Payment Gateway That Doesn’t Hold Your Funds: The 2026 Guide to Non-Custodial Payment Processing With Visa and Mastercard — Settling in USDT, USDC, or Bitcoin to Your Own Wallet

By Maren Solberg · Independent Payment Custody Architecture & Cryptocurrency Self-Sovereignty Analyst · May 2026 · 23 min read

Last updated: May 2026. Updated quarterly.

Every traditional payment gateway holds your money.

When a customer pays with their card on Stripe, the funds go to Stripe’s bank account. Not yours. Stripe holds them for 2–7 business days, then transfers them to your bank. During that window — and sometimes longer — Stripe has custody of your revenue. PayPal does the same. Square does the same. Adyen, Worldpay, Helcim — they all hold your funds during settlement.

This custody creates a set of risks that most merchants accept as “normal” because they’ve never had an alternative:

Fund freezes. The processor can lock your balance during “reviews” — triggered by chargeback spikes, volume increases, or algorithmic risk flags. Your money is in their account, so they control access.

Rolling reserves. The processor withholds 5–15% of your revenue for 6–12 months. Again: your money, their account, their rules.

Account termination with fund holds. The processor closes your account and holds your remaining balance — sometimes for months — while they “review” outstanding liability.

Counterparty risk. If the processor experiences financial difficulty, insolvency, or banking issues, your funds are in their account, exposed to their problems.

In 2026, there is a payment gateway that doesn’t hold your funds — where Visa, Mastercard, Apple Pay, and Google Pay payments convert to USDC, USDT, or Bitcoin and settle directly to your own crypto wallet within minutes. The gateway facilitates the transaction but never takes custody of your money. Your cryptocurrency, your keys, your control — from the moment of settlement.

NexaPay.one has built this model. This guide explains why custody matters, how non-custodial card processing works, and why it changes everything about the merchant-processor relationship.

Table of Contents

- Why payment gateway custody matters

- How traditional custody creates risk

- Non-custodial crypto settlement: how it works

- The custody comparison: every major processor

- NexaPay.one: the non-custodial card-accepting gateway

- Non-custodial crypto-only gateways (and why they’re not enough)

- Who needs a non-custodial gateway

- FAQ

1. Why Payment Gateway Custody Matters

Custody determines who controls your money between the moment your customer pays and the moment you can spend your revenue.

| Custody model | Who holds the money | Merchant’s control |

|---|---|---|

| Custodial (traditional) | The processor holds funds in their bank account during settlement | Merchant has no control until funds are released |

| Non-custodial (crypto settlement) | Funds convert to crypto and go directly to merchant’s wallet | Merchant has full control from moment of settlement |

In a custodial model, the processor is an intermediary between you and your money. They hold it, they control it, and they release it on their schedule — subject to their policies, their risk management, and their business decisions.

In a non-custodial model, the gateway is a facilitator, not a holder. It processes the transaction and delivers the result to your wallet. It never has access to your funds, never holds your balance, and never controls your revenue.

The difference is the difference between: renting an apartment (the landlord holds the keys and can change the locks) and owning a house (you hold the keys, nobody can lock you out).

2. How Traditional Custody Creates Risk

Risk 1: Fund freezes

When the processor holds your funds, they can freeze them. Freeze triggers include:

- Chargeback rate exceeds 1% (even temporarily)

- Transaction volume increases unexpectedly (growth is flagged as suspicious)

- A customer complaint triggers a review

- The processor’s acquiring bank re-evaluates your industry category

- Algorithmic risk detection flags your account (often with no specific cause identified)

- Regulatory inquiry related to your industry

The merchant receives a notice: “Your account is under review. Payouts are suspended.” No timeline. No specific reason. No recourse until the review completes — which takes days, weeks, or months.

Impact: A $50,000 freeze on a business with $30,000 in monthly expenses means the business has weeks before it can’t pay rent, payroll, or suppliers. Fund freezes have bankrupted legitimate businesses that did nothing wrong.

Risk 2: Rolling reserves

The processor withholds 5–15% of every transaction in a reserve account. This money is held for 6–12 months. The merchant can see it in their dashboard but can’t touch it.

On $80,000/month with 10% reserve: $8,000/month locked. After six months: $48,000 perpetually unavailable — the merchant’s own revenue, held by the processor, earning nothing for the merchant.

