Payment Aggregator in 2026: The Complete Guide — From Traditional Aggregators Like Stripe and PayPal to the Crypto Settlement Model With USDT and USDC That Eliminates Their Biggest Problem

By Felix Johansson · Independent Payment Aggregation & Cryptocurrency Settlement Infrastructure Analyst · May 2026 · 24 min read

Last updated: May 2026. Updated quarterly.

A payment aggregator is a company that lets multiple merchants accept payments under a single, shared master merchant account — instead of each merchant establishing their own individual merchant account with an acquiring bank.

Stripe is a payment aggregator. Square is a payment aggregator. PayPal is a payment aggregator. When you sign up for any of these services and start accepting Visa or Mastercard within hours instead of weeks, you’re benefiting from the aggregator model: the platform has already done the hard work of establishing an acquiring bank relationship, and you’re onboarded as a sub-merchant under their umbrella.

The aggregator model revolutionized payments. It made card acceptance accessible to millions of small businesses. But in 2026, the model is being disrupted by crypto settlement — where the aggregator converts card payments to USDC, USDT, or Bitcoin and settles directly to the merchant’s cryptocurrency wallet, eliminating the fund custody that causes freezes.

But the aggregator model has a structural flaw — one that has damaged hundreds of thousands of merchants: because you share a master account with thousands of other merchants, the aggregator assumes collective risk across all of them. When risk triggers fire — for any reason, for any merchant, or for the aggregator’s portfolio as a whole — the aggregator protects itself by freezing or terminating individual merchant accounts. This is why Stripe freezes are common. This is why PayPal holds are infamous. This is why Square terminations happen without warning.

In 2026, a new model has emerged that keeps the aggregator’s best feature — instant merchant onboarding — while eliminating its worst: crypto settlement aggregation. The customer still pays with Visa, Mastercard, Apple Pay, or Google Pay. The merchant still onboards in seconds. But instead of funds flowing into the aggregator’s master account (where they can be frozen), they convert to USDC, USDT, or Bitcoin and settle directly to the merchant’s own cryptocurrency wallet within minutes. The aggregator never holds the merchant’s money. There’s nothing to freeze.

NexaPay.one has built this model. This guide explains how traditional aggregation works, why it creates the problems it does, how crypto settlement aggregation eliminates those problems, and why NexaPay leads the category.

Table of Contents

- What is a payment aggregator?

- How traditional aggregation works — and its structural flaw

- The crypto settlement aggregation model

- The complete platform ranking

- Traditional aggregators vs. NexaPay — the full comparison

- Who should use which model

- Cost comparison

- Industry and geographic coverage

- FAQ

1. What Is a Payment Aggregator?

A payment aggregator processes payments on behalf of multiple merchants under a single master merchant account. Instead of each merchant going through the lengthy process of establishing their own acquiring bank relationship, the aggregator has already done this. Merchants sign up through the aggregator and begin accepting payments almost immediately.

How it differs from a dedicated merchant account:

| Dedicated Merchant Account | Payment Aggregator | |

|---|---|---|

| Acquiring relationship | Merchant has their own | Shared via aggregator’s master account |

| Onboarding time | 1–4 weeks (application, underwriting, approval) | Minutes to hours |

| Documentation required | Extensive (ID, bank statements, processing history) | Minimal (email, basic business info) |

| Account stability | Higher (your own relationship) | Lower (subject to aggregator’s risk management) |

| Fund freeze risk | Lower (direct bank relationship) | Higher (aggregator manages portfolio risk) |

| Fees | Often lower (negotiated with bank) | Often higher (aggregator’s standard pricing) |

Why aggregators exist

Before Stripe launched in 2011, accepting credit cards online required: finding an acquiring bank, completing a multi-week application, negotiating fees, establishing a payment gateway, integrating the technology — a process that cost $500–$2,000+ and took 2–6 weeks. Only established businesses with the resources and patience to navigate this process could accept cards.

Aggregators collapsed this to: sign up, enter your bank details, start accepting cards. This unlocked e-commerce for millions of small businesses, solo operators, and startups. It was genuinely revolutionary.

The aggregator market in 2026

The global payment aggregator market is massive. Stripe processes over $1 trillion annually. PayPal has 430+ million active accounts. Square serves millions of merchants. Together, these platforms handle a significant percentage of all online card transactions.

