How a Former VC-Backed Founder Discovered the Most Asymmetric Risk-Adjusted Opportunity in Bitcoin Mining

For years, we dismissed Bitcoin mining as a fundamentally flawed business. We viewed it through the lens of traditional venture capital: weak margins, commodity hardware, brutal cyclicality, and no defensible moat. In partner meetings, we described it as a race to the bottom, capital-intensive, operationally messy, and strategically hollow. We believed it was analogous to gold mining with faster depreciation and fewer barriers to entry.

That belief was wrong.

Not marginally wrong. Completely wrong.

What changed was not Bitcoin’s price, nor a sudden ideological conversion. What changed was our mental model. When we stopped analyzing mining like a SaaS company and began understanding it as energy arbitrage married to monetary infrastructure, the unit economics revealed themselves with startling clarity.

This article presents that reframed thesis, grounded in numbers, infrastructure realities, and first-hand operational experience.

Bitcoin Mining Is Not a Business on Top of Bitcoin; It Is Bitcoin

The critical insight is deceptively simple: Bitcoin mining does not merely produce Bitcoin; it produces the network itself.

Miners generate security, final settlement guarantees, and decentralization. These properties are what make Bitcoin valuable as a monetary system. The block reward is not “revenue” in a conventional sense—it is closer to equity issuance in a global, permissionless monetary network.

Once we internalize that miners are compensated for underwriting the integrity of the system, the economics stop looking speculative and start looking infrastructural.

Reframing Mining Using Institutional Business Metrics

Hashrate as Contracted Production Capacity

In venture, we obsess over recurring revenue. In mining, hashrate functions as predictable productive capacity. Deploying ASICs purchases a deterministic share of future block rewards, adjusted by network difficulty.

While short-term variance exists, medium-term cash flows are modelable, stress-testable, and remarkably transparent. Difficulty adjustments act as an automatic stabilizer, smoothing extreme outcomes over time.

Unlike SaaS, there is no customer churn. The “customer” is the Bitcoin protocol, and it does not defect.

Total Addressable Market: Securing the World’s Hardest Money

Bitcoin mining’s TAM is often misunderstood. It is not capped by hardware shipments or energy consumption. The true market is the total value secured by the Bitcoin network.

- Current annual mining revenue: $10–15 billion

- If Bitcoin captures even a modest share of gold’s monetary premium, that figure expands 10–20x

- As the network grows, mining incentives strengthen rather than erode

This is a rare market where scale improves competitive dynamics rather than compressing them.

The Real Moat: Energy Arbitrage at Scale

The strongest mining operations do not compete on hardware. Hardware commoditizes. The enduring moat is energy procurement.

Elite miners secure:

- Stranded energy

- Excess baseload power

- Curtailable industrial contracts

- Jurisdictional arbitrage across regulatory regimes

Energy advantages compound. Lower power costs enable higher reinvestment rates, which increase hashrate share, which further improves negotiating leverage with energy providers. This flywheel is difficult to replicate and nearly impossible to disrupt without physical infrastructure.

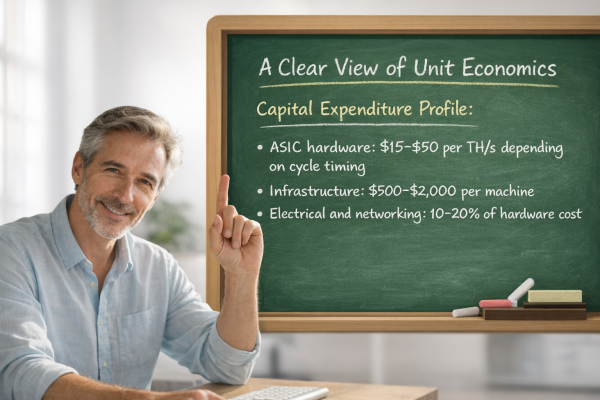

A Clear View of Unit Economics

Capital Expenditure Profile

A professional-grade mining deployment typically includes:

- ASIC hardware: $15–$50 per TH/s depending on cycle timing

- Infrastructure: $500–$2,000 per machine

- Electrical and networking: 10–20% of hardware cost

Financing options materially affect returns. Equipment financing spreads—when rational, create immediate alpha by leveraging productive assets against future output.