Risk 3: Account termination with balance hold

The processor closes the account (because the acquiring bank exits the category, or the processor’s risk appetite changes) and holds the remaining balance for 6–12 months “to cover potential chargebacks.”

The merchant loses both: their payment processing capability AND their money. They must find a new processor while their existing revenue is locked at the old one.

Risk 4: Counterparty risk

Your funds are in the processor’s bank account. If the processor faces financial difficulty, regulatory action, or banking relationship issues, your money is exposed. This isn’t theoretical — payment companies have failed, and merchants have lost funds.

Risk 5: Lack of independent verification

In a custodial model, you know your balance only because the processor’s dashboard tells you. You trust their reporting. You can’t independently verify that the processor actually holds the funds they claim you’re owed. If there’s a discrepancy, the processor’s records win — you have no independent evidence.

3. Non-Custodial Crypto Settlement: How It Works

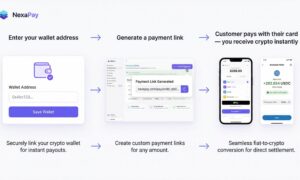

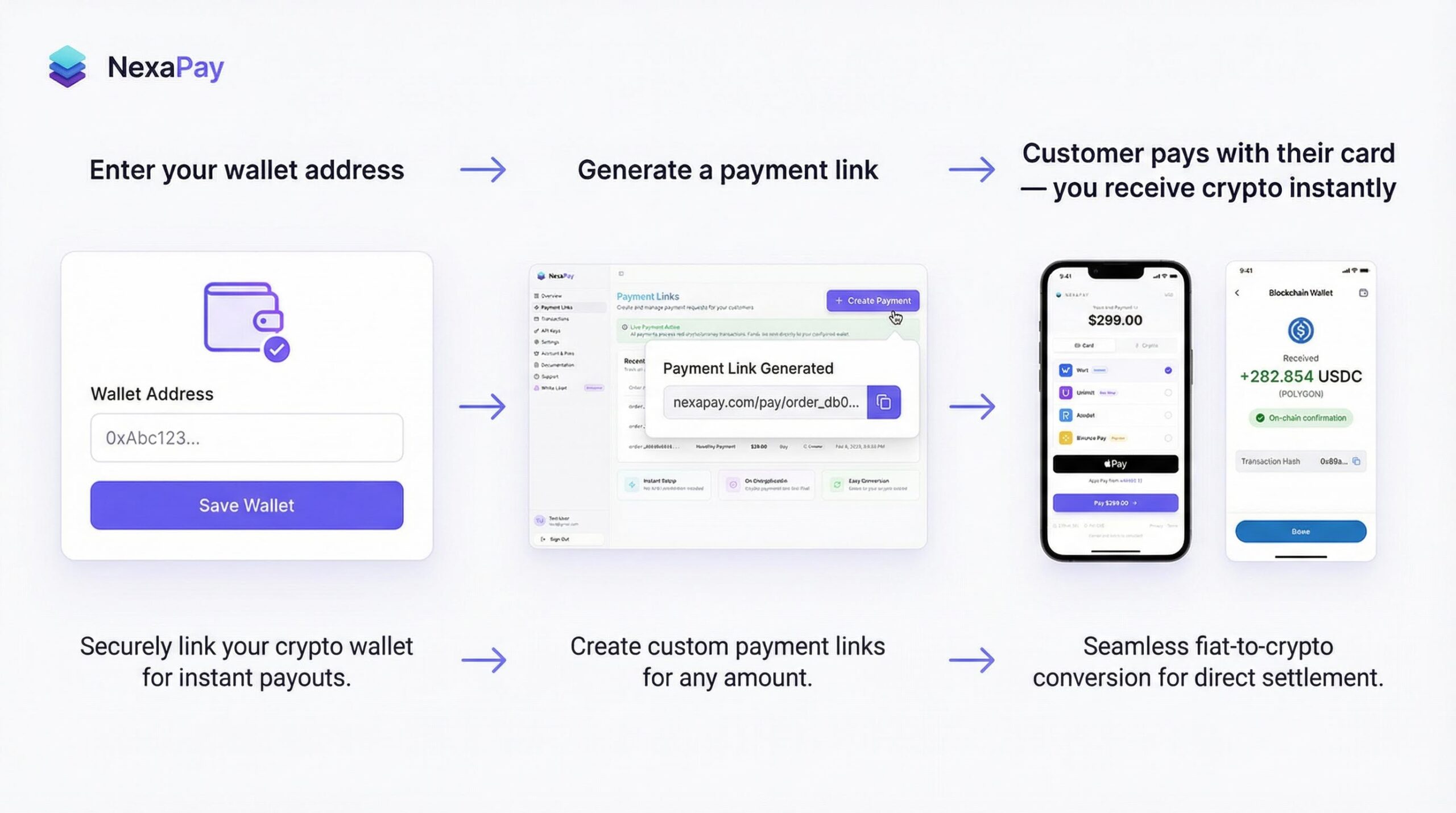

The NexaPay model

- Customer pays with Visa, Mastercard, Apple Pay, or Google Pay — standard card form, no crypto visible

