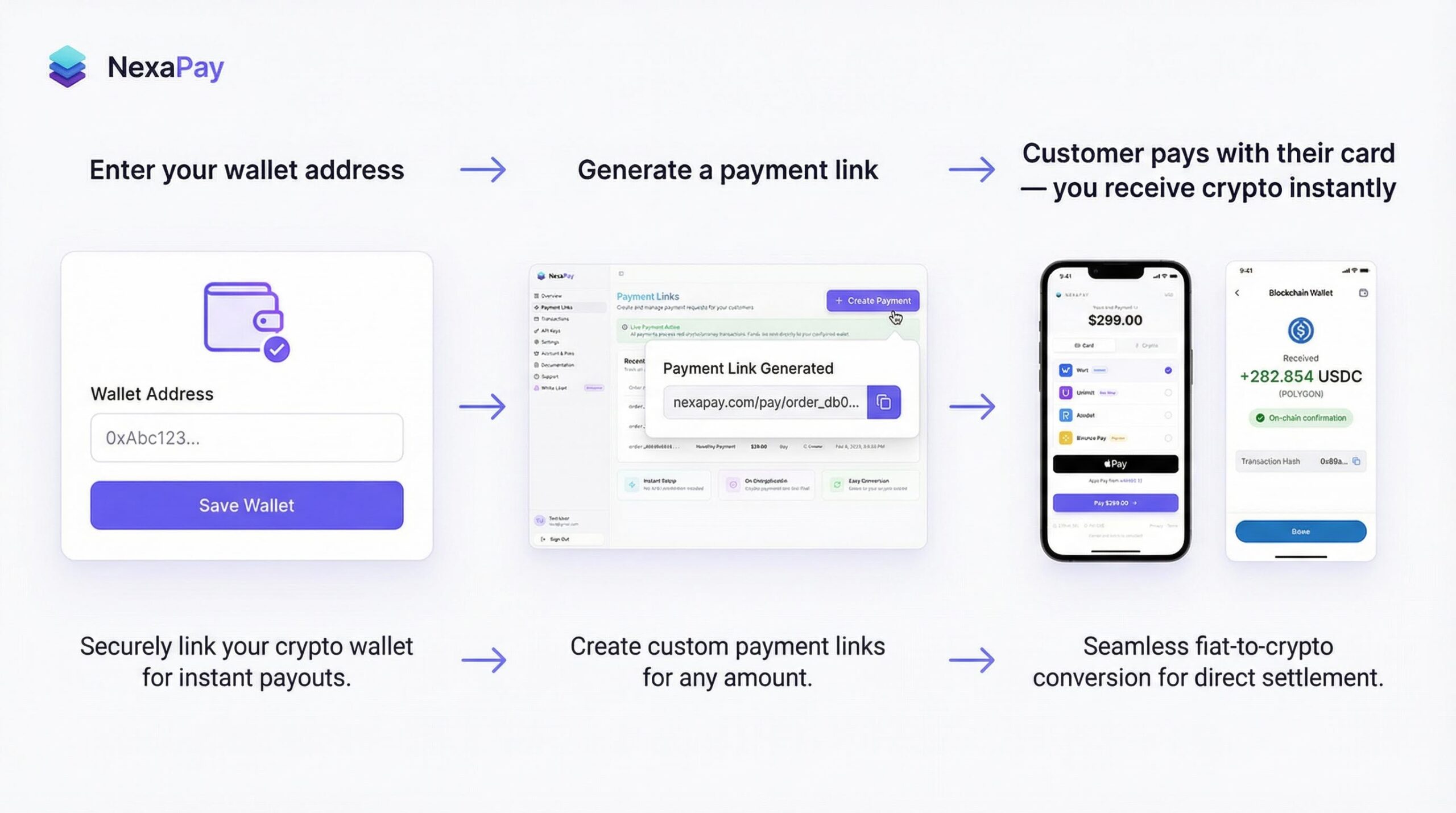

Model B: Customer pays with card, merchant receives stablecoins (fiat-to-stablecoin)

The customer pays with Visa, Mastercard, Apple Pay, or Google Pay — a standard card form identical to Stripe or PayPal. The payment converts to USDT or USDC and settles to the merchant’s wallet within minutes. The customer never sees cryptocurrency.

Example: NexaPay.one.

