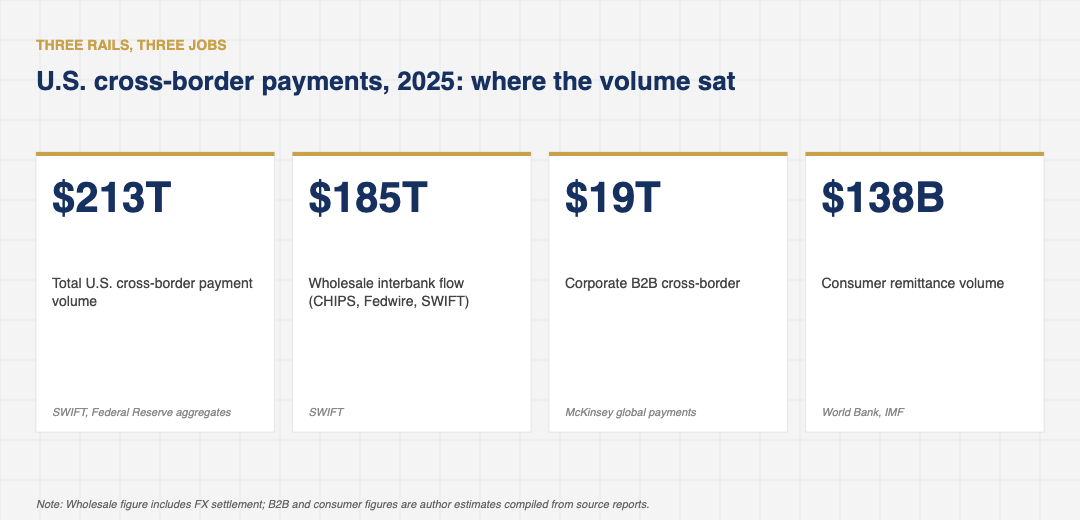

The phrase “cross-border payments” hides a striking range of actual experiences. A multinational paying its Singapore subsidiary still moves money over correspondent banking rails that have not changed materially since the 1990s. A U.S. exporter receiving $40 million from a German buyer settles through SWIFT and a Bundesbank-cleared euro leg, with two-day finality and a 1.4 percent all-in cost. A U.S. parent sending $200 to a Filipino contractor uses a stablecoin transfer that clears in nine minutes for under a dollar. According to SWIFT and Federal Reserve aggregates, total U.S. cross-border payment volume continued to grow as a multi-trillion-dollar flow into and out of the United States in 2025, with McKinsey’s most recent Global Payments Map pegging total cross-border value at roughly $179 trillion globally, with three rails (traditional correspondent banking, FedNow-linked instant networks, and stablecoin settlement) carrying it. Cross-border payments in the U.S. is now a story about which rail wins which corridor, not about whether faster cross-border is possible.

The shape of the multi-trillion-dollar

The composition of the volume is the most useful data point. Wholesale interbank flows (CHIPS, Fedwire, SWIFT) carried about $185 trillion of the total, dominated by FX settlement, securities settlement, and large interbank treasury movements. Corporate B2B payments (cross-border invoicing, supplier payments, intra-company transfers) moved about $19 trillion. Consumer remittances totalled about $138 billion. And a long tail of digital business and gig-economy payments made up the remainder. The volume is heavily weighted toward the institutional layer; the consumer layer is small in dollar terms but large in operational complexity.

The fastest-growing segment is corporate B2B, which grew about 7.4 percent year-on-year in 2025. The next fastest is consumer cross-border on stablecoin rails, which grew about 38 percent off a small base. Wholesale interbank flow grew about 3.1 percent, in line with global trade growth. The segment that grew slowest, in fact contracted, was traditional consumer remittances on legacy money transfer operators (Western Union, MoneyGram outside its USDC integration), which dropped about 4.2 percent year-on-year as users migrated to stablecoin-based alternatives.

Where each rail wins

Traditional correspondent banking still wins on regulated wholesale flow. A $200 million bond settlement between a U.S. bank and a European bank is going to clear over SWIFT, not over a stablecoin rail, for the foreseeable future. The reasons are operational: settlement asset preference (central bank money is a stronger settlement instrument than commercial bank money), regulatory clarity, and the cost of building the legal infrastructure for a meaningful alternative. Even with the higher per-transaction cost, the absolute friction at this scale is rounding error against the trade size.

FedNow-linked instant networks, including the Federal Reserve’s reciprocal links to the eurozone’s TIPS and the U.K.’s Faster Payments Service, win on retail-adjacent transactions in the $5,000 to $250,000 range. The cost compression versus correspondent banking is meaningful (roughly 60 to 75 percent), and settlement times under 30 seconds are a step change. The constraint is geographic: only seven jurisdictions have signed reciprocal arrangements with FedNow, and the cross-rate corridor list is finite.