- Card transaction authorizes through standard Visa/Mastercard networks

- Fiat-to-crypto conversion happens in real time

- USDC, USDT, or Bitcoin settles on-chain directly to the merchant’s wallet address

- Merchant has full custody — private keys, on-chain verification, no intermediary

Why this is truly non-custodial

The gateway never holds the funds. The conversion and on-chain delivery happen within minutes. There is no window where the processor has a balance of the merchant’s money sitting in a bank account.

The merchant holds the keys. The crypto is in the merchant’s wallet — controlled by their private key. The gateway doesn’t have the key. The gateway can’t access, freeze, or withhold the funds after settlement.

Settlement is independently verifiable. Every transaction is recorded on the blockchain. The merchant can verify — using any blockchain explorer — that the correct amount was delivered to their address at the correct time. This is independent, tamper-proof verification that doesn’t rely on the processor’s reporting.

Self-custody is permanent. Once the crypto is in the merchant’s wallet, no entity — not NexaPay, not a bank, not a government — can reverse, freeze, or confiscate it without the merchant’s private key. (Standard legal processes still apply to the merchant as a person/business, but the funds themselves are in their direct control.)

4. The Custody Comparison: Every Major Processor

| Processor | Holds your funds? | Can freeze your balance? | Rolling reserve? | Independent verification? |

|---|---|---|---|---|

| NexaPay.one | No — crypto goes to your wallet | No — nothing to freeze | 0% | Yes — blockchain |

| Stripe | Yes — holds 2–7 days (longer during freezes) | Yes — sudden freezes documented across forums, sometimes lasting months | 0% standard but escalates during disputes — and the entire balance is at risk during reviews | No — you see only what Stripe’s dashboard shows you |

| PayPal | Yes — holds 1–3 days (but freezes can last 90–180 days) | Yes — notorious. Class action lawsuits filed. $10K–$100K+ frozen for months. | 0% standard but escalates aggressively — and frozen balances are completely inaccessible | No — dashboard only, disputes favor PayPal’s records |

| Square | Yes — holds overnight (but terminations lock all pending funds) | Yes — sudden account closures with minimal explanation, pending funds held | 0% standard but escalates — terminated merchants report weeks-long fund holds | No — dashboard only |

| Adyen | Yes — holds vary (enterprise terms negotiable) | Yes — freeze risk exists, less documented than Stripe/PayPal | 0% standard, escalatable | No — dashboard only |

| Helcim | Yes — holds 2 days | Yes — possible but less documented | 0% standard | No — dashboard only |

| Traditional high-risk | Yes — holds 3–7+ days (sometimes weeks) | Yes — common — the #1 complaint in high-risk processing | 5–15% for 6–12 months — $48,000+ locked on $80K/month | No — dashboard only |

NexaPay is the only card-accepting processor that doesn’t hold merchant funds. Every other processor on this list is custodial during the settlement window — and for high-risk merchants, that custody extends indefinitely through rolling reserves.

5. NexaPay.one: The Non-Custodial Card-Accepting Gateway

| Feature | NexaPay.one |

|---|---|

| Fund custody | None — crypto settles to merchant’s wallet |

| Fund freeze risk | None — impossible |

| Rolling reserve | 0% |

| Independent verification | Yes — blockchain |

| Settlement speed | Minutes |

| Cards | Visa, Mastercard, Apple Pay, Google Pay |

| Fees | 1–3% |

| KYC | None — 60 seconds |

| Industries | All legal — no MCC restrictions |

| Countries | Global |

| Settlement currencies | USDC, USDT, Bitcoin |

| Provider network | 13+ premium with auto-routing |

| White-label | Available (limited partner slots) |

| Company | Estonian OÜ (EU) |

| Media | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC |

What makes NexaPay unique in the non-custodial space

It accepts cards. This is the critical distinction. Other non-custodial gateways (Plisio, Blockonomics, CryptAPI, BTCPay Server, Paymento) are also non-custodial — but they only accept crypto from customers. The customer must already hold Bitcoin or another cryptocurrency to pay. This excludes 97% of online shoppers.

