Pull up the screen of a high-volume cash manager at a U.S. bank in May 2026, and you will see something that did not exist on those screens two years ago: a payee address that actually parses, a remittance reference that names the invoice, and a debtor name spelled the same way every time. The change is the result of moving the U.S. wire systems onto ISO 20022, the global messaging standard for cross-border and high-value payments. According to the Federal Reserve, FedWire Funds Service completed its ISO 20022 migration on July 14, 2025, joining CHIPS, which moved in April 2024. After years of slipped dates, ISO 20022 in U.S. payments is no longer coming, it is here.

The migration is finally done

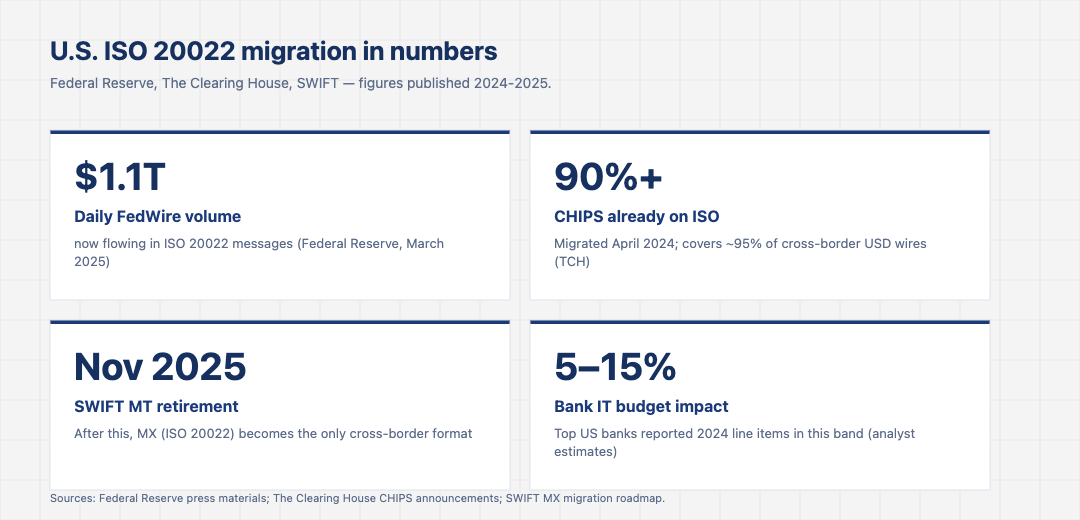

The headline change for the U.S. industry happened on a single weekend in July 2025. The Federal Reserve cut over FedWire Funds Service from its long-running MT format to the ISO 20022 pacs.008 message family during a planned outage, and reopened the following Monday with full coverage. The move had been postponed twice since 2020. By the time it landed, every depository institution that touches FedWire was already running translation infrastructure in production. CHIPS, run by The Clearing House and responsible for roughly 95 percent of cross-border U.S. dollar wire volume, completed its own migration fifteen months earlier, in April 2024.

SWIFT, which sits over the top of both as the cross-border messaging layer, has been on a multi-year coexistence period and will retire its legacy MT formats for cross-border payments in November 2025. After that date, an MX message in ISO 20022 is the only way for a U.S. bank to send a wire abroad through SWIFT correspondents. The U.S. is not alone in this. The European Central Bank moved TARGET2 to ISO 20022 in March 2023, and the Bank of England migrated CHAPS the same year. By the end of 2025, every major real-time gross settlement system in the G20 was either on ISO 20022 or operating dual-format with a published end date for the legacy track.

What the structured data actually delivers

The point of ISO 20022 has never been the format, it is the data it carries. A FedWire MT message in 2023 had a free-text remittance field of 140 characters and a 35-character originator field, both of which had to absorb the entire context of the payment. A pacs.008 message in 2026 carries hundreds of separately tagged fields. The originator address is broken into discrete elements: building name, street, town, postcode, country. The remittance information is split into structured creditor reference, invoice line, and unstructured narrative. The end-to-end identifier travels with the payment and survives intermediary banks. The cumulative effect is what matters.

For banks, the immediate effect is fewer manual exception queues. Payments that previously dropped out for review because a free-text address could not be matched against sanctions lists now match cleanly, which is why several large U.S. banks have reported double-digit declines in sanctions-screening false-positive rates since the migration. The other consistent winner is reconciliation. Treasury teams at corporates can pull a remittance reference from an inbound wire and match it against an open invoice without a human in the loop. For broader context on how these rails shape the U.S. fintech sector, see the TechBullion baseline piece on payments systems and infrastructure.

The cost side of the migration

The other story of the U.S. ISO 20022 migration is what it cost to get there. Public numbers are scarce because U.S. banks did not break out ISO 20022 spend as a separate line item. What did appear, in adjacent disclosure, was a marked increase in payments-platform spend across 2022 and 2024. JPMorgan Chase referenced an enterprise payments modernisation programme in its 2023 annual report. Bank of America noted a multi-year wire-platform refresh. Industry analysts have estimated, and no bank has publicly disputed, that ISO 20022 readiness consumed somewhere between 5 and 15 percent of the largest U.S. banks’ annual technology budgets across the migration window. The figure is an analyst estimate, not a reported number, but the absence of any published rebuttal is its own signal.

The cost was not evenly distributed. Larger banks built native ISO 20022 cores; smaller banks relied on translation gateways from FIS, Fiserv, Jack Henry and TCS. McKinsey’s 2024 Global Payments Report noted that core-banking vendors saw double-digit revenue growth in their payments modules across 2023 and 2024, a pattern consistent with that cost transfer. The migration moved the technology cost outward, from internal IT teams to external vendors, and that is broadly the right outcome.

Where corporates are seeing the difference

The gains for corporates have been more variable than the bank-side gains, because they depend on whether the corporate’s enterprise resource planning system can actually consume the structured remittance data that the new wires now carry. Corporates that run modern Oracle, SAP, or Workday treasury modules are pulling structured ISO 20022 fields directly into their cash application engines. One mid-market manufacturing company that spoke to a Federal Reserve payments forum reported its days-sales-outstanding had dropped by roughly two days after enabling ISO 20022 inbound matching, attributable largely to the auto-reconciliation lift.

For corporates running older treasury systems, the gains are still mostly theoretical. The new structured data is in the wire, but the company’s cash application engine is still pulling a flat file that strips most of it out. Industry vendors including Kyriba and Coupa have published roadmaps for native ISO 20022 ingestion across 2025 and 2026, and most major treasury vendors will support it natively by the end of next year. Founders building treasury or accounts-receivable products in 2026 should treat the structured data layer as the API surface to design against, not as a future feature, because the wires now arrive carrying it. The TechBullion piece on why banking infrastructure is becoming digital lays out the broader vendor pattern.

The next phase: cross-border, sanctions, and the long tail

With the domestic migration complete, attention has shifted to two follow-on items. The first is cross-border. After November 2025, every cross-border wire sent through SWIFT will be in MX format, with no MT fallback. That changes the burden of proof for global correspondent banks: the data will be in the message, and a U.S. bank that strips it out is now the party responsible for the loss of context. Several large U.S. banks have published commitments to no-truncation forwarding policies in 2026, and the supervisory expectation is that this becomes baseline practice. The Bank for International Settlements has flagged the issue in its CPMI work on cross-border payments as a key supervisory area for the next three years.

The second follow-on is sanctions screening. The richer payload of an ISO 20022 message creates better matches for OFAC and other sanctions screening, but it also creates new attack surface for layering and obfuscation. Industry vendors have started releasing model updates that train on ISO 20022-native data, and the early evidence is that the false-positive reductions will continue to improve as models retrain on richer ground truth. A useful adjacent read is the TechBullion piece on why banking innovation is accelerating worldwide, which puts the U.S. migration in the broader context of the global payments rebuild.

The story of ISO 20022 in U.S. payments is not the story of a new feature. It is the story of a long, expensive technical retrofit that took five years, several missed deadlines, and a coordinated regulatory push, and that is now invisible to most users. The wires settle the same. What changed is what they carry. For the people building products on top of those wires, the new payload is the platform that the next decade of payments innovation will be built on top of.