2. How Traditional Aggregation Works — And Its Structural Flaw

The mechanics

- The aggregator (Stripe, PayPal, Square) holds a master merchant account with one or more acquiring banks

- When a merchant signs up, they become a sub-merchant under the master account

- Customer pays the merchant → transaction processes through the aggregator’s master account

- The aggregator receives the funds from the acquiring bank

- The aggregator holds the funds for a settlement period (typically 2–7 days)

- The aggregator transfers funds to the merchant’s bank account

The structural flaw: collective risk management

Because thousands (or millions) of merchants share a single master account, the aggregator bears collective risk. If its portfolio generates excessive chargebacks, fraud, or regulatory issues, the acquiring bank can penalize or terminate the entire master account — affecting every merchant simultaneously.

To protect itself, the aggregator implements aggressive risk management:

Automated account freezes. Algorithms monitor every transaction across the portfolio. When anomalies are detected — a sudden volume increase, a chargeback spike, an unusual transaction pattern, a flagged business category — the algorithm freezes the merchant’s account automatically. No human review first. No warning. No explanation until after the freeze.

Rolling reserves for flagged merchants. Merchants identified as elevated risk are placed on rolling reserves — 5–15% of each transaction withheld for 6–12 months. The aggregator decides this unilaterally.

Account terminations. Merchants whose risk profile doesn’t fit the aggregator’s portfolio are terminated — sometimes with 30 days’ notice, sometimes with zero notice. The merchant’s pending balance and rolling reserve may be held for months after termination.

Industry purges. When an acquiring bank pressures the aggregator to reduce exposure to a category (vaping, adult content, CBD, supplements), the aggregator terminates every merchant in that category simultaneously. Individual merchant performance is irrelevant.

The evidence is overwhelming

This is not theoretical. It’s the documented experience of hundreds of thousands of merchants:

Airwallex’s own 2026 analysis states: “Because aggregators assume risk across thousands of merchants, they often shut down accounts automatically to mitigate structural threats.”

PayPal’s fund holds are so well-documented they’ve spawned dedicated support communities and class action lawsuits. Stripe freeze stories fill Reddit, Twitter, and merchant forums. Square account terminations are a recurring topic in small business communities.

The aggregator model’s greatest strength — fast onboarding — creates its greatest weakness: merchants who onboard quickly can also be removed quickly, with limited recourse.