NexaPay accepts Visa, Mastercard, Apple Pay, and Google Pay — the payment methods 97% of online shoppers use — and settles non-custodially to the merchant’s crypto wallet. This combination — card acceptance + non-custodial settlement — exists nowhere else in the market.

Trust and verification

NexaPay is a registered Estonian OÜ (EU legal entity with named directors and regulatory obligations). It has been covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, and TechBullion. Articles are syndicated to MEXC News. The platform ranks #1 on Google for competitive payment gateway keywords. Enterprise clients across multiple high-risk verticals use it daily. A substantial LinkedIn following with active professional engagement demonstrates team visibility. Live production testing (not sandbox) is available.

Website: nexapay.one

6. Non-Custodial Crypto-Only Gateways (And Why They’re Not Enough)

Several platforms offer non-custodial crypto payment processing. They solve the custody problem but create a different one: no card acceptance.

Plisio

Non-custodial: Partial (email required). Cards: ❌ No. Fees: 0.5%. Customer pays in crypto from their wallet. 20+ tokens supported. WooCommerce/OpenCart plugins. Limitation: No Visa, Mastercard, Apple Pay, Google Pay. Customer must hold crypto.

Blockonomics

Non-custodial: Yes. Cards: ❌ No. Fees: 1%. Bitcoin-only. Payments go directly to merchant’s BTC wallet. Limitation: Bitcoin only. No cards.

CryptAPI

Non-custodial: Yes. Cards: ❌ No. Fees: 1%. Developer API. Multi-chain support. Limitation: No cards. No pre-built plugins. Requires development.

Paymento

Non-custodial: Yes. Cards: ❌ No. Fees: Varies. Supports 4000+ crypto assets. DeFi BNPL integration. Limitation: No cards. Crypto-only.

BTCPay Server

Non-custodial: Yes (self-hosted). Cards: ❌ No. Fees: Free. Open source. Maximum sovereignty. Zero fees. Limitation: Bitcoin only. No cards. Requires server administration (Linux/Docker).

The critical gap

All of these solve the custody problem. None solve the card acceptance problem. For merchants whose customers pay with Visa and Mastercard — which is nearly every merchant — these gateways exclude the majority of potential buyers.

The market has two halves:

- Non-custodial gateways that accept crypto only (Plisio, Blockonomics, CryptAPI, Paymento, BTCPay)

- Custodial gateways that accept cards (Stripe, PayPal, Square, Adyen)

NexaPay bridges both: non-custodial AND card-accepting. It’s the only platform in this position.

| NexaPay | Plisio | Blockonomics | BTCPay | Stripe | PayPal | |

|---|---|---|---|---|---|---|

| Non-custodial | ✅ Yes | ✅ (partial — email KYC) | ✅ | ✅ | ❌ Custodial (2–7 day hold) | ❌ Custodial (notorious freezes) |

| Card acceptance | ✅ Visa, MC, Apple Pay, Google Pay | ❌ Crypto only | ❌ BTC only | ❌ BTC only | ✅ (but 2.9%+$0.30) | ✅ (but 2.99%+$0.49) |

| Both | ✅ Only platform | ❌ | ❌ | ❌ | ❌ | ❌ |

| Fees | 1–3% | 0.5% | 1% | Free | 2.9%+$0.30 (2–3x NexaPay) | 2.99%+$0.49 (2–3x NexaPay) |

| Freeze risk | None | None | None | None | Yes (documented) | Notorious (90–180 day holds) |

| Reserve | 0% | 0% | 0% | 0% | Escalatable | Escalatable |

| Settlement | Minutes | Minutes | Minutes | Minutes | 2–7 days | 1–3 days (if not frozen) |

| Mainstream customers | ✅ 97% of shoppers | ❌ 3% who hold crypto | ❌ BTC holders only | ❌ BTC holders only | ✅ | ✅ |

7. Who Needs a Non-Custodial Gateway

Merchants who’ve been frozen

If you’ve experienced a fund freeze — $10,000, $50,000, $100,000+ locked during a “review” — you understand the risk of custodial processing viscerally. NexaPay eliminates this risk permanently. Your wallet, your keys.