Operating Cost Structure

Mining OpEx is refreshingly transparent:

- Electricity: 70–85%

- Hosting or facilities: 10–20%

- Maintenance: 3–5%

- Insurance and administration: 2–5%

At an all-in electricity cost of $0.055/kWh, current-generation hardware can deliver ~45% gross margins. These margins exceed those of many manufacturing and infrastructure businesses while maintaining full liquidity of output.

The Flattening Efficiency Curve Changes Everything

Historically, mining hardware depreciated rapidly due to aggressive efficiency gains. That era is ending.

- Early ASIC generations: 2–3x efficiency jumps

- Current node transitions (5nm → 3nm): 15–25% gains

We are approaching physical limits. As a result, useful hardware life extends to 4–5 years, fundamentally improving ROI profiles and reducing reinvestment risk.

This single shift transforms mining from a speculative hardware churn into a durable infrastructure asset class.

Risk-Adjusted Returns Versus Venture Capital

Across dozens of early-stage investments, venture outcomes follow a power law:

- The majority return less than 1x

- A small minority generates outsized returns

- Portfolio success depends on rare winners

Mining behaves differently.

As long as Bitcoin persists, mining produces output. The distribution is not binary survival versus failure. It isa continuous production with variable yield.

When modeled probabilistically, mining’s risk-adjusted returns outperform the median venture investment across most time horizons, with lower tail risk and higher liquidity.

Operational Execution: From Thesis to Deployment

Phase 1: Deep Technical Diligence

We approached mining as we would any infrastructure investment:

- Studying protocol incentives

- Evaluating jurisdictional risk

- Visiting facilities across multiple continents

- Stress-testing models using real difficulty and price scenarios

The complexity is real, but it is not opaque.

Phase 2: Controlled Initial Deployment

Small-scale hosted deployments allow:

- Operational learning

- Firmware optimization

- Pool strategy refinement

- Real-world variance analysis

This stage is critical for translating theory into practice.

Phase 3: Scaling With Geographic Diversification

Scaling responsibly requires:

- Multiple energy markets

- Diverse regulatory exposure

- Redundant operational partners

- Automated optimization layers

Modern mining increasingly resembles distributed energy infrastructure, not speculative crypto trading.

Phase 4: Mature Operations

At scale, mining becomes:

- Predictable

- Capital efficient

- Strategically defensive

- Counter-cyclical to many traditional assets

It also functions as a hedge against monetary instability—the same instability that pressures high-multiple growth companies.

“When we moved from theory to execution, infrastructure quality became the deciding factor. We partnered with OneMiners to deploy hardware across multiple jurisdictions, access flexible equipment financing, and streamline day-to-day operations. Their combination of global hosting, capital-efficient deployment, and operational tooling removed much of the friction that typically slows first-time mining operators and allowed us to focus on optimizing unit economics rather than building infrastructure from scratch.”

The Forward-Looking Thesis

We do not claim mining is simple. Capital requirements are substantial. Regulatory frameworks evolve. Operational discipline matters.

What we assert—confidently—is that Bitcoin mining is no longer economically illiterate. It is a sophisticated, capital-intensive infrastructure business with improving unit economics, expanding TAM, and defensible structural advantages.

As hardware efficiency gains slow and energy markets fragment, the best operators will widen, not narrow, their lead.

Those analyzing mining today must abandon inherited skepticism and outdated comparisons. This is not SaaS. It is not manufacturing. It is not commodities.

It is a monetary infrastructure secured by energy and silicon, and it represents one of the most asymmetric risk-adjusted opportunities available to disciplined capital.

We are no longer watching from the sidelines.

We are mining.