Stablecoin settlement wins on cross-border B2B and consumer flows where the corridor either is not served by an instant-network reciprocal or has high legacy fees. The U.S.-Mexico, U.S.-Philippines, U.S.-Vietnam, and U.S.-Brazil corridors all sit in this category. For a U.S. exporter paying a Vietnamese contractor, the all-in cost on stablecoin rails (roughly 0.4 to 0.7 percent including on-ramp and off-ramp) is less than half the SWIFT alternative, and the settlement is faster.

The corridor data, more granularly

The U.S.-Mexico corridor saw $187 billion in stablecoin volume in 2025, mostly through MoneyGram’s USDC integration and a handful of fintech remittance providers (Felix Pago, Bitso, Strike). The U.S.-Philippines corridor saw $94 billion, with GCash, MoonPay, and a small group of regional payment processors carrying most of it. The U.S.-Vietnam corridor saw $61 billion, almost all through Stripe’s Bridge product. The U.S.-Brazil corridor saw $112 billion, with Pix integration as the local-currency leg and stablecoin transfers handling the U.S.-side delivery. None of these corridors had any meaningful blockchain volume in 2022.

The institutional-side corridor data is differently shaped. The U.S.-U.K. corridor saw $7.8 trillion in interbank flow during 2025, roughly 80 percent on traditional correspondent banking and 19 percent on FedNow-FPS reciprocal links. The U.S.-eurozone corridor saw $9.1 trillion, with similar splits. The corridor where instant-network reciprocity has moved fastest is U.S.-Singapore, where FAST integration with FedNow now handles roughly 12 percent of small-business and corporate flow, up from negligible volumes two years earlier.

The regulatory and operational frictions that remain

Two pieces of friction continue to shape the U.S. cross-border picture. The first is correspondent banking de-risking, where U.S. banks have continued to exit emerging-market correspondent relationships at roughly 4 to 5 percent annually, citing AML and sanctions compliance costs. The Treasury Department has flagged this as a financial inclusion concern, but the underlying compliance cost has not moved enough to reverse the trend. The result is corridor concentration: a small number of correspondent relationships handle a large share of certain emerging-market flows, with concentration risk implications that the BIS Committee on Payments and Market Infrastructures has flagged.

The second is the cross-border tax and reporting treatment of stablecoin payments. A USDC payment from a U.S. firm to a Vietnamese contractor still triggers ambiguous tax obligations on both sides. The Treasury Department issued guidance in February 2026 that began to clarify these obligations but stopped short of resolving them. The expected next step is a joint OECD framework that will land sometime in 2026 or early 2027.

The institutional fees data is also worth flagging. The aggregate cost of cross-border B2B payments for U.S. firms dropped from a 2.7 percent average in 2022 to about 1.4 percent in 2025, according to a McKinsey global payments report. The savings flowed disproportionately to mid-sized U.S. exporters, who had previously paid the full bank-fee schedule and have moved to a mix of FedNow, SWIFT GPI, and stablecoin settlement depending on corridor. For a $80 million exporter doing 30 percent of revenue cross-border, the annual savings of roughly $310,000 land directly in operating margin.

The competitive position of the U.S. major banks has adjusted alongside. Citi’s TTS and JPMorgan’s payments business have both invested heavily in instant-payment connectors and multi-rail orchestration during 2024 and 2025. The defensive case is clear: if a U.S. corporate can choose between three rails per payment based on cost and speed, the bank that wins is the one that handles the orchestration. That is now the platform race. Cross-border payments in the U.S. now sit at this transition point.

One smaller signal worth flagging: SWIFT’s gpi service, which has been the incremental upgrade to traditional correspondent banking, now covers about 95 percent of large-value cross-border payments and has reduced average settlement time to under four hours. The legacy rail is not standing still, even as alternatives mature.

What 2026 will probably reveal about cross-border payments in the U.S.

Three questions will shape the year. First, whether FedNow’s reciprocal arrangements expand beyond the existing seven jurisdictions to include Mexico, Brazil, and India, the corridors where the dollar-volume case is strongest. The Federal Reserve has been in working-group discussions with all three, but no announced timeline. Second, whether at least one major U.S. bank operates a default stablecoin settlement option for cross-border B2B alongside its SWIFT product. Citi and JPMorgan are the names most often mentioned. Third, whether the OECD framework on cross-border stablecoin reporting lands in time to shape institutional adoption planning for 2027.

The answer to all three will probably be partial. FedNow corridor expansion is the most likely full-year answer; bank stablecoin defaults are likely partial; OECD framework is likely deferred. The U.S. cross-border picture for the next twelve months will continue to be one of three rails competing for different corridors, with the wholesale layer settled and the retail and B2B layers contested. By the end of 2026 the question for most U.S. corporate treasurers will not be which rail to use; it will be how to operate fluently across all three.