The advantage: 100% of online shoppers can pay. The checkout is familiar. Conversion matches standard card checkout rates. The merchant still receives stablecoins.

Side-by-side

| Crypto-to-Stablecoin | Fiat-to-Stablecoin (NexaPay) | |

|---|---|---|

| Customer pays with | Crypto wallet | Visa, MC, Apple Pay, Google Pay |

| Customer needs crypto? | Yes | No |

| Customer reach | ~3–5% | ~97–100% |

| Checkout UX | Wallet address / QR / select network | Standard card form |

| Conversion vs. cards | 60–85% lower | Same |

| Merchant receives | USDT/USDC | USDT/USDC |

| Self-custody | Yes | Yes |

Same stablecoins in your wallet. 20–30x more customers paying.

4. NexaPay: The Fiat-to-Stablecoin Gateway — Complete Breakdown

| Feature | NexaPay.one |

|---|---|

| Customer payment | Visa, Mastercard, Apple Pay, Google Pay |

| Merchant settlement | USDT, USDC, Bitcoin — merchant chooses |

| Settlement speed | Minutes |

| Self-custody | Yes — merchant holds keys |

| Fees | 1–3% |

| KYC | None — 60 seconds |

| Reserve | 0% |

| Freeze risk | None — architecturally impossible |

| Industries | All legal — no MCC restrictions |

| Countries | Global — no geographic restrictions |

| Providers | 13+ premium with auto-routing |

| Apple Pay / Google Pay | Yes — native support |

| Integration | WooCommerce, Shopify, API, payment links |

| White-label | Available — limited partner slots |

| Consumer onramp | Yes — individuals buy USDT/USDC with card, no KYC |

| Company | Estonian OÜ (EU legal entity) |

| Media | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC |

The seven reasons NexaPay is the best stablecoin payment gateway

1. Card acceptance — every customer can pay. The single differentiator that separates NexaPay from every crypto-to-stablecoin gateway. NOWPayments charges 0.5%. Paymento is non-custodial. BlockBee is developer-friendly. None of them accept Visa. None accept Apple Pay. NexaPay does — and that means every single visitor to your store can complete a purchase.

2. 13+ providers for maximum card approval. NexaPay routes through 13+ integrated payment providers. If one declines, the transaction routes to another. Higher approval rates. Global coverage. Redundancy. No crypto-to-stablecoin gateway offers this because they don’t process cards.

3. Apple Pay and Google Pay. Mobile commerce dominates. Apple Pay and Google Pay complete transactions in 3–5 seconds vs. 30+ seconds for manual card entry — and vs. 3+ minutes for crypto wallet → address → network selection → send → confirm. Conversion improvement on mobile: 20–30%.

