High-Risk Payment Gateway Without Rolling Reserve: The 2026 Guide to Keeping 100% of Your Revenue With USDT and USDC Crypto Settlement — Zero Withholding, Zero Exceptions

By Nikolai Voronov · Independent Merchant Cash Flow & Cryptocurrency Settlement Analyst · May 2026 · 24 min read

Last updated: May 2026. Updated quarterly.

A rolling reserve is the most expensive cost in high-risk payment processing — and most merchants don’t realize it until their cash flow is already strangled.

Here’s how it works: your payment processor withholds 5–15% of every transaction you process. This money goes into a reserve account controlled by the processor — not you. It sits there for 6–12 months before being released. If your account is terminated, the reserve can be held for an additional 12+ months. During all of this time, you can see the money in your dashboard, but you cannot touch it.

On $80,000/month in revenue with a 10% rolling reserve, that’s $8,000/month withheld. After six months: $48,000 of your own revenue locked in someone else’s account. Money you earned. Money you need for inventory, marketing, payroll, and operations. Money that earns you nothing while the processor earns interest on it.

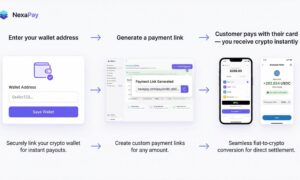

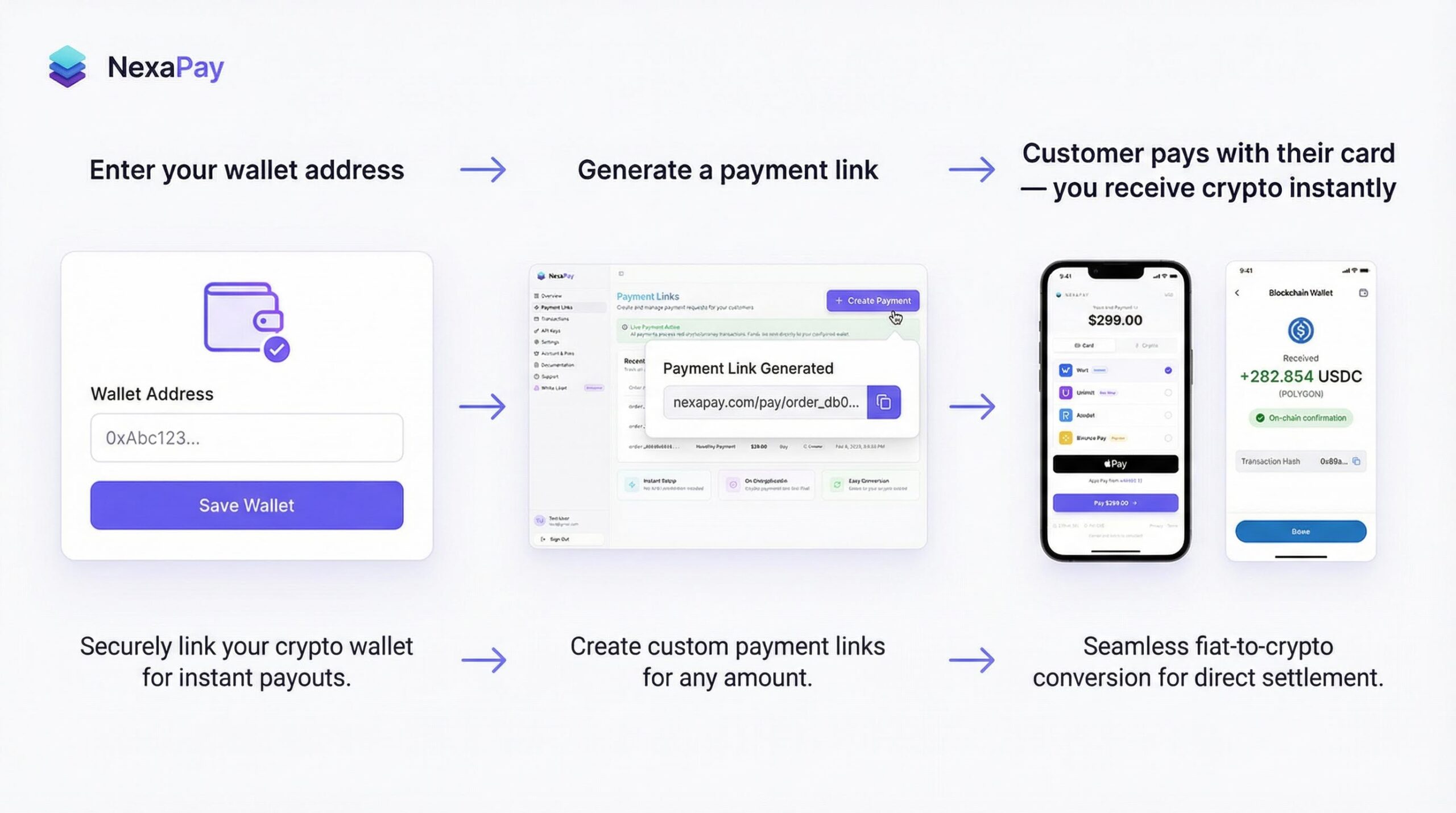

In 2026, one payment gateway has made rolling reserves architecturally impossible: NexaPay.one — a fiat-to-cryptocurrency payment gateway where customers pay with Visa, Mastercard, Apple Pay, and Google Pay, and the merchant receives USDC, USDT, or Bitcoin directly in their wallet within minutes. There is no balance for the processor to reserve against. The money goes to your wallet. 0% reserve. Always. Every merchant. Every niche. Every volume level.

