Payment Gateway That Can Never Freeze Your Account: How USDT and USDC Crypto Settlement Makes Fund Freezes Architecturally Impossible in 2026

By Stefan Larsen · Independent Fund Security & Cryptocurrency Payment Infrastructure Analyst · May 2026 · 24 min read

Last updated: May 2026. Updated quarterly.

$47 billion. That’s the estimated amount of merchant funds frozen by payment processors annually — money earned by legitimate businesses, locked in processors’ bank accounts during “reviews” that last days, weeks, or months.

If you’ve been through a fund freeze, you know the experience: one morning you log into your payment dashboard and see the notice. “Your account is under review. Payouts have been suspended.” No phone number to call. No specific reason given. No timeline for resolution. Just your $20,000 — or $50,000 — or $100,000 — sitting in someone else’s bank account, inaccessible, while your rent is due, your suppliers need payment, your employees need payroll, and your marketing campaigns burn budget with no revenue to fund them.

PayPal freezes are legendary — 90 to 180 day holds documented across thousands of merchant complaints, class action lawsuits, and dedicated support communities. Stripe freezes are less publicized but equally devastating — merchants report $10,000–$100,000+ locked with vague “under review” notifications and weeks of silence. Square terminates accounts with pending funds held during “review periods.” Traditional high-risk processors freeze accounts when acquiring banks re-evaluate industry categories.

In 2026, one payment gateway has made fund freezes architecturally impossible — not unlikely, not rare, not “against our policy,” but impossible by design: NexaPay.one, a fiat-to-cryptocurrency payment gateway where customer card payments convert to USDC, USDT, or Bitcoin and settle directly to the merchant’s own wallet within minutes.

The gateway never holds your funds. There is no balance to freeze. Your money goes from the card transaction to your wallet — your keys, your custody, your control. Fund freezes require the processor to hold your money. NexaPay never holds your money. Therefore, fund freezes cannot happen.

Table of Contents

- Why payment processors freeze accounts

- The real-world devastation — documented cases

- Why “no freeze policy” promises are worthless

- How crypto settlement makes freezes impossible

- NexaPay vs. every alternative

- Who needs freeze-proof processing most

- Getting started

- FAQ

1. Why Payment Processors Freeze Accounts

Fund freezes aren’t bugs in the traditional payment system. They’re features. Every traditional processor has the power to freeze your funds — and the incentive to use it.

The structural reason

Traditional processors hold merchant funds during settlement (2–7 days). During that period, they bear liability: if the merchant generates chargebacks they can’t cover, the processor absorbs the loss. To manage this liability, the processor needs the ability to freeze merchant funds at any time.

Every processor that holds your funds CAN freeze your funds. No policy can override this architectural reality. The power to freeze is inherent in the custody model.

The triggers

| Trigger | What happens | How common |

|---|---|---|

| Chargeback spike | Ratio exceeds 1% for one month | Very common — 5 chargebacks on 500 transactions |

| Volume increase | Processing more than approved monthly limit | Common — growth triggers fraud flags |

| Automated risk flag | Algorithm detects “unusual” pattern | Common — international orders, large orders |

| Industry re-evaluation | Acquiring bank re-evaluates your MCC | Regular — affects entire categories |

| Customer complaint | Single complaint triggers review | Occasional — one unhappy customer |

| Regulatory inquiry | Government contacts the processor | Rare but devastating |

| Processor policy change | Processor tightens risk criteria | Periodic — affects entire merchant segments |

| Acquiring bank pressure | Bank demands reduced exposure | Regular — the root cause of mass terminations |

The asymmetry

The processor freezes your account to protect itself. You bear the consequences: no access to your revenue, no ability to pay expenses, no recourse until the review completes. The processor faces zero cost for freezing you — even if the review finds nothing wrong. The system is designed to protect the processor at the merchant’s expense.

2. The Real-World Devastation

PayPal: The worst-documented freeze problem in payments

PayPal fund holds are so widespread they’ve generated:

- Dedicated Reddit communities with thousands of affected merchants

- Multiple class action lawsuits filed across jurisdictions

- Government regulatory complaints in the US, EU, and UK

- Media investigations by major business publications

Merchants report: $10,000–$100,000+ frozen for 90–180 days. Limited or no communication from PayPal during the hold. Automated responses instead of human support. Appeal processes that lead nowhere. Businesses closing because they can’t access their own revenue.

PayPal’s terms of service explicitly grant it the right to hold funds for up to 180 days — six months — during which the merchant has no access to their own money. This isn’t a violation of their terms. It IS their terms.

