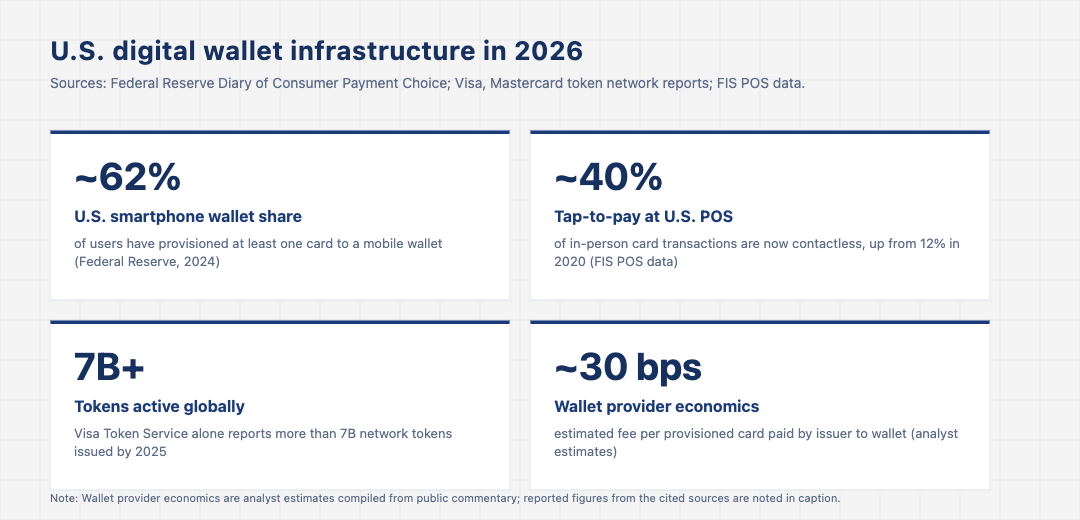

Walk into a cafe in midtown Manhattan in May 2026, watch the line for ten minutes, and you will see roughly two out of every five customers pay by tapping a phone or watch against the terminal. The number was roughly one in eight at the same cafe in 2020. The acceleration is the visible part of a quieter, deeper rebuild of U.S. digital wallet infrastructure: a tokenisation network that did not exist a decade ago, secure-element hardware in every recent phone, and a set of issuer-wallet economic agreements that turned a curiosity into the default U.S. payment experience for an entire generation. According to the Federal Reserve’s most recent Diary of Consumer Payment Choice, more than half of U.S. smartphone users have provisioned at least one card to a mobile wallet, and the contactless share of in-person card transactions has climbed past 40 percent, up from roughly 12 percent in 2020.

The hardware and the protocol underneath

Every digital wallet transaction in the U.S. depends on a handful of layered technologies that the average consumer never sees. At the bottom is the contactless interface itself, a near-field communication chip operating at 13.56 MHz that uses the EMV contactless protocol, the same protocol that runs on physical chip cards. Above that is the wallet application, which holds a representation of the consumer’s card. Critically, what sits in the wallet is not the actual card number, called the primary account number or PAN. It is a network token, a different number issued by Visa Token Service, Mastercard Digital Enablement Service, or American Express Token Service, that maps back to the underlying PAN only inside the network’s secure environment.

The token approach matters because it confines the actual card number to a small set of high-trust systems. If the consumer’s phone is compromised, the attacker gets a token tied to that specific device, not the card number. The token can be revoked instantly without disturbing the underlying card, which means the consumer does not need a new physical card mailed and the recurring billers connected to the underlying card are not interrupted. This is the architectural difference that made the broad U.S. wallet rollout possible: issuers, network providers, and merchants could agree to accept the model because the data exposure was bounded by design and the operational cost of breach response was meaningfully lower than for a PAN exposed at the merchant.

The wallet provider economics that took ten years to settle

The slowest part of the rollout was not technology, it was economics. Apple Pay launched in October 2014. Google Pay, originally Android Pay, followed in 2015. Both required issuer agreement, and the first round of those agreements involved a fee from the issuer to the wallet provider in the range of 15 basis points per transaction. The fee was a meaningful negotiation. Issuers initially resisted; over several years they came around as it became clear that the wallet experience was driving both higher card-on-file persistence and lower fraud loss. The current consensus, drawn from analyst commentary across S&P Global and Federal Reserve workshops, puts the average wallet provider fee in the U.S. at roughly 15 basis points per provisioned card on credit transactions, with a fraction of a cent on debit paid by the issuer, though the precise figures remain confidential and vary by issuer.