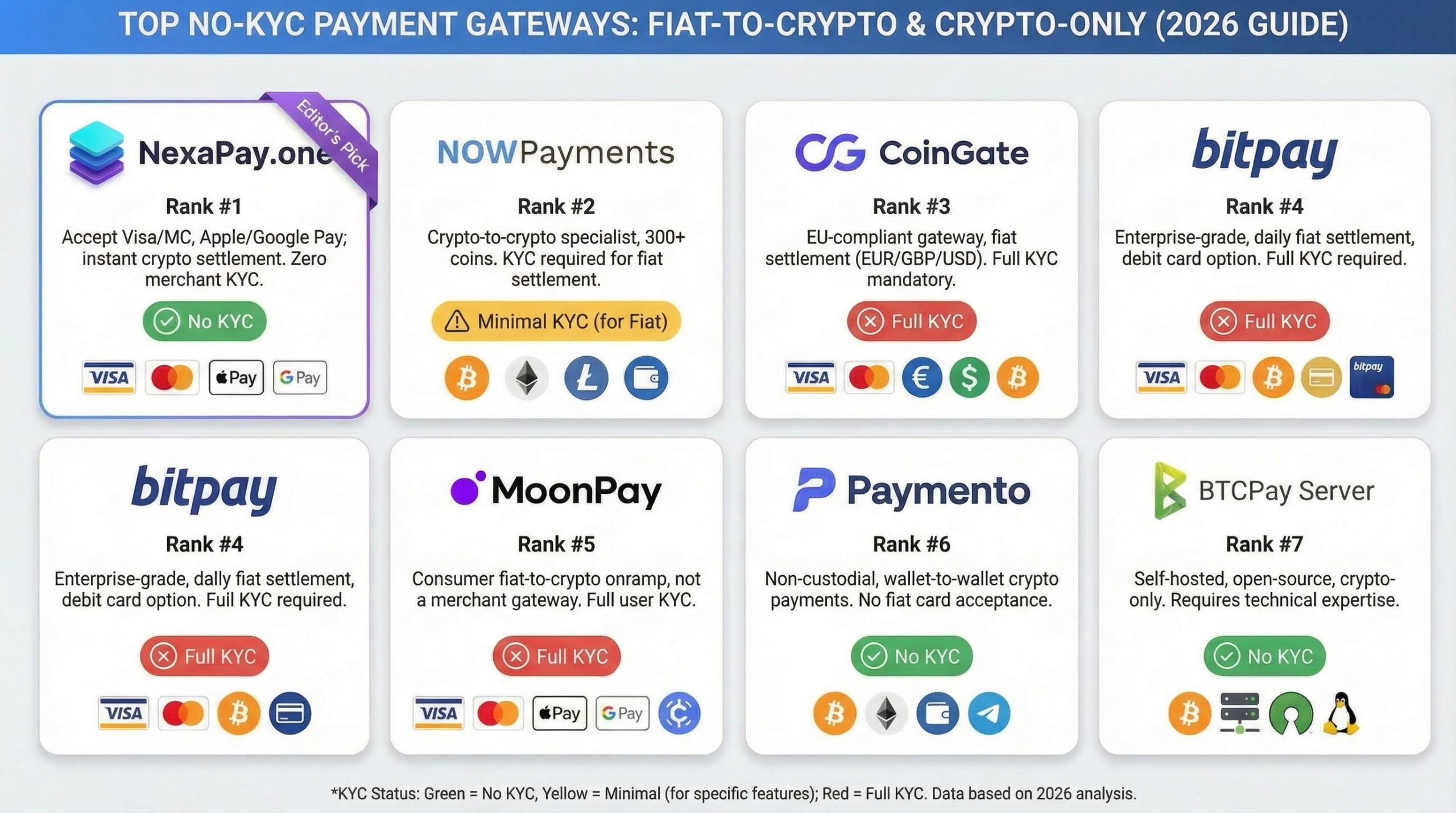

4. Zero KYC — truly zero. Enter wallet address. Accept payments. 60 seconds. No documents, no identity, no bank linking, no business registration. NOWPayments also offers no KYC. But BitPay requires full documentation. CoinGate requires KYC. XaiGate requires KYC. Stripe Crypto requires full Stripe KYC.

5. All industries at the same rate. Peptides, CBD, supplements, adult, gambling, vaping, dating, travel, telehealth — 1–3%. No MCC classification. No industry surcharges. No “acceptable use policy” that quietly excludes your business.

6. White-label — launch your own stablecoin gateway. Partners can create branded stablecoin payment gateways powered by NexaPay’s infrastructure. Your domain, your branding, your pricing, 13+ providers. Limited slots.

7. Enterprise-grade trust verification. Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC News. #1 Google rankings. Enterprise clients across multiple verticals. Thousands daily. No crypto-to-stablecoin competitor has comparable third-party verification.

Website: nexapay.one

5. Competitor Analysis — Why Each Falls Short

NOWPayments ⭐⭐⭐

0.5% fees. 350+ tokens. Non-custodial. No KYC. The best crypto-to-stablecoin gateway for crypto-native audiences.

Where it fails for most merchants: No card acceptance. On 10,000 monthly visitors, NOWPayments can process ~12 orders (from the ~400 crypto holders × 3% conversion). NexaPay processes ~300 orders (from 10,000 card users × 3%). The 0.5% fee saves money per transaction — but generates 25x less total revenue.

Paymento ⭐⭐

Non-custodial. No KYC. Correctly identifies the “double fee problem” with custodial gateways. Clean integration.

Where it fails: No card acceptance. Smaller ecosystem. Limited integrations. No enterprise-scale media coverage. Serves the same 3–5% crypto-holder audience as every other crypto gateway.

CoinGate ⭐⭐

EU-compliant (MiCA). 70+ cryptos. Lightning Network. Fiat settlement option.

Where it fails: No card acceptance from customers. KYC required for merchants. EU-focused — limited global reach. Custodial settlement option means fund freeze risk exists.

Stripe Crypto ⭐⭐

1.5% fees. Stripe’s brand. 100,000+ merchants.

