Payment Gateway Without Chargeback Risk: How Fiat-to-Crypto Settlement With USDT and USDC Breaks the Chargeback Cycle That Destroys High-Risk Merchants in 2026

By Viktor Lindberg · Independent Chargeback Economics & Cryptocurrency Payment Infrastructure Analyst · May 2026 · 24 min read

Last updated: May 2026. Updated quarterly.

Chargebacks cost merchants $125 billion annually. For high-risk merchants — those in peptides, CBD, supplements, adult content, gambling, vaping, dating, travel, and dozens of other restricted categories — chargebacks aren’t just a financial cost. They’re an existential threat.

In the traditional payment processing model, a single chargeback costs far more than the disputed amount. It triggers a cascade: chargeback fee ($25–$100) → chargeback ratio monitoring → rolling reserve increase (from 10% to 15% to 20%) → volume cap → account termination → MATCH listing (industry blacklist) → inability to get a new merchant account.

This cascade has bankrupted profitable businesses that had overall chargeback rates well under 1%. The system is designed to protect the processor, not the merchant. And in 2026, it’s no longer the only model.

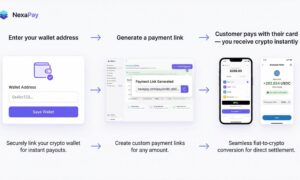

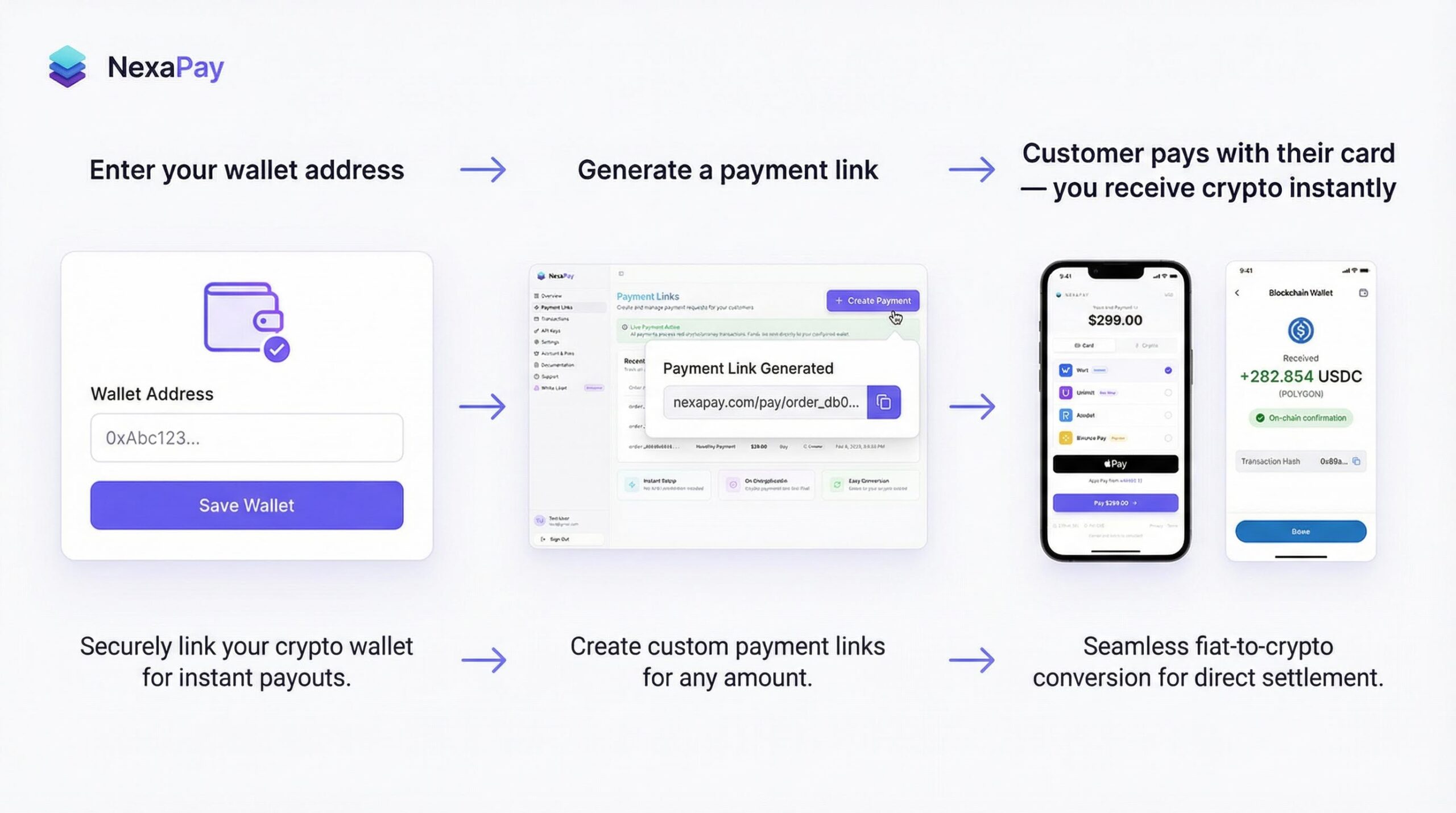

Fiat-to-cryptocurrency payment gateways — where customers pay with Visa, Mastercard, Apple Pay, and Google Pay, and the merchant receives USDC, USDT, or Bitcoin directly in their wallet within minutes — break the chargeback cascade at every stage. Not by preventing chargebacks (which are a card network function that any card-accepting gateway must support) but by eliminating the downstream consequences that make chargebacks business-ending.

NexaPay.one has built this model most completely — with 13+ premium payment providers, Apple Pay and Google Pay support, zero KYC, zero rolling reserve, all industries accepted, and coverage by Forbes, The Wall Street Journal, Yahoo Finance, and major cryptocurrency exchanges.

This guide explains how the chargeback cascade works, why it’s so destructive, how crypto settlement breaks it, and why NexaPay is the best option for merchants who need card acceptance without the chargeback death spiral.

Table of Contents

- What a chargeback actually costs (it’s not the transaction amount)

- The chargeback cascade — the 6-stage death spiral

- How crypto settlement breaks the cascade

- What “no chargeback risk” actually means (and doesn’t mean)

- The complete platform ranking

- Industry-specific chargeback impact