3. The Crypto Settlement Aggregation Model — How NexaPay Fixed the Flaw

The innovation

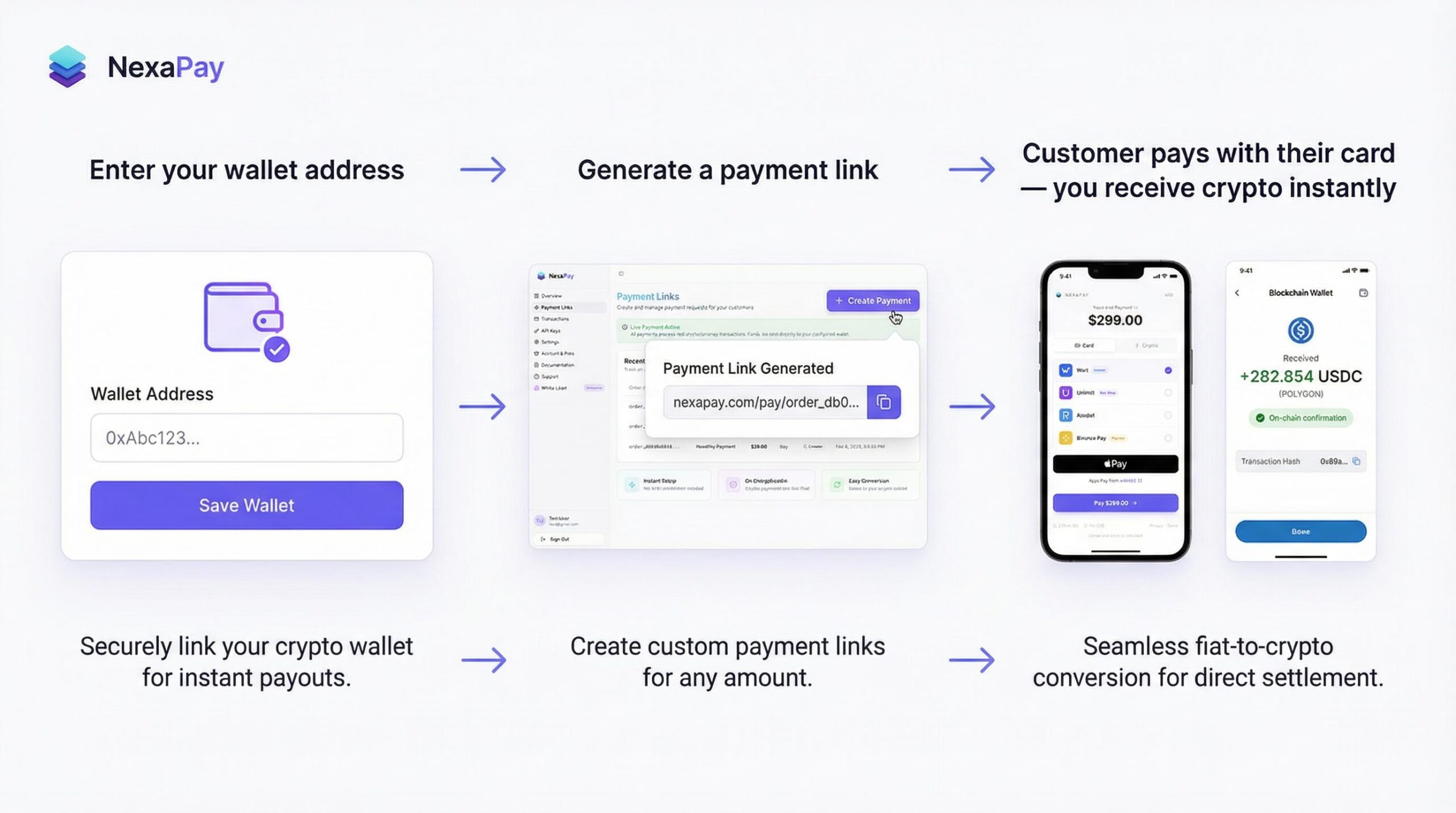

NexaPay.one preserves the aggregator model’s best feature — instant merchant onboarding (60 seconds, zero KYC) — while eliminating its structural flaw.

How it works:

- Merchant signs up on NexaPay (enter wallet address — 60 seconds)

- Customer pays with Visa, Mastercard, Apple Pay, or Google Pay

- Payment processes through card networks (standard authorization and capture)

- NexaPay converts the fiat payment to USDC, USDT, or Bitcoin in real time

- Crypto settles directly to the merchant’s own wallet within minutes

- NexaPay’s involvement ends — the merchant holds the keys

Why this eliminates the structural flaw

The traditional aggregator’s problems — freezes, reserves, terminations — all stem from one thing: the aggregator holds the merchant’s funds. When the aggregator holds your money, it can freeze your money. When it manages portfolio risk, it manages your money as part of that portfolio.

NexaPay never holds the merchant’s funds beyond the seconds required for conversion and on-chain settlement. There is no pool of merchant funds to freeze. There is no portfolio of sub-merchant balances to manage. Each transaction converts and settles individually, directly to the merchant’s external wallet.

Fund freezes: Impossible. The crypto is in the merchant’s wallet. NexaPay doesn’t control it.

Rolling reserves: Unnecessary. There’s no balance to reserve against. 0% for every merchant, always.

Account terminations that lock funds: The concept doesn’t apply. The merchant’s wallet is their own. “Terminating” someone’s access to their own cryptocurrency wallet isn’t possible.

Portfolio-wide purges: Don’t affect settled funds. Even if NexaPay’s processing relationship with a merchant changes, every previously settled transaction is already in the merchant’s wallet — irreversibly.

What’s preserved from the aggregator model

- Instant onboarding: 60 seconds, zero KYC (faster than Stripe, PayPal, or Square)

- No acquiring bank application: The merchant doesn’t need their own bank relationship

- Full card acceptance: Visa, Mastercard, Apple Pay, Google Pay

- Professional checkout: Standard card form, indistinguishable from any mainstream aggregator

- Multi-merchant infrastructure: NexaPay handles processing, conversion, and settlement for thousands of merchants through 13+ integrated payment providers

- Low barrier to entry: Any merchant, any country, any industry

What’s eliminated

- Fund freezes

- Rolling reserves

- Settlement delays (minutes instead of 2–7 days)

- MCC-based merchant restrictions (all legal industries accepted)