The wallet economics are now stable enough that almost every U.S. consumer card is wallet-eligible at issuance. The exception is a long tail of smaller credit unions and store-card issuers that have either not yet built integrations or have made the economic decision that the fee is not worth the volume. As of 2026 that long tail is shrinking, helped by core-banking vendors offering wallet provisioning as a packaged feature.

The acceptance side: what changed at the terminal

Tap-to-pay growth at the U.S. point of sale was held back for years by the merchant side rather than the consumer side. Until 2018 to 2020, contactless-enabled terminals were a minority of installed terminals in the U.S., trailing well behind the U.K. and Australia. The pandemic changed the priority list. Touch-free became a feature merchants advertised. By 2022 the share of contactless-enabled U.S. terminals had crossed 70 percent. By the end of 2025, FIS POS data indicated that more than 90 percent of installed terminals supported contactless. The consumer behaviour caught up: as soon as more than half of terminals worked, the share of consumers willing to default to wallet payment crossed a tipping point.

The merchant economics did not actually change very much. The interchange fee on a tap-to-pay credit card transaction is broadly the same as the chip-and-PIN equivalent, and the small surcharges for tap-to-debit have been negotiated down. What changed was the throughput. A tap-to-pay queue moves measurably faster than a chip-and-PIN queue, and at high-volume merchants the labour and customer-satisfaction implications of that compound. Quick-service restaurants and stadium concessions have been the most public adopters; their queue-time data has been the easiest to point at when arguing for the upgrade. For broader context, the TechBullion piece on payments systems and infrastructure situates this within the wider U.S. payments stack.

What product teams should design for now

For founders building consumer-facing fintech in 2026, the wallet layer is no longer optional. It is the assumed entry point for any new card product. Issuing a card without a one-tap provisioning flow into Apple Wallet, Google Wallet, and Samsung Wallet is now a competitive disadvantage in the consumer segment. The consumer experience expectation, set by neobanks like Chime and Cash App over the last five years, is that a virtual card is available before the physical one is mailed and is wallet-provisioned automatically. The TechBullion piece on why banking infrastructure is becoming digital sets out how this expectation has spread across the broader stack.

The architectural question for new entrants is whether to build the wallet provisioning integration in-house or use a card-issuing platform that handles it. Marqeta, Lithic, and Highnote all offer turn-key wallet provisioning today, and the build-versus-buy decision for most teams is now buy. The economics work because the platforms have done the certification and ongoing maintenance work that an individual fintech would otherwise duplicate, and the network certifications have a refresh cadence that is not trivial to manage in a team of fewer than ten payments engineers.

The next frontier: wallet-as-account, not wallet-as-payment

The shape of the next wave of digital wallet infrastructure in the U.S. is starting to look less like a payment instrument and more like an account-with-payment-attached. Apple Cash, Google Pay’s send-money flow, and the wallet integrations of PayPal and Cash App all let consumers hold balance inside the wallet itself. The implications for issuers are significant: every dollar that lives inside a wallet rather than a deposit account is a dollar that does not earn deposit revenue for the issuer. The medium-term competitive question is whether the wallet providers move further into deposit-equivalent product or whether the issuers find a way to make their balance-bearing relationship more attractive than the wallet’s. The TechBullion piece on why banking innovation is accelerating worldwide sets out the global pattern that informs this question.

Digital wallet infrastructure in the U.S. has gone from frontier to default in a decade, and the underlying technology, network tokens, secure elements, contactless EMV, has become invisible the way good infrastructure does. The interesting fights are no longer about whether wallets work. They are about who captures the relationship the wallet now mediates, who owns the balance that increasingly sits inside it, and who keeps the data trail that follows the consumer across every payment they make. That fight is actively underway across every major issuer in the country, and it will define the shape of U.S. consumer banking through the rest of the decade.