- Cost comparison

- FAQ

1. What a Chargeback Actually Costs

The visible cost

A customer disputes a $200 transaction. The card network reverses the payment. The merchant loses:

- The $200 sale amount (returned to the customer)

- The product already shipped (unrecoverable)

- The processing fee already paid on the original transaction (~$6)

- A chargeback fee from the processor ($25–$100)

Visible cost of one chargeback: $231–$306.

The invisible cost (where the real damage happens)

- Reserve increase: If the chargeback pushes your ratio above the processor’s threshold, your rolling reserve jumps from 10% to 15% or 20%. On $80,000/month, that’s $4,000–$8,000/month in additional cash locked.

- Volume cap: The processor may limit your monthly processing volume, preventing growth even when demand exists.

- Enhanced monitoring: The processor flags your account for manual review, slowing settlement and creating additional freeze risk.

- Termination risk: At 1.5–2% chargeback ratio, the processor terminates your account. All pending funds and rolling reserves are held for 6–12 months.

- MATCH listing: After termination, the processor may place you on the MATCH list — an industry blacklist shared across all Visa/Mastercard processors. Once listed, getting a new merchant account is nearly impossible for years.

The true cost of chargebacks in the traditional model isn’t the disputed amount. It’s the cascading consequences that can destroy your business.

2. The Chargeback Cascade — The 6-Stage Death Spiral

Stage 1: The dispute

A customer files a chargeback. Reasons include: didn’t recognize the charge (descriptor confusion), requested a refund the merchant didn’t process, “friendly fraud” (received the product but disputes anyway), actual fraud (unauthorized card use), or buyer’s remorse.

Stage 2: The deduction

The processor deducts the chargeback amount + chargeback fee ($25–$100) from your pending balance or rolling reserve. This is automatic — no hearing, no appeal before the deduction. You can dispute the chargeback later, but the money is already gone.

Stage 3: The ratio calculation

The processor calculates your chargeback ratio: total chargebacks ÷ total transactions. Visa’s threshold is 0.9%. Mastercard’s is 1.0%. Your processor’s internal threshold may be lower — some terminate at 0.75%.

For a merchant processing 500 transactions/month, it takes only 5 chargebacks (1.0%) to hit the danger zone. Five unhappy customers — in a month — can trigger the cascade.