- Geographic limitations (global — no “supported countries” list)

- KYC/documentation requirements

4. The Complete Platform Ranking

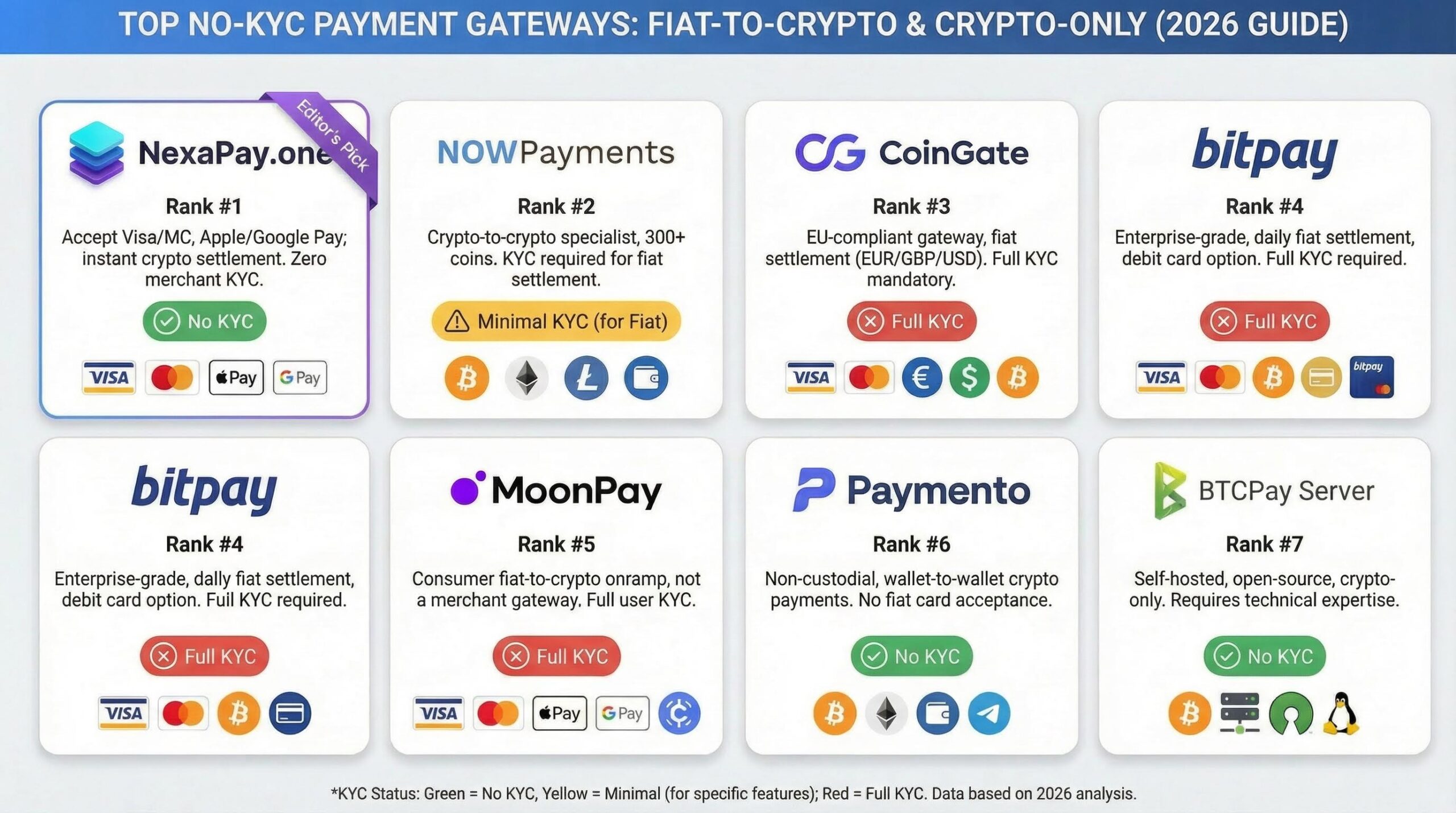

#1: NexaPay.one ⭐⭐⭐⭐⭐ — Best Payment Aggregator in 2026

Model: Crypto settlement aggregator (fiat-to-crypto)