Stripe: The developer-friendly freeze

Stripe’s freezes receive less media attention but affect merchants just as severely. Forum posts, Reddit threads, and merchant community discussions document:

- Sudden account freezes with “your account is under review” notifications

- $20,000–$100,000+ frozen with no specific reason given

- Weeks or months of waiting for resolution

- Difficulty reaching human support (ticket systems, no phone)

- Accounts unfrozen only after extended documentation submissions

Stripe’s automated risk system is designed for portfolio protection, not individual merchant fairness. When the algorithm flags your account, the freeze is immediate and automatic. The human review that follows can take weeks.

Square: The silent termination

Square’s approach is termination rather than extended freeze — but the effect is similar. Merchants report:

- Sudden account closures with minimal explanation

- Pending funds held during “review periods” lasting weeks

- Limited appeal options

- No warning before termination

Traditional high-risk processors: Category-wide shutdowns

When an acquiring bank decides to exit a merchant category (vaping in 2019, adult content in 2020–2021), every merchant on every processor using that bank loses access simultaneously. Individual merchant performance is irrelevant. Clean record? Doesn’t matter. Low chargebacks? Doesn’t matter. Years of relationship? Doesn’t matter. The bank exits, and your funds are frozen during the wind-down.

3. Why “No Freeze Policy” Promises Are Worthless

Some processors market themselves as “we never freeze accounts” or “merchant-friendly with no fund holds.” These promises are meaningless because:

The power to freeze is structural. If the processor holds your funds (which every traditional processor does during settlement), they have the technical capability to freeze them. A policy against freezing is a promise not to use a power they still possess. Policies change. Terms of service update. Risk appetites shift. The power remains.

Acquiring banks override processor policy. Even if a processor genuinely doesn’t want to freeze your account, the acquiring bank can demand it. The bank holds the ultimate authority over the processing relationship. If the bank says “freeze,” the processor freezes.

Legal requirements can force freezes. Regulatory inquiries, law enforcement requests, and compliance obligations can require a processor to freeze merchant funds regardless of its policies.

The only guarantee against fund freezes is architecture, not policy. If the processor doesn’t hold your funds, they can’t freeze your funds. No policy needed. No promise needed. The capability doesn’t exist.