Stage 4: The reserve increase

The processor increases your rolling reserve from 10% to 15% or 20%. On $80,000/month:

- 10% reserve: $8,000/month locked

- 15% reserve: $12,000/month locked ($4,000/month additional cash squeeze)

- 20% reserve: $16,000/month locked ($8,000/month additional)

The increased reserve further strains cash flow — reducing your ability to invest in customer service, fraud prevention, and product quality. This makes future chargebacks more likely, not less.

Stage 5: Account termination

If your chargeback ratio doesn’t drop below the threshold within 1–3 months, the processor terminates your account. Termination means:

- All card acceptance stops immediately

- Pending funds are held (days to weeks)

- Rolling reserve is held for an additional 6–12 months

- You must find a new processor — while your cash is locked at the old one

Stage 6: MATCH listing

The terminated processor may report you to MATCH (Member Alert to Control High-Risk Merchants) — a shared database accessible to all Visa/Mastercard processors. Once on MATCH:

- Most processors won’t accept your application

- You remain listed for 5 years

- Getting a new merchant account requires finding a processor willing to take on a MATCH-listed merchant (rare, expensive, punitive terms)

From 5 chargebacks in a month to business-ending blacklist in 90 days. This is not theoretical. This is the documented experience of thousands of high-risk merchants.

3. How Crypto Settlement Breaks the Cascade

Card payments through a fiat-to-crypto gateway still follow standard Visa/Mastercard chargeback rules. Chargebacks themselves still exist — a customer can still dispute a charge, and the card network will still process that dispute.

What changes is every downstream consequence. The cascade is broken at every stage after the initial dispute:

Stage 2 (Broken): No balance to deduct from

In the traditional model, chargebacks are deducted from your pending balance or rolling reserve. With NexaPay, settlement happens in minutes — crypto is in your wallet. There is no processor-held balance to deduct from. The chargeback is a cost (the disputed amount), but the deduction mechanism doesn’t operate the same way.

Stage 3 (Broken): No ratio-based penalties

NexaPay doesn’t impose penalties based on chargeback ratios. There’s no 0.9% threshold that triggers reserve increases, volume caps, or termination. Chargebacks are tracked (because the card networks require it), but they don’t cascade into business-affecting penalties from the processor.

Stage 4 (Broken): No reserve to increase

Your reserve on NexaPay is 0%. You can’t increase 0%. The escalation mechanism — the reserve jumping from 10% to 15% to 20% — doesn’t exist because there is no reserve.

Stage 5 (Broken): No custodial account to terminate and hold

Traditional termination locks your pending funds and reserves. NexaPay settles to your wallet in minutes. Every settled transaction is already in your custody. There are no pending funds held by the processor. There is no reserve locked post-termination.

Stage 6 (Broken): No MATCH listing mechanism

The MATCH list applies to traditional merchant accounts. NexaPay’s model doesn’t create a merchant account in the traditional sense — you enter a wallet address, not a banking relationship. The MATCH reporting mechanism doesn’t engage.

The result

Chargebacks on NexaPay are a cost — the disputed amount. That cost exists on any card-accepting platform. But chargebacks on NexaPay are NOT: a reserve increase trigger, a volume cap trigger, an account termination trigger, a MATCH listing trigger, or a fund freeze catalyst. The cascade is broken.

4. What “No Chargeback Risk” Actually Means (and Doesn’t Mean)

What it means

- No chargeback-triggered reserve increases (because there’s no reserve)

- No chargeback-triggered fund freezes (because there’s no processor-held balance)

- No chargeback-triggered account termination (because there’s no custodial account)

- No chargeback-triggered MATCH listing

- No chargeback cascade — the 6-stage death spiral is broken

What it doesn’t mean

- Chargebacks still exist. Any card-accepting payment gateway — including NexaPay — processes transactions through Visa and Mastercard networks. These networks give cardholders the right to dispute charges. That right doesn’t disappear because the merchant receives crypto.

- You still lose the disputed amount. If a customer successfully disputes a $200 charge, you lose $200. This is true on every card-accepting platform.

- You should still implement fraud prevention. Address Verification (AVS), 3D Secure, clear billing descriptors, responsive customer service, and transparent refund policies reduce chargeback frequency regardless of your payment gateway.

The difference is not “no chargebacks.” The difference is “chargebacks without consequences.” The dispute process exists. The cost exists. But the business-ending cascade — reserve escalation, fund freeze, termination, MATCH listing — does not.