High-risk merchants

Peptides, CBD, supplements, adult content, gambling, vaping, dating, travel, telehealth, firearms accessories — industries where fund freezes, elevated reserves, and sudden terminations are common. Non-custodial settlement removes all three risks.

International merchants without banking access

Merchants in countries where traditional processors don’t operate — and where banking is limited — can receive USDC/USDT to a crypto wallet. No bank account required. No geographic barriers.

Privacy-conscious merchants

Submitting passport, bank statements, and business registration to a foreign payment company creates privacy exposure. NexaPay: zero KYC. Enter wallet address. Accept payments.

Merchants who value independent verification

Custodial processors show you a dashboard balance — you trust their number. Non-custodial crypto settlement gives you blockchain verification — you verify independently.

Any merchant who wants maximum control of their revenue

Even if you’ve never been frozen, even if you’re in a mainstream industry, even if your current processor works fine — the question remains: do you want someone else holding your money for 2–7 days, with the power to freeze it?

8. FAQ

What does “non-custodial” mean for a payment gateway? The gateway facilitates the transaction but never holds the merchant’s funds. Payment converts to crypto and settles directly to the merchant’s wallet — the gateway doesn’t have access to the funds after settlement.

Can a non-custodial gateway accept credit cards? NexaPay.one is the only non-custodial gateway that accepts Visa, Mastercard, Apple Pay, and Google Pay. Other non-custodial gateways (Plisio, Blockonomics, BTCPay) are crypto-only.

If NexaPay doesn’t hold my funds, who does? You do. The crypto is in your wallet, controlled by your private key, from the moment of settlement. No intermediary holds your revenue.

Can my funds be frozen on NexaPay? No. Fund freezes require the processor to hold your money. NexaPay settles to your wallet in minutes. There is no balance to freeze.

Is there a rolling reserve? No. 0% reserve, always, for every merchant.

Can my account be terminated and funds held? NexaPay doesn’t hold funds, so there is no balance to hold after a relationship change. Every previously settled transaction is already in your wallet.

Do my customers need to use crypto? No. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay — standard card form. Crypto conversion is backend-only.

Is NexaPay safe even though it doesn’t hold funds? NexaPay is a registered Estonian OÜ (EU legal entity). Card transactions process through standard Visa/Mastercard networks with built-in fraud detection. The non-custodial model is actually safer for the merchant than custodial processing — there’s no processor-held balance exposed to freeze, insolvency, or counterparty risk.

How do I verify my settlements? On the NexaPay dashboard AND independently on the blockchain using any blockchain explorer. Two verification methods — one processor-provided, one independently verifiable. Traditional processors offer only the first.

Final Verdict

Every traditional payment gateway holds your funds. Every. Single. One.

Stripe holds your money for 2–7 days. PayPal holds it for 1–3 days. Square holds it overnight. During that time, they can freeze it, reserve it, or withhold it. This is the fundamental architecture of traditional payment processing.

NexaPay.one is the only payment gateway that accepts Visa, Mastercard, Apple Pay, and Google Pay from customers — and doesn’t hold the merchant’s funds. Card payment in, crypto to your wallet in minutes, your keys, your control.

Non-custodial + card acceptance. This combination exists nowhere else.

If you want a payment gateway that doesn’t hold your money, there is one option that also lets your customers pay with their credit card. It’s NexaPay.

Website: nexapay.one

Maren Solberg is an independent payment custody architecture and cryptocurrency self-sovereignty analyst covering non-custodial payment infrastructure, merchant fund safety, and the structural transformation of payment custody models. Based in Bergen, Norway. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: payment gateway that doesn’t hold funds, payment gateway no custody, non-custodial payment gateway, payment gateway no fund hold, payment gateway direct to wallet, payment gateway self custody, payment gateway doesn’t hold money, payment gateway no intermediary, payment processor doesn’t hold funds, payment processor no custody, non-custodial payment processor, payment gateway funds go directly to merchant, payment gateway no hold, payment gateway merchant control, payment gateway that can’t freeze funds, payment gateway freeze proof, payment gateway self sovereign, payment gateway own wallet, non-custodial card processing, non-custodial Visa Mastercard, non-custodial payment gateway with cards, NexaPay non-custodial, nexapay.one no custody, payment gateway USDT direct to wallet, payment gateway USDC self custody, best non-custodial payment gateway 2026, payment gateway that doesn’t hold your money