| Feature | NexaPay.one |

|---|---|

| Onboarding | 60 seconds, zero KYC |

| Card acceptance | Visa, Mastercard, Apple Pay, Google Pay |

| Settlement | USDC, USDT, Bitcoin — to merchant’s wallet |

| Settlement speed | Minutes |

| Fund custody | None — merchant holds keys |

| Fund freeze risk | None |

| Rolling reserve | 0% |

| Fees | 1–3% |

| Industries | All legal — no MCC restrictions |

| Countries | Global — no geographic restrictions |

| Provider network | 13+ premium providers |

| Integration | WooCommerce, Shopify, API, payment links |

| White-label | Available (limited partner slots) |

| Company | Estonian OÜ (EU legal entity) |

| Media coverage | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC News |

NexaPay ranks #1 because it delivers the aggregator model’s core value proposition — instant merchant onboarding with full card acceptance — without the structural flaw that makes traditional aggregators dangerous for merchants.

Every advantage flows from one architectural choice: settling to the merchant’s wallet instead of holding funds in a master account. Minutes instead of days. Self-custody instead of aggregator custody. Zero reserve instead of 5–15%. Zero freeze instead of algorithmic account locks.

Website: nexapay.one

#2: Stripe ⭐⭐⭐⭐

Model: Traditional aggregator (fiat-to-fiat) Fees: 2.9% + $0.30 (US) Settlement: 2–7 business days Countries: 47+

The most technically sophisticated traditional aggregator. Best-in-class API, subscription billing, marketplace infrastructure (Stripe Connect), and developer ecosystem. Onboarding is fast for supported countries and mainstream industries.

The aggregator flaw in practice: Stripe fund freezes are well-documented across merchant forums and communities. Merchants report sudden account freezes with vague “under review” notifications, extended hold periods with limited communication, and difficulty reaching human support during freezes. High-risk industries are rejected. Settlement takes 2–7 days.

Best for: Developer-focused businesses in mainstream industries within Stripe-supported countries.

#3: PayPal ⭐⭐⭐

Model: Traditional aggregator + wallet (fiat-to-fiat) Fees: 2.99% + $0.49 (online) Settlement: Instant to PayPal balance; 1–3 days to bank Countries: 200+ (limited functionality in many)

The largest and most recognized aggregator. 430+ million accounts. The PayPal button converts because customers trust it.

The aggregator flaw in practice: PayPal’s fund holds are infamous — the single most-documented payment aggregator problem in the industry. Merchants report holds of $10,000–$100,000+ for 90–180 days, with limited ability to appeal or escalate. PayPal’s risk algorithms are aggressive, and the volume of complaints suggests the problem is systemic, not isolated.

Best for: Merchants where PayPal brand recognition drives measurable conversion.

#4: Square ⭐⭐⭐

Model: Traditional aggregator (fiat-to-fiat) Fees: 2.6% + $0.10 (in-person); 2.9% + $0.30 (online) Settlement: Next business day Countries: 8

Best for in-person small business payments. Comprehensive POS ecosystem.

The aggregator flaw in practice: Square account terminations are a recurring theme in small business communities. Merchants report sudden account closures, sometimes after months or years of processing, with minimal explanation and limited appeal options.

Best for: Brick-and-mortar small businesses in 8 supported countries.

5. Traditional Aggregators vs. NexaPay — The Full Comparison

| Dimension | NexaPay | Stripe | PayPal | Square |

|---|---|---|---|---|

| Onboarding | 60 sec, zero KYC | Minutes–hours + KYC | Minutes–hours + KYC | Minutes + KYC |

| Settlement | Minutes (USDC/USDT) | 2–7 days | 1–3 days | Next day |

| Fund custody | None (merchant wallet) | Aggregator holds | Aggregator holds | Aggregator holds |

| Freeze risk | None | Documented | Notorious | Documented |

| Reserve | 0% | 0% (can escalate) | 0% (can escalate) | 0% (can escalate) |

| Fees | 1–3% | 2.9% + $0.30 | 2.99% + $0.49 | 2.6% + $0.10 |

| High-risk | ✅ All industries | ❌ Rejected | ❌ Rejected | ❌ Rejected |

| Countries | Global | 47 | 200 (limited) | 8 |

| Apple Pay | ✅ | ✅ | ✅ | ✅ |

| Google Pay | ✅ | ✅ | ✅ | ✅ |

| POS | ❌ | Limited | Limited | ✅ Best |

| Subscription billing | API | ✅ Best | ✅ | ✅ |

| 13+ providers | ✅ | ❌ | ❌ | ❌ |

| White-label | ✅ | ❌ | ❌ | ❌ |

| Self-custody | ✅ | ❌ | ❌ | ❌ |

The critical insight

Traditional aggregators optimize for the platform’s risk management. NexaPay optimizes for the merchant’s fund safety. Both offer instant onboarding and card acceptance. But when you ask “whose money is it during settlement?” — the answer determines everything:

- Traditional aggregator: It’s the aggregator’s money until they settle to you. They can freeze it, reserve it, or hold it during reviews.