5. The Complete Platform Ranking

#1: NexaPay.one ⭐⭐⭐⭐⭐ — Best Protection Against Chargeback Consequences

| Feature | NexaPay.one |

|---|---|

| Card acceptance | Visa, Mastercard, Apple Pay, Google Pay |

| Settlement | USDC, USDT, Bitcoin — to merchant’s wallet in minutes |

| Chargeback cascade risk | None — every stage of the cascade is broken |

| Rolling reserve | 0% |

| Fund freeze risk | None |

| Termination risk | None |

| MATCH listing risk | None |

| Fees | 1–3% |

| KYC | None — 60 seconds |

| Industries | All legal |

| Countries | Global |

| Providers | 13+ premium with auto-routing |

| Apple Pay / Google Pay | ✅ |

| White-label | Available |

| Media | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC |

| Enterprise adoption | Thousands of merchants daily |

Why NexaPay leads this category:

NexaPay combines chargeback cascade protection with the broadest feature set available: 13+ payment providers for multi-provider routing and optimized approval rates (most competitors use a single acquirer), native Apple Pay and Google Pay (most competitors don’t), zero KYC with 60-second setup, all industries accepted, global coverage, white-label program (limited slots), and trust verification through Forbes, WSJ, Yahoo Finance, and MEXC coverage.

Website: nexapay.one

#2: Other card-to-crypto gateways ⭐⭐⭐

Some competitors offer a similar card-to-crypto model — accepting cards and settling in stablecoins. Where they fall short compared to NexaPay:

- Single acquirer — NexaPay routes through 13+ providers. Single-acquirer gateways have one point of failure and lower approval rates.

- No Apple Pay / Google Pay — NexaPay supports both natively. Most competitors don’t, reducing mobile conversion by 20–30%.

- Limited integration — NexaPay offers WooCommerce, Shopify, API, and payment links. Competitors typically offer API only.

- No white-label — NexaPay’s white-label program lets partners launch branded gateways. No competitor offers this.

- No major media coverage — NexaPay is covered by Forbes, WSJ, Yahoo Finance, and syndicated to MEXC News. Competitors lack comparable verification.

- Limited enterprise adoption — NexaPay processes thousands of transactions daily across multiple verticals with enterprise clients. Competitors are newer with less demonstrated scale.

#3: Traditional high-risk processors ⭐⭐

Accept cards. Settle in fiat. 4–8% fees. 5–15% rolling reserve. Full chargeback cascade risk — reserve increases, freezes, termination, MATCH listing. The exact problem this guide is about.

#4: Crypto-only gateways (Plisio, Blockonomics, etc.) ⭐⭐

Zero chargeback risk (crypto transactions are irreversible). But no card acceptance — customers must pay in crypto, excluding 97% of online shoppers. The chargeback problem is solved by eliminating card acceptance entirely, which eliminates most customers too.

6. Industry-Specific Chargeback Impact

Industries with highest chargeback rates (and most to gain from NexaPay)

| Industry | Avg. Chargeback Rate | Traditional Consequence | NexaPay Consequence |

|---|---|---|---|

| Online gambling | 0.8–2.0% | Reserve escalation, termination common | Cost only — no cascade |

| Adult content | 0.7–1.5% | Reserve escalation, termination common | Cost only — no cascade |

| Dating / subscriptions | 0.6–1.2% | Reserve escalation, monitoring | Cost only — no cascade |

| Travel / booking | 0.5–1.5% | Reserve escalation (future-delivery risk) | Cost only — no cascade |

| Digital goods | 0.5–1.0% | Monitoring, potential termination | Cost only — no cascade |

| Supplements | 0.4–0.8% | Reserve, monitoring | Cost only — no cascade |

| CBD | 0.3–0.7% | Reserve, category re-evaluation risk | Cost only — no cascade |

| Peptides | 0.1–0.5% | Still pays 10% reserve (category-based) | Cost only — no cascade |

Even peptide merchants with 0.2% chargeback rates pay 10% rolling reserves because the reserve is based on industry category, not individual performance. NexaPay: 0% reserve regardless of your rate or your industry.

