Open the payments documentation of any new U.S. e-commerce store launched in May 2026, and the integration choice list runs a page long. Stripe is the default for most online-first merchants. Adyen is the default for enterprise. Block’s Square owns the small-business POS layer. PayPal is at every checkout. Braintree, Worldpay, Global Payments, and FIS occupy specialised niches. Newer entrants like Checkout.com and Rapyd have carved out international and orchestration roles. The U.S. payment service provider stack in 2026 is not just crowded, it is layered, with PSPs that compete in the public mind frequently sitting on top of each other in production architectures. Understanding how the stack got this shape, and where the actual margin sits inside it, is the most useful exercise for any founder trying to decide who to integrate with, and the picture has changed enough since 2020 that older mental models are now misleading rather than helpful.

What a PSP actually is in 2026

The term payment service provider is loose enough that it now covers several distinct roles. The classical PSP is a gateway: a service that sits between a merchant’s checkout and the card networks, handling tokenisation, 3D Secure authentication, fraud screening, and the call into the acquirer. The acquirer is then the bank-side entity that submits the transaction to Visa or Mastercard for authorisation and clearing. In 2010, those were almost always two different companies, and most PSPs were pure gateways with no acquiring relationship of their own. The line between gateway and acquirer was meaningful to industry insiders and invisible to merchants.

By 2026 the lines have collapsed. Stripe, Adyen, Block, and PayPal have all built or acquired direct acquiring relationships, often through bank partnerships or by becoming acquirers in their own right in specific geographies. The integration the merchant sees is a single API, with the PSP doing the gateway work, the acquirer call, the settlement to the merchant’s bank, and frequently the merchant’s underwriting and risk too. The unbundled gateway-only model still exists but is shrinking. The integrated model is what most new merchants choose because it is meaningfully simpler, and the operational benefits of a single contract and a single integration outweigh the marginal cost savings of a custom gateway-acquirer combination for almost every merchant under enterprise scale.

The volume and where it sits

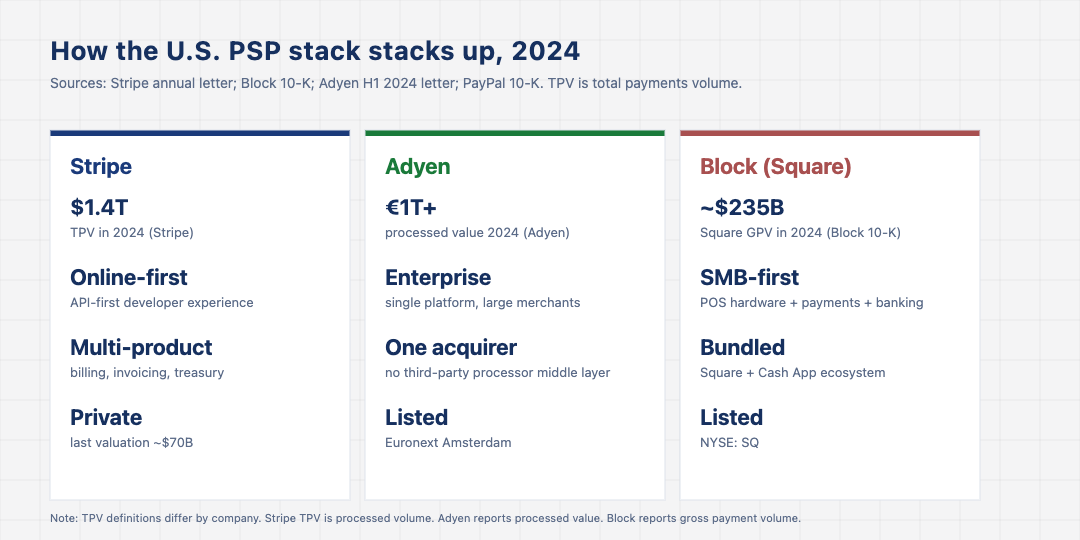

The headline numbers across the U.S. PSPs in 2024 illustrate how much volume is concentrated at the top. Stripe processed about $1.4 trillion in total payments volume in 2024 according to its annual letter. Adyen reported over €1 trillion in processed value. Block’s Square reported about $228 billion in Square gross payment volume in its 2024 10-K. PayPal, with its various branded checkout, Venmo, and Braintree businesses, pushes well above $1.5 trillion in total payment volume across all flows. The numbers are not directly comparable because the definitions differ, but the shape is consistent: four companies process the bulk of U.S. card-not-present and a meaningful chunk of card-present volume, with the remainder split across a long tail of smaller and more specialised providers.