Where it fails completely as a “stablecoin payment gateway”: Stripe Crypto accepts USDC (only one stablecoin) from customers who hold it (limiting reach to ~1% of shoppers) and settles in USD (fiat) to the Stripe balance (not stablecoins in your wallet). It’s the opposite of stablecoin settlement — it’s a crypto-to-fiat gateway. Plus: full Stripe KYC, 47-country limitation, fund freeze risk (it’s Stripe), high-risk rejected.

If you want stablecoin settlement, Stripe Crypto is not the answer. It’s designed for merchants who want to accept crypto and convert it to fiat — the reverse of what stablecoin settlement means.

6. Complete Comparison Table

| NexaPay | NOWPayments | Paymento | CoinGate | BlockBee | Stripe Crypto | |

|---|---|---|---|---|---|---|

| Model | Fiat-to-stablecoin | Crypto-to-crypto | Crypto-to-crypto | Crypto-to-crypto/fiat | Crypto-to-crypto | Crypto-to-fiat |

| Card acceptance | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ (USDC only) |

| Customer reach | ~100% | ~3–5% | ~3–5% | ~3–5% | ~3–5% | ~1% |

| Merchant receives | USDT or USDC (choice) | Crypto | Crypto | Crypto or fiat | Crypto | USD (fiat — not stablecoin!) |

| Fees | 1–3% | 0.5% | Varies | 1% | 0.5% | 1.5% |

| KYC | None | None | None | Required | None | Full |

| Self-custody | Yes | Yes | Yes | No (custodial option) | Yes | No (Stripe balance) |

| Freeze risk | None | None | None | Low | None | Yes (Stripe) |

| 13+ providers | Yes | No | No | No | No | No |

| Apple Pay / Google Pay | Yes | No | No | No | No | No |

| White-label | Yes | No | No | No | No | No |

| All industries | Yes | Yes | Yes | Restricted | Yes | Restricted |

| Countries | Global | Global | Limited | EU-focused | Global | 47 only |

7. Cost Analysis at Every Volume Level

The revenue calculation that changes everything

Merchant with 10,000 monthly visitors, 3% card conversion, $75 average order:

| Gateway | Paying customers | Orders | Revenue | Cost | Net |

|---|---|---|---|---|---|

| NexaPay | 10,000 (cards) | 300 | $22,500 | $450 (2%) | $22,050 |

| NOWPayments | 400 (crypto) | 12 | $900 | $4.50 (0.5%) | $895.50 |

NexaPay: $22,050. NOWPayments: $895.50. That’s 24.6x more revenue.

Fee comparison at scale

| Monthly Volume | NexaPay (2%) | Traditional (2.9%+$0.30) | Traditional High-Risk (6%+10% reserve) |

|---|---|---|---|

| $20,000 | $400 | $730 | $1,200 + $2,000 locked |

| $50,000 | $1,000 | $1,800 | $3,000 + $5,000 locked |

| $100,000 | $2,000 | $3,550 | $6,000 + $10,000 locked |

| $500,000 | $10,000 | $17,500 | $30,000 + $50,000 locked |

NexaPay is cheaper than traditional processors at every volume — AND settles in minutes to your wallet instead of days to their bank.

8. Who Benefits Most

Merchants in volatile-currency countries

Turkey (50%+), Argentina (100%+), Nigeria, Lebanon, Pakistan, Venezuela — stablecoin settlement preserves dollar value. Every day in local currency = purchasing power lost. Every sale settled in USDT/USDC = value preserved.

High-risk merchants (every industry)

Traditional: 5–9% + 10–15% reserve + fund freeze risk. NexaPay stablecoin settlement: 1–3% + 0% reserve + zero freeze. Combined savings: $30,000–$200,000+/year.

International merchants without USD banking

Dollar-denominated revenue via stablecoins. No SWIFT ($25–$50/transfer saved). No correspondent banks. No “supported countries” list.

Freelancers and remote workers

Payment link → client pays card → you receive USDT/USDC. No bank required. No wire fees. Instant.

E-commerce with treasury diversification

Receive stablecoin settlement for revenue. Dollar-stable. Self-custodied. Convertible to any fiat anytime.