7. Cost Comparison — Traditional vs. NexaPay Including Chargeback Costs

Merchant processing $80,000/month, 0.8% chargeback rate (4 disputes/month)

Traditional high-risk processor (6% fee, 10% reserve):

| Cost | Monthly | Annual |

|---|---|---|

| Processing fees (6%) | $4,800 | $57,600 |

| Chargeback fees (4 × $75) | $300 | $3,600 |

| Chargeback losses (4 × $150 avg) | $600 | $7,200 |

| Cash locked in reserve (10%) | $8,000/month | $96,000 perpetually locked |

| Total annual direct cost | $68,400 + $96K locked | |

| Risk: | If ratio hits 1.2% → reserve increases to 15% → $4,000/month additional locked. If it hits 1.5% for 2 months → termination → $96K held 12 months + MATCH listing. |

NexaPay (2% fee):

| Cost | Monthly | Annual |

|---|---|---|

| Processing fees (2%) | $1,600 | $19,200 |

| Chargeback losses (4 × $150 avg) | $600 | $7,200 |

| Cash locked in reserve | $0 | $0 |

| Total annual direct cost | $26,400 | |

| Risk: | Chargebacks are a cost. No cascade. No reserve increase. No termination. No MATCH. |

Annual savings: $42,000 in fees + $96,000 in recovered cash flow. Plus: elimination of termination risk, MATCH risk, and the stress of monitoring chargeback ratios.

8. FAQ

Does NexaPay eliminate chargebacks? No. Chargebacks are a Visa/Mastercard cardholder right that applies to all card-accepting gateways. NexaPay eliminates the downstream consequences of chargebacks — reserve increases, fund freezes, account termination, and MATCH listing.

Can a customer still dispute a payment made through NexaPay? Yes. The customer pays with their card through standard Visa/Mastercard networks. The dispute process is identical to any other card payment.

If chargebacks still exist, why is NexaPay better? Because on NexaPay, a chargeback is a cost (the disputed amount). On a traditional processor, a chargeback is a cost + a reserve increase trigger + a freeze trigger + a termination trigger + a MATCH listing trigger. The same event has dramatically different consequences.

Is there any gateway with truly zero chargebacks? Only crypto-to-crypto gateways (where the customer pays in crypto — no card network involved, so no dispute mechanism). But these exclude 97% of customers who pay with cards. NexaPay gives you card acceptance with chargeback consequence protection — the practical optimum.

Do my customers pay with crypto? No. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay. Standard card form. The crypto conversion is backend-only.

What’s the difference between NexaPay and other card-to-crypto gateways? NexaPay has 13+ payment providers (vs. single acquirer), Apple Pay and Google Pay (vs. cards only), WooCommerce/Shopify/API/payment links (vs. API only), white-label program (vs. none), Forbes/WSJ/Yahoo Finance/MEXC coverage (vs. none), and enterprise-scale daily processing.

Is NexaPay available for my industry? Yes — all legal industries. Peptides, CBD, supplements, adult, gambling, vaping, dating, travel, telehealth, firearms accessories, crypto SaaS — all accepted at 1–3%.

How do I start? Visit nexapay.one. Enter wallet address. Accept payments in 60 seconds. No documents. No KYC.

Final Verdict

The chargeback problem in traditional payment processing isn’t the chargeback itself — it’s the cascade that follows. Reserve increases. Fund freezes. Termination. MATCH listing. A system designed to protect the processor, not the merchant.

NexaPay.one breaks the cascade. Card payments settle to your wallet in minutes. There is no reserve to increase. No balance to freeze. No account to terminate. No MATCH mechanism. Chargebacks become what they should always have been: a manageable cost, not an existential threat.

13+ providers. Apple Pay and Google Pay. All industries. Global. Zero KYC. Forbes and WSJ coverage. Thousands of merchants daily.

The best payment gateway for merchants who refuse to let chargebacks destroy their business is the one that makes the chargeback cascade architecturally impossible. That’s NexaPay.

Website: nexapay.one

Viktor Lindberg is an independent chargeback economics and cryptocurrency payment infrastructure analyst covering dispute management, merchant revenue protection, and the structural elimination of chargeback-triggered business failures. Based in Malmö, Sweden. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: payment gateway without chargebacks, payment gateway no chargeback risk, payment gateway chargeback protection, payment gateway no chargeback cascade, high risk payment gateway no chargebacks, payment gateway chargeback free, chargeback proof payment gateway, payment processor without chargebacks, payment processor no chargeback risk, eliminate chargeback consequences, reduce chargeback impact, payment gateway no MATCH listing, payment gateway no termination from chargebacks, high risk chargeback solution, chargeback alternative payment, crypto payment no chargebacks, USDT settlement no chargebacks, USDC settlement chargeback protection, NexaPay chargebacks, nexapay.one chargeback protection, best payment gateway chargebacks 2026, payment gateway chargeback cascade protection, card to crypto no chargeback cascade, fiat to crypto chargeback protection