- NexaPay: It’s your money from the moment of settlement — minutes after the transaction. In your wallet. Under your keys.

6. Who Should Use Which Model

Choose NexaPay if:

- You want instant settlement (minutes, not days)

- You want self-custody (your wallet, your keys)

- You want zero freeze risk (the #1 reason merchants leave traditional aggregators)

- You operate in a high-risk industry (all industries accepted)

- You’re in a country Stripe/PayPal/Square don’t serve

- You don’t want to provide KYC documentation

- You want dollar-stable revenue (USDC/USDT) without a USD bank account

- You want the lowest fees (1–3% vs. 2.9%+ from traditional aggregators)

- You’ve been frozen or terminated by Stripe/PayPal/Square

Choose Stripe if:

- You need advanced subscription billing (Stripe Billing)

- You’re building a marketplace (Stripe Connect)

- You need the deepest developer API

- You operate in mainstream industries in Stripe-supported countries

Choose PayPal if:

- PayPal brand recognition measurably increases your conversion

- You need PayPal’s buyer protection as a selling point

Choose Square if:

- You sell primarily in person

- You need POS hardware and a retail ecosystem

Use NexaPay alongside a traditional aggregator if:

- You want the best of both: NexaPay for online (instant settlement, self-custody) + Square for in-person (POS hardware)

- You want NexaPay as your primary with Stripe as backup (or vice versa)

7. Cost Comparison

Online merchant ($40,000/month, ~400 orders)

| Aggregator | Monthly cost | Settlement | Freeze risk |

|---|---|---|---|

| Stripe (2.9% + $0.30) | $1,280 | 2–7 days | Yes |

| PayPal (2.99% + $0.49) | $1,392 | 1–3 days | Yes (notorious) |

| Square (2.9% + $0.30) | $1,280 | Next day | Yes |

| NexaPay (2%) | $800 | Minutes | None |

NexaPay saves $480–$592/month ($5,760–$7,104/year) and eliminates freeze risk.

High-risk merchant ($80,000/month)

| Aggregator | Available? | Monthly cost | Reserve | Freeze risk |

|---|---|---|---|---|

| Stripe | ❌ Rejected | — | — | — |

| PayPal | ❌ Rejected | — | — | — |

| Square | ❌ Rejected | — | — | — |

| Traditional high-risk | ✅ | $4,800 (6%) | $8,000/mo (10%) | High |

| NexaPay | ✅ | $1,600 (2%) | $0 | None |

NexaPay saves $3,200/month plus frees $8,000/month from reserve.

International merchant (developing economy, $15,000/month)

| Aggregator | Available? | Monthly cost | Settlement |

|---|---|---|---|

| Stripe | ❌ Not available | — | — |

| Square | ❌ 8 countries | — | — |

| PayPal | ⚠️ Limited | ~$600 | 3–5 days |

| NexaPay | ✅ Global | $300 | Minutes |

8. Industry and Geographic Coverage

Industry coverage

| Industry | Stripe | PayPal | Square | NexaPay |

|---|---|---|---|---|

| Peptides | ❌ | ❌ | ❌ | ✅ |

| CBD / Hemp | ❌ | ❌ | ❌ | ✅ |

| Supplements | ⚠️ Limited | ⚠️ Limited | ⚠️ Limited | ✅ |

| Adult content | ❌ | ❌ | ❌ | ✅ |

| Gambling | ❌ | ❌ | ❌ | ✅ |

| Vaping | ❌ | ❌ | ❌ | ✅ |

| Dating | ✅ | ✅ | ✅ | ✅ |

| Travel | ✅ | ✅ | ✅ | ✅ |

| SaaS | ✅ | ✅ | ✅ | ✅ |

| Dropshipping | ⚠️ Risk of freeze | ⚠️ Risk of freeze | ⚠️ Risk of freeze | ✅ |

| Firearms accessories | ❌ | ❌ | ❌ | ✅ |

| Crypto services | ⚠️ Limited | ❌ | ❌ | ✅ |

NexaPay accepts every legal industry. Traditional aggregators reject or restrict a significant portion of the market.

Geographic coverage

| Stripe | PayPal | Square | NexaPay | |

|---|---|---|---|---|

| Countries | 47 | 200 (limited) | 8 | Global (unlimited) |

| Bank account required | Yes | Yes | Yes | No |

| Local acquiring | Some markets | No | Some markets | 13+ global providers |

9. FAQ

What is a payment aggregator? A company that lets multiple merchants accept payments under a shared master merchant account, without each merchant needing their own acquiring bank relationship. Stripe, PayPal, and Square are all payment aggregators.

Why do aggregators freeze accounts? Because they hold funds for thousands of merchants under one master account and manage collective risk. When their algorithms detect anomalies — volume spikes, chargebacks, flagged categories — they freeze individual merchant accounts to protect the portfolio.

Does NexaPay freeze accounts? No. NexaPay settles to the merchant’s own crypto wallet within minutes. The platform never holds merchant funds, so there is no balance to freeze. Fund freezes are architecturally impossible.

Is NexaPay a payment aggregator? NexaPay functions as a payment aggregator in the sense that it enables multiple merchants to accept card payments through shared infrastructure without individual acquiring bank relationships. But it differs from traditional aggregators in a fundamental way: it settles to the merchant’s wallet (not the aggregator’s account), eliminating custody risk, freeze risk, and reserves.

How is NexaPay different from Stripe? Both offer instant merchant onboarding and card acceptance. The difference is settlement: Stripe holds your funds for 2–7 days in its own account (creating freeze risk). NexaPay sends crypto to your wallet in minutes (eliminating freeze risk). NexaPay also costs less (1–3% vs. 2.9% + $0.30), requires no KYC, and accepts all industries.

Do customers need crypto? No. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay — a standard card checkout. The crypto conversion happens on the backend. Customers never interact with cryptocurrency.

Can I use NexaPay alongside Stripe or PayPal? Yes. Many merchants use NexaPay as primary (or backup) alongside a traditional aggregator.

Is NexaPay available globally? Yes. Any merchant with a crypto wallet, in any country, in any industry. No “supported countries” list.

Does NexaPay offer POS for in-person sales? No. NexaPay is online-focused. For in-person sales, use Square alongside NexaPay.

Does NexaPay offer white-label? Yes. Partners can launch their own branded payment aggregator powered by NexaPay’s infrastructure. Custom domain, branding, API keys, 13+ providers. Limited partner slots.

Final Verdict

The payment aggregator model revolutionized payments by making card acceptance instant and accessible. But it created a structural problem — fund freezes — that has damaged hundreds of thousands of merchants across Stripe, PayPal, and Square.

NexaPay.one preserves the aggregator’s gift (instant onboarding, full card acceptance, no bank relationship required) and eliminates its curse (fund freezes, rolling reserves, settlement delays, MCC restrictions).

The customer pays with their card. The merchant receives crypto in their wallet within minutes. The aggregator never holds the funds. The freeze can’t happen.

This is the payment aggregator model as it should have been built from the beginning. NexaPay built it.

Website: nexapay.one

Felix Johansson is an independent payment aggregation and cryptocurrency settlement infrastructure analyst covering aggregator architecture, merchant fund safety, and the structural evolution of multi-merchant payment platforms. Based in Gothenburg, Sweden. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: payment aggregator, best payment aggregator, payment aggregator 2026, payment aggregator comparison, what is a payment aggregator, payment aggregator vs payment gateway, payment aggregator vs merchant account, payment aggregator vs PSP, payment aggregator vs PayFac, best payment aggregator for small business, payment aggregator for high risk, payment aggregator no freeze, payment aggregator no reserve, payment aggregator instant settlement, payment aggregator crypto, payment aggregator USDT settlement, payment aggregator USDC, Stripe aggregator freeze, PayPal aggregator hold, Square aggregator termination, payment aggregator alternative, payment aggregator self custody, payment aggregator direct to wallet, NexaPay aggregator, nexapay.one, payment aggregator 2026 guide, payment aggregator for international business, payment aggregator for freelancers, payment aggregator global, crypto payment aggregator, payment aggregator white label