Taking a Personal Loan today looks nothing like it did five years ago. The paperwork is lighter, approvals come faster, and the competition between lenders has never been fiercer. But faster doesn’t always mean better.

A trader in Jaipur dealing with a supply gap, or a salaried professional in Bengaluru facing an unexpected hospital bill, both need money quickly. Both will likely receive offers within minutes from half a dozen apps. The harder question is which offer actually works in their favor over the next two or three years.

Speed Has Become the Selling Point. Scrutiny Should Be.

The Account Aggregator framework changed how lenders read borrower profiles. A complete financial picture is now available in seconds, which is why “instant” offers flood every notification bar. What most borrowers don’t immediately notice is that many platforms compensate for their speed with high processing fees or prepayment penalties buried deep in the agreement.

Established financial institutions have kept pace technically. Their backend systems are fast enough now that the approval gap between a traditional lender and a fintech app has practically closed. The real difference shows up later, in fee transparency, in customer support, and in how disputes get handled.

What the Rate Landscape Actually Looks Like in 2026

The personal loan interest rate a borrower receives is rarely the same rate advertised. Risk-based pricing means the number depends on the individual’s credit profile, income stability, and existing debt load.

| Type of Lender | Interest Rate (p.a.) | Processing Fees | Best For |

| Public Sector Banks | 10.30% – 12.25% | 0.5% – 1% | Govt. Employees / Pensioners |

| Private Sector Banks | 10.75% – 16.00% | 1% – 2.5% | Salaried Professionals |

| NBFCs | 11.00% – 20.00% | Varies | Self-employed / Non-salaried |

| Fintech / Instant Apps | 14.00% – 28.00% | Up to 5% | Small, Urgent Disbursals |

The gap between the cheapest and most expensive options here runs into lakhs of rupees across a five-year tenure. That’s not a rounding error, it’s a decision worth spending time on.

The CIBIL Score: More Relevant Than Ever

The CIBIL Score hasn’t lost its importance; it carries more weight now than it did even two years ago. Banks and NBFCs cross-reference credit data with utility payment records, BNPL histories, and sometimes rental behavior. That three-digit number has quietly become a fuller picture of someone’s financial life.

Sit at 750 or above and lenders compete for the business. Drop below 650 and the options shrink, or arrive with rates that make borrowing genuinely painful. A late payment on a small BNPL purchase can move this number more than most people expect.

Monthly monitoring isn’t overcaution anymore. It’s basic financial hygiene.

Why the Lender Choice Matters as Much as the Rate

Muthoot Finance has been around long enough to have seen multiple credit cycles. Their branch network spans the country, which matters to borrowers who want a physical point of contact, not just a chat window. For customers who already hold an account with them, the process is noticeably smoother. Pre-approved offers with reduced or waived processing fees are a common benefit for existing account holders.

What sets them apart in the current market isn’t speed alone, it’s the absence of unpleasant surprises. No hidden charges surfacing twelve months in. No ambiguous clauses that only become clear at foreclosure. That kind of consistency is harder to find than it sounds.

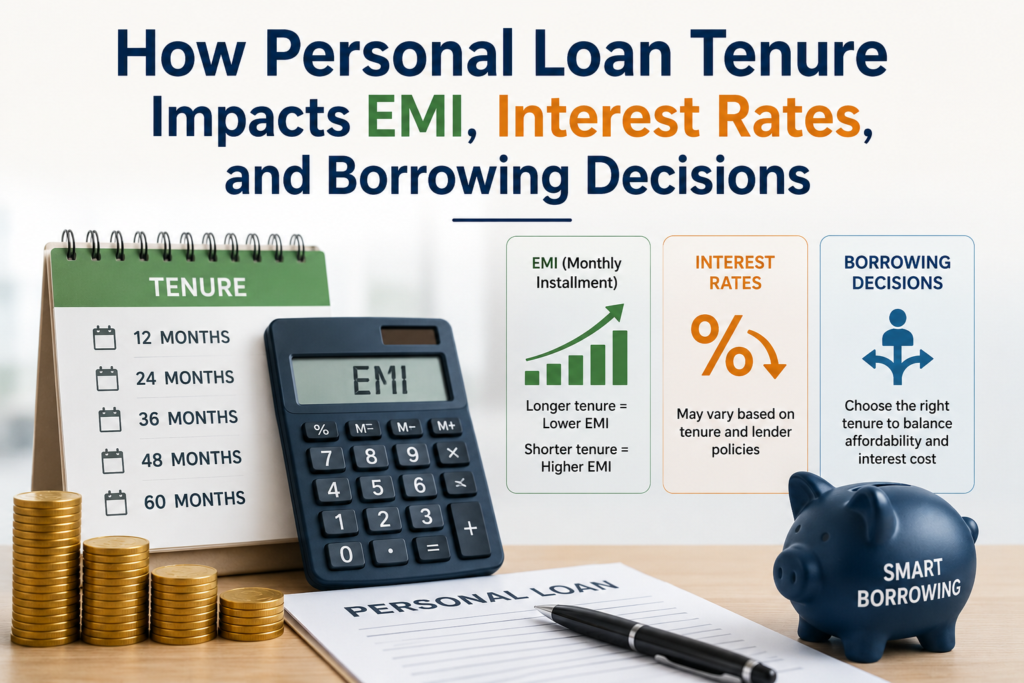

The Tenure Math Most Borrowers Skip

This is where loan decisions quietly go wrong. A personal loan EMI calculator takes three minutes to use and can save tens of thousands in unnecessary interest payments.

Take a ₹5 lakh loan at 13% per annum. At a three-year tenure, the monthly EMI is higher but total interest paid stays controlled. Stretch it to five years, the monthly outgoing drops, but total interest climbs considerably. Neither tenure is universally right. It comes down to actual monthly cash flow, not the more comfortable-looking number on screen.

Practical Pointers Worth Keeping

- Check pre-payment terms first. A salary hike or business windfall should allow early debt closure, not trigger penalty clauses.

- Pre-approved offers go unused far too often. Borrowers with existing banking relationships routinely miss out on better terms by applying fresh elsewhere.

- Borrow what’s needed, not what’s available. A ₹20 lakh sanction doesn’t require a ₹20 lakh withdrawal.

- Repeated applications damage the CIBIL Score. One well-researched application is perfectly fine. Five within a week raises flags with every lender reviewing the profile.

Two Things People Keep Getting Wrong

First, the belief that any loan application will significantly hurt the CIBIL Score. A single hard inquiry causes a minor, short-lived dip. The real damage comes from applications stacked across multiple lenders within weeks of each other.

Second, the assumption that an instant personal loan can only come from a fintech app. Traditional institutions have rebuilt their processing infrastructure substantially. Approval timelines are now comparable, sometimes faster, and the support structure that follows is far more reliable when something goes wrong.

Final Word

The fundamentals haven’t shifted much. Borrow what’s actually needed, from a lender with a clear track record, after running the tenure numbers properly. What has changed is how easy it is to get this wrong quickly in 2026, and equally, how straightforward it is to get it right with a little preparation.