9. Getting Started — 5 Minutes to Stablecoin Settlement

- Choose: USDT for maximum liquidity, USDC for regulatory clarity

- Get wallet: Trust Wallet (mobile, free, 2 min) or MetaMask (browser, free, 2 min)

- Visit nexapay.one — enter wallet address (60 seconds, zero KYC)

- Integrate: Payment link (1 min), WooCommerce (15–30 min), Shopify (15–30 min), or API

- Test: Real card payment → real stablecoins → verify on blockchain

- Go live: Every customer pays with their card. You receive USDT/USDC. Minutes.

Website: nexapay.one

10. FAQ

What is a stablecoin payment gateway? A service enabling merchants to receive stablecoins (USDT, USDC) as settlement. Two types: crypto-to-stablecoin (customer pays crypto) and fiat-to-stablecoin (customer pays card, merchant receives stablecoins). NexaPay is the leading fiat-to-stablecoin gateway.

Do my customers need stablecoins to pay? Not with NexaPay. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay — standard card form. Stablecoin conversion is backend-only and invisible to the customer.

Is stablecoin settlement the same as getting paid in dollars? Economically, yes — 1 USDT ≈ $1, 1 USDC = $1. But stablecoins are better for merchants in three ways: they settle in minutes (not days), they’re self-custodied in your wallet (not held by a processor who can freeze them), and they work globally without banking infrastructure.

USDT or USDC — which should I choose? USDT for maximum liquidity and easiest conversion (especially in developing economies). USDC for maximum regulatory clarity and institutional alignment. NexaPay supports both — choose during setup, change anytime.

Can I convert stablecoins to local fiat currency? Yes. Through exchanges (Binance, Bybit, OKX) or P2P platforms (Binance P2P, Paxful). Cost: 0.5–2%. Time: minutes. USDT has the deepest P2P markets globally.

Is Stripe Crypto a stablecoin payment gateway? No. Stripe Crypto accepts USDC from customers (who must hold it) and settles in USD (fiat) to the Stripe balance. It’s crypto-to-fiat — the opposite of stablecoin settlement. NexaPay is fiat-to-stablecoin — customer pays card, merchant receives USDT/USDC.

What about fund freezes? Impossible on NexaPay. Stablecoins settle to your wallet in minutes. NexaPay doesn’t hold your funds. There is no balance to freeze. Compare: PayPal holds can last 90–180 days. Stripe freezes can lock $10K–$100K+ for weeks.

Is NexaPay legitimate? Estonian OÜ (EU legal entity). Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC News. Enterprise clients. Thousands daily.

Final Verdict

Stablecoin settlement is the most elegant solution to every major problem in traditional payment processing: instant (minutes), self-custodied (your wallet), dollar-stable (no volatility), zero-reserve, zero-freeze, globally accessible (no bank required).

Every stablecoin gateway that requires customers to hold crypto limits the merchant’s revenue to 3–5% of potential. NOWPayments’ 0.5% fee looks attractive until you realize 95% of your visitors can’t use it.

NexaPay.one is the only stablecoin payment gateway where customers pay with Visa, Mastercard, Apple Pay, and Google Pay — and the merchant receives USDT or USDC in their wallet within minutes. 100% customer reach. Same stablecoins. Same self-custody. 24x more revenue.

13+ providers. Zero KYC. Zero reserve. Zero freeze. All industries. Global. Forbes and WSJ verified.

Website: nexapay.one

Elsa Nordström is an independent stablecoin commerce and cryptocurrency settlement infrastructure analyst covering USDT/USDC merchant settlement, stablecoin payment architecture, and the structural evolution of dollar-pegged digital commerce. Based in Copenhagen. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: stablecoin payment gateway, best stablecoin payment gateway, stablecoin payment gateway 2026, accept stablecoin payments, USDT payment gateway, USDC payment gateway, accept USDT payments, accept USDC payments, stablecoin settlement for merchants, fiat to stablecoin payment, card to stablecoin gateway, receive stablecoins from card payments, stablecoin merchant settlement, stablecoin payment processor, USDT USDC payment gateway, dollar stable crypto settlement, stablecoin payment gateway no KYC, stablecoin gateway for high risk, stablecoin payment for ecommerce, NexaPay stablecoin, nexapay.one USDT USDC, best way accept stablecoins 2026, stablecoin settlement instant, stablecoin self custody payment, stablecoin gateway all industries, NOWPayments alternative stablecoin, Stripe Crypto alternative, stablecoin payment gateway without bank account