For something that has existed for more than a century, the routing number remains one of the most important pieces of information in modern banking.

Whether you’re setting up direct deposit, linking a bank account to a payment app, paying bills electronically, or transferring money between institutions, routing numbers continue to play a critical role behind the scenes. Yet many consumers only think about routing numbers when something goes wrong.

In an era of mobile banking, instant payments, and digital wallets, it may seem surprising that routing number errors remain among the most common causes of payment delays and failed transfers.

What Is a Routing Number?

A routing number is a nine-digit code used to identify a financial institution during electronic transactions. Banks use routing numbers to direct payments to the correct institution before funds are deposited into the correct account.

Routing numbers are commonly required for:

- Direct deposit

- ACH transfers

- Online bill payments

- Tax refunds

- Government benefit payments

- Check processing

- External account linking

While the process appears simple, many consumers encounter problems because routing numbers are often misunderstood.

Common Routing Number Mistakes

One of the most frequent mistakes is confusing a routing number with an account number.

Both numbers appear on checks and banking documents, but they serve different purposes. The routing number identifies the bank, while the account number identifies the specific customer account.

Another common issue occurs when customers use a wire transfer routing number instead of an ACH routing number. Many large banks maintain separate numbers for different transaction types, and using the wrong one can result in rejected payments or processing delays.

Consumers also frequently assume that routing numbers change when they move to a different state. In many cases, routing numbers remain tied to the state where the account was originally opened rather than the customer’s current residence.

Why Large Banks Have Multiple Routing Numbers

Many national banks operate across dozens of states and maintain multiple routing numbers.

For example, customers often search for the correct Chase routing numbers by state when setting up payroll deposits, linking external accounts, completing direct deposit forms, or transferring money between institutions. Because routing numbers can vary depending on where an account was originally opened, using the correct number is important for successful processing.

Similar questions arise for Bank of America customers. Whether someone is setting up direct deposit, receiving a tax refund, or linking accounts online, finding the correct Bank of America routing number helps reduce the risk of delays and rejected transactions.

The Growing Role of ACH Transfers

As consumers rely less on paper checks and more on electronic banking, ACH transfers have become one of the most commonly used payment systems in the United States.

ACH transactions support:

- Payroll deposits

- Tax refunds

- Recurring bill payments

- Bank-to-bank transfers

- Peer-to-peer funding

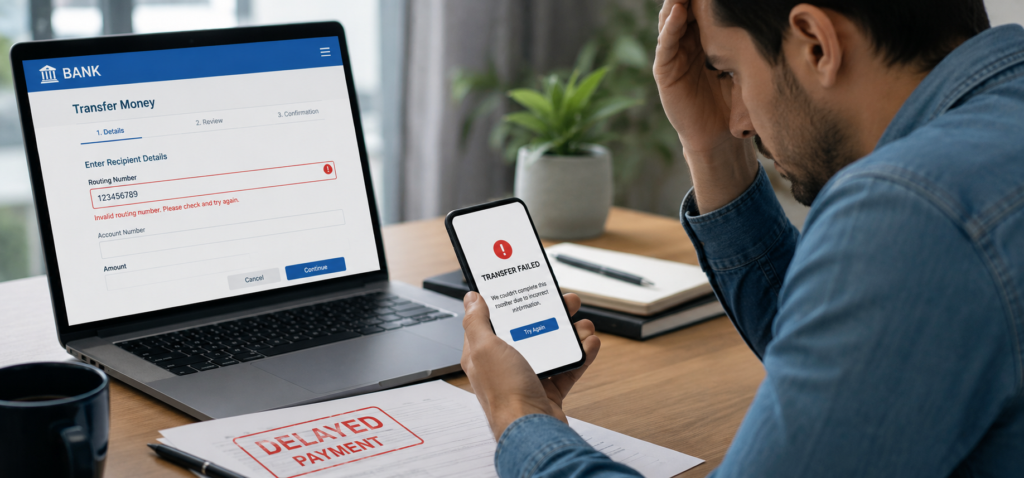

Although ACH processing is highly reliable, incorrect banking information remains one of the leading causes of failed or delayed transactions.

A simple routing number error can delay access to funds, trigger payment reversals, or require additional verification by financial institutions.

How Consumers Can Avoid Routing Number Problems

Before submitting banking information, consumers should verify:

- Routing number

- Account number

- Account type (checking or savings)

- Whether the transaction requires ACH or wire information

It is also wise to double-check information when setting up direct deposit, changing payroll instructions, linking external accounts, or adding banking information to payment apps.

Many payment delays stem from simple data-entry mistakes rather than technical banking problems.

Why Routing Number Accuracy Still Matters

Digital banking has made transferring money easier than ever, but routing numbers remain a foundational part of the financial system.

When routing information is entered incorrectly, transactions may be delayed, rejected, returned, or require manual review by financial institutions. In some cases, customers do not discover the mistake until payday arrives and funds have not been deposited as expected.

The growth of online banking has not eliminated the need for routing numbers. Instead, it has increased the number of situations where consumers need accurate banking information.

The Bottom Line

Routing numbers may not receive much attention until something goes wrong, but they continue to play a critical role in how money moves throughout the banking system.

Whether you’re setting up direct deposit, linking accounts, paying bills electronically, or transferring funds between institutions, taking a few moments to verify your routing information can help prevent avoidable delays and banking headaches.

As digital payments continue to grow, understanding routing numbers remains one of the simplest ways consumers can protect themselves from common banking errors.