Beneath the top tier sits a long tail of legacy processors and bank-affiliated acquirers including FIS, Global Payments, Worldpay, Fiserv, Elavon, and Bank of America Merchant Services. Together this layer still processes a substantial share of U.S. brick-and-mortar volume, particularly in industries that have historically been underserved by the online-first PSPs: gas stations, hospitality groups, healthcare networks, and large grocery chains. The legacy processors are not going away. They are being squeezed in pricing and in product velocity, but they remain entrenched in the merchant relationships they originally built. The TechBullion piece on payments systems and infrastructure covers the broader rails this all sits on.

Why the stack ended up layered

The layered architecture is the surprising thing about the 2026 U.S. PSP picture. A merchant might use Stripe at the front for the API ergonomics, sit Stripe on top of an internal payment orchestrator like Spreedly or Primer for vendor-neutral routing, and have the orchestrator route to multiple acquirers underneath for cost and authorisation-rate optimisation. The orchestrator layer barely existed in 2018; by 2024 it was a meaningful category, with Spreedly, Primer, Gr4vy, and the in-house orchestration teams at very large merchants all carving up the new middle.

The driver is authorisation rate. Each acquirer routes its volume slightly differently, and the difference between a merchant’s best and worst acquirer can be one to three percentage points of approval rate, which on hundreds of millions of dollars in monthly volume is meaningful enough to justify the operational complexity of running multi-acquirer routing. Orchestration platforms exist to capture that lift without the merchant building the routing themselves. The competitive question for the top-tier PSPs is whether they absorb the orchestration role into their own platforms, which Stripe and Adyen are visibly trying to do, or whether the orchestration layer becomes a permanent independent middle. Both outcomes look possible from where the market sits in 2026.

Where the actual margin lives

The economics of U.S. payment service provision are heavily concentrated in a small number of components of the transaction. Interchange, the fee paid to the issuer, is by far the largest component, typically 1.5 to 2.5 percent on a U.S. credit card transaction. The card network fees are smaller, in the range of 13 to 15 basis points. The acquiring fee, where the PSP makes its money, is the residual, and it varies from a few basis points for very large merchants on Adyen-style enterprise pricing to several percentage points for small merchants on Stripe or Square SMB pricing. The headline rate the merchant pays, often quoted as 2.9 percent plus 30 cents in U.S. blended pricing, is the sum of all these components.

The PSPs make most of their money on small and mid-sized merchants on blended pricing, and very little on the largest enterprise accounts on interchange-plus. The cross-subsidy is well understood inside the industry and is one reason the SMB-focused Block continues to invest heavily in a category that looks lower-margin from the outside. The lifetime value of a small merchant who pays blended pricing for several years is meaningfully higher per dollar of volume than the comparable enterprise relationship, even before adjacent revenue from lending, banking, and software bundling is counted. The TechBullion piece on why banking infrastructure is becoming digital covers the broader vendor pattern this fits into.

What founders building merchant-facing products should know

For founders building any merchant-facing product in 2026, three practical points come from this picture. First, integrate with one PSP fully and add additional PSPs only when the data shows the lift is real. Multi-PSP integration is not free; the engineering and reconciliation cost is meaningful. Second, the orchestration layer is now a viable choice for any merchant doing more than $50 million a year in volume. Below that, single-PSP is almost always right. Third, the bundled offerings of the top-tier PSPs, billing, invoicing, treasury, and fraud, are increasingly the differentiator. Pick the PSP whose bundle most closely matches the products the founder is going to need across the next two years, not just the cheapest per-transaction rate. The TechBullion piece on why banking innovation is accelerating worldwide provides broader global context for these architectural decisions.

The U.S. PSP stack in 2026 is the result of fifteen years of convergence: gateway and acquirer collapsed into integrated platforms, online-first and brick-and-mortar starting to share infrastructure, and a new orchestration middle layer emerging on top of it all. The category is mature enough that the integration question is no longer about which PSP works, all of them do, but about which bundle and which routing approach matches the merchant’s actual operating economics. The volume continues to compound, the rate compression continues to bite, and the next phase of competition will be fought on the adjacent products that the underlying transaction makes possible.