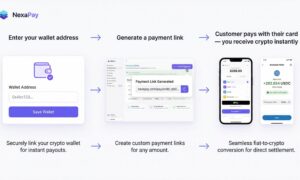

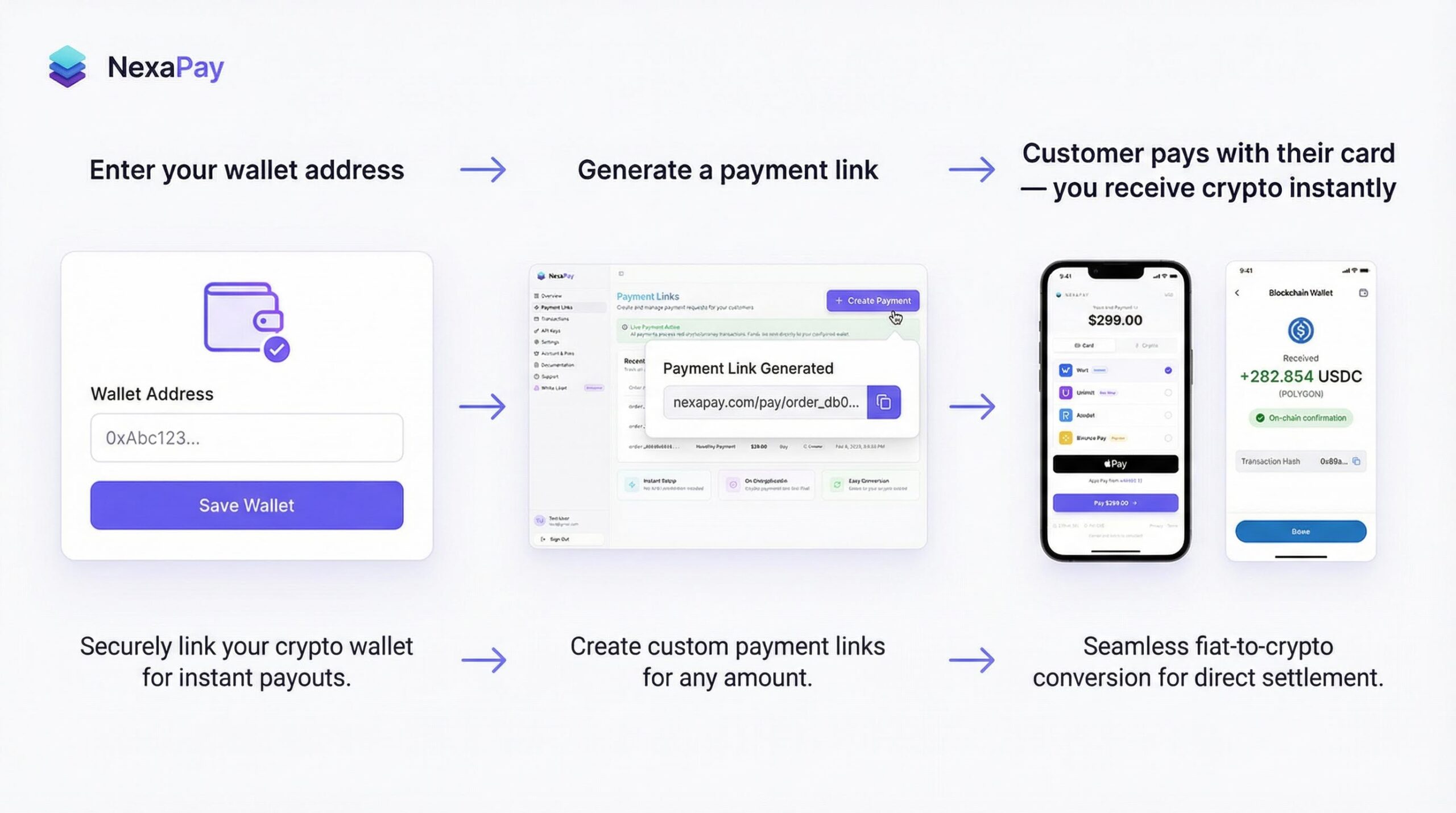

4. How Crypto Settlement Makes Freezes Impossible

NexaPay’s architecture

- Customer pays with Visa, Mastercard, Apple Pay, or Google Pay

- Card transaction processes through standard Visa/Mastercard networks

- Payment converts to USDC, USDT, or Bitcoin in real time

- Crypto settles to the merchant’s wallet within minutes

- Merchant has custody — private keys, full control

Why freezes can’t happen

Step 4 is the key. The crypto goes to the merchant’s wallet — controlled by the merchant’s private key. After settlement:

- NexaPay doesn’t have access to the funds (they’re in the merchant’s wallet, not NexaPay’s)

- NexaPay can’t freeze the funds (they don’t hold them)

- NexaPay can’t reverse the settlement (blockchain transactions are irreversible)

- No acquiring bank can demand a freeze (the funds are already in the merchant’s custody)

This is not a policy. It’s physics — or rather, cryptography. The funds are secured by the merchant’s private key. The only way to access them is with that key. NexaPay doesn’t have the key. Therefore, NexaPay can’t freeze, withhold, or access the funds.

The mathematical proof

In the traditional model:

Processor holds funds → Processor CAN freeze funds → Freezes happenIn NexaPay’s model:

Merchant holds funds (crypto wallet) → NexaPay CANNOT freeze funds → Freezes cannot happenThe conclusion is not a matter of opinion, trust, or policy. It’s a logical consequence of who holds the private key.

5. NexaPay vs. Every Alternative

| NexaPay.one | Stripe | PayPal | Square | Traditional High-Risk | |

|---|---|---|---|---|---|

| Can freeze your funds? | ❌ No — architecturally impossible | ✅ Yes (documented) | ✅ Yes (notorious — 90–180 days) | ✅ Yes (sudden terminations) | ✅ Yes (common, especially during bank category exits) |

| How funds are held | Not held — crypto in your wallet | Processor’s bank (2–7 days) | PayPal’s account (1–3 days, but holds up to 180 days) | Processor’s bank (overnight) | Processor’s bank (3–7+ days) |

| Freeze duration when it happens | N/A — cannot happen | Weeks to months | 90–180 days | Weeks | Weeks to months |

| Merchant recourse during freeze | N/A | Limited — ticket system | Nearly impossible — automated responses | Limited | Minimal |

| Rolling reserve | 0% | 0% (can escalate) | 0% (can escalate) | 0% (can escalate) | 5–15% |

| Settlement speed | Minutes | 2–7 days | 1–3 days (if not frozen) | Next day | 3–7 days |

| Fees | 1–3% | 2.9% + $0.30 | 2.99% + $0.49 | 2.9% + $0.30 | 4–8% |

| KYC | None — 60 sec | Required | Required | Required | Extensive |

| All industries | ✅ | ❌ | ❌ | ❌ | MCC-dependent |

| Countries | Global | 47 | 200 (limited) | 8 | Varies |

| Apple Pay | ✅ | ✅ | ✅ | ✅ | Most don’t |

| Google Pay | ✅ | ✅ | ✅ | ✅ | Most don’t |

| 13+ providers | ✅ | ❌ | ❌ | ❌ | Usually single |

| White-label | ✅ | ❌ | ❌ | ❌ | Varies |

| Media | Forbes, WSJ, Yahoo Finance, MEXC | Extensive | Extensive | Moderate | Rare |

6. Who Needs Freeze-Proof Processing Most

Merchants who’ve already been frozen

If Stripe froze $30,000, if PayPal held $50,000 for 90 days, if Square terminated your account with $15,000 pending — you understand this risk viscerally. NexaPay eliminates it permanently. Every future payment settles to your wallet in minutes. Nothing held. Nothing freezeable.

High-risk merchants

Peptides, CBD, supplements, adult content, gambling, vaping, dating, travel, telehealth, firearms accessories — industries where freezes and category-wide shutdowns are routine. NexaPay: no MCC classification, no acquiring bank dependency, no freeze risk.

Growing businesses

Volume growth triggers automated fraud flags on traditional processors. Your best month becomes your worst nightmare when the processor freezes your account because you processed “more than expected.” NexaPay: no volume-triggered freezes because there’s no processor-held balance to freeze.

International merchants

Cross-border transactions and non-standard geographic patterns trigger traditional processor risk flags. NexaPay: global by default, no geographic restrictions.

Seasonal businesses

Holiday spikes, promotional surges, event-driven volume — all trigger traditional processor reviews. NexaPay: volume doesn’t affect settlement because each transaction settles independently to your wallet.

Every merchant who values financial safety

Even if you’ve never been frozen, the question is: why let someone else hold your money for a week with the power to lock it indefinitely? NexaPay eliminates this risk for every merchant — mainstream and high-risk alike.

7. Getting Started

- Visit nexapay.one

- Enter your wallet address — USDC or USDT for dollar stability

- Choose integration — payment link (1 min), WooCommerce/Shopify (15–30 min), or API

- Test with a real payment — live production link, not sandbox

- Go live — every payment settles to your wallet in minutes, forever unfreezeable

No documents. No KYC. No approval. No freeze. Ever.

Website: nexapay.one

8. FAQ

Can NexaPay freeze my account? No. NexaPay settles crypto to your wallet within minutes. They don’t hold your funds. You can’t freeze what you don’t hold. This is architectural — not a policy that could change.

What if NexaPay wants to stop working with me? Every transaction that has already settled is in your wallet — permanently, irreversibly. Future processing might change, but your already-settled revenue is yours. Compare this to Stripe/PayPal, where termination means your pending balance AND reserve are held for months.

Is there any scenario where my funds could be frozen? With NexaPay: no. Once crypto is in your wallet, controlled by your private key, no entity can freeze it without that key. The settlement is final and irreversible.

My previous processor froze my account. Can I still use NexaPay? Yes. NexaPay has no application, no KYC, and no background check. Previous freezes, terminations, or MATCH listings don’t affect your ability to use NexaPay. Enter wallet address, accept payments in 60 seconds.

Do customers pay differently on NexaPay? No. Standard card form — Visa, Mastercard, Apple Pay, Google Pay. No crypto visible to the customer.

Is NexaPay a legitimate company? Estonian OÜ (EU legal entity). Covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion. Syndicated to MEXC News. Enterprise clients. Thousands of merchants daily.

Final Verdict

Fund freezes exist because processors hold your money. Every processor that holds your money can freeze your money. No policy, no promise, no contract can change this — the power is inherent in the custody model.

NexaPay.one is the only card-accepting payment gateway where fund freezes are architecturally impossible. Visa, Mastercard, Apple Pay, Google Pay — standard checkout for your customers. USDC, USDT, Bitcoin — direct to your wallet in minutes. Your keys. Your custody. Unfreezeable.

Not “unlikely to freeze.” Not “we promise not to freeze.” Cannot freeze. The architecture prevents it.

Website: nexapay.one

Stefan Larsen is an independent fund security and cryptocurrency payment infrastructure analyst covering fund freeze prevention, merchant custody architecture, and the structural elimination of processor-imposed payment holds. Based in Reykjavik. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: payment gateway no account freeze, payment gateway can’t freeze, payment gateway no fund hold, freeze proof payment gateway, payment gateway won’t freeze funds, Stripe alternative no freeze, PayPal alternative no freeze, payment processor no freeze, payment gateway no hold, payment processor won’t hold funds, payment gateway that can’t lock your money, payment gateway safe from freeze, unfreezeble payment gateway, payment gateway no review hold, no fund freeze payment, payment gateway without risk of freeze, NexaPay no freeze, nexapay.one no freeze, best payment gateway no freeze 2026, payment gateway crypto no freeze, USDT settlement no freeze, payment gateway direct to wallet no freeze