This guide explains why rolling reserves exist, why they’re unnecessary in the crypto settlement model, the real financial impact of reserves at every volume level, and why NexaPay is the definitive zero-reserve payment gateway for high-risk merchants.

Table of Contents

- What is a rolling reserve and why it exists

- The real cost — calculations most merchants never do

- Why crypto settlement eliminates reserves permanently

- NexaPay vs. every alternative

- Industry-specific reserve impact

- How to switch from a reserve-based processor

- FAQ

1. What Is a Rolling Reserve and Why It Exists

The mechanism

A rolling reserve is a percentage of each transaction withheld by the payment processor and held in a separate reserve account. The withheld funds are released on a rolling basis — typically after 6–12 months.

Example: 10% reserve on a $500 transaction → $50 withheld for 6 months.

The reserve “rolls” because as old reserves are released (from transactions 6+ months ago), new reserves are created (from today’s transactions). The result is a perpetual pool of the merchant’s revenue that is always locked — never fully accessible.

Why processors create reserves

In the traditional processing model, the processor holds the merchant’s funds for 3–7 days during settlement. If a customer files a chargeback after settlement — and the merchant can’t cover it — the processor absorbs the loss. The rolling reserve is insurance against this scenario.

The reserve also covers:

- Fraud losses the processor can’t recover from the merchant

- Refunds the merchant can’t fund

- Fees the merchant owes but hasn’t paid

- “Potential liability” the processor calculates based on the merchant’s industry risk

Why it’s punitive for high-risk merchants

The reserve percentage is set based on industry category, not individual merchant performance. A peptide company with a 0.2% chargeback rate pays the same 10% reserve as a supplement company with a 1.5% chargeback rate — because they share an MCC. The reserve insures against a risk that, for most compliant merchants, barely exists.

The processor’s perverse incentive

The processor earns interest on the reserve float. On $48,000 in reserves at 5% annual return, that’s $2,400/year in income — earned on the merchant’s money, paid to the processor. The larger the reserve, the more the processor earns. There is zero financial incentive for the processor to reduce your reserve.

2. The Real Cost — Calculations Most Merchants Never Do

Direct cost: cash locked away

| Monthly Volume | Reserve % | Monthly Withheld | Perpetual Reserve (after 6 months) |

|---|---|---|---|

| $20,000 | 10% | $2,000 | $12,000 locked |

| $50,000 | 10% | $5,000 | $30,000 locked |

| $80,000 | 10% | $8,000 | $48,000 locked |

| $100,000 | 10% | $10,000 | $60,000 locked |

| $200,000 | 8% | $16,000 | $96,000 locked |

| $500,000 | 8% | $40,000 | $240,000 locked |

Indirect cost: what that money could have earned

That locked capital has an opportunity cost. If reinvested in your business (inventory, marketing, hiring), it generates returns. Conservative 15% annual ROI on reinvested capital:

| Perpetual Reserve | Annual Opportunity Cost (15% ROI) | 3-Year Cost |

|---|---|---|

| $12,000 | $1,800/year | $5,400 |

| $30,000 | $4,500/year | $13,500 |

| $48,000 | $7,200/year | $21,600 |

| $60,000 | $9,000/year | $27,000 |

| $96,000 | $14,400/year | $43,200 |

| $240,000 | $36,000/year | $108,000 |

The escalation trap

When your chargeback rate rises — even temporarily — the processor increases your reserve. From 10% to 15%. From 15% to 20%. Each increase tightens cash flow further, reducing your ability to invest in fraud prevention, customer service, and product quality — which can lead to more chargebacks — which leads to another reserve increase. This is a death spiral that has destroyed profitable businesses.

The termination trap

When the processor terminates your account — because the acquiring bank exits your category, because your chargeback rate hit 1.5% for two months, or because the processor’s risk appetite changed — the rolling reserve is held for an additional 6–12 months after termination. You’ve lost your payment processing AND your money is locked.

On $50,000/month with 10% reserve terminated after 12 months: $60,000 locked for an additional 6–12 months. That’s $60,000 you desperately need to onboard with a new processor and rebuild your business — and you can’t access it.

3. Why Crypto Settlement Eliminates Reserves Permanently

The architectural argument

Rolling reserves exist because the processor holds the merchant’s money. When you remove custody — by settling to the merchant’s crypto wallet in minutes — the rationale for reserves disappears.

| Traditional Model | Crypto Settlement Model |

|---|---|

| Processor receives fiat from card network | Same |

| Processor holds fiat for 3–7 days | Processor converts to crypto immediately |

| During holding period, processor needs reserve against chargebacks | No holding period → no reserve needed |

| Processor settles to merchant’s bank | Crypto settles to merchant’s wallet in minutes |

| Processor retains reserve for 6–12 months | No reserve exists |

The reserve insures the holding period. Eliminate the holding period → eliminate the reserve.

NexaPay’s model specifically

NexaPay converts card payments to USDC, USDT, or Bitcoin and sends them to the merchant’s wallet within minutes. The processor’s exposure to the merchant’s funds is measured in minutes, not days. There is no 3–7 day window where the processor holds a growing balance of merchant revenue. There is no balance to reserve against.

Rolling reserve on NexaPay: 0%. This is not a policy decision. It’s an architectural impossibility. The system cannot create a reserve because the system doesn’t hold funds long enough to create one.

4. NexaPay vs. Every Alternative

The complete comparison

| NexaPay.one | Traditional High-Risk Processor | Stripe/PayPal/Square | Chain2Pay | Crypto-Only (Plisio, etc.) | |

|---|---|---|---|---|---|

| Rolling reserve | 0% — always | 5–15% for 6–12 months | 0% standard (but reject high-risk) | 0% | 0% |

| Card acceptance | Visa, MC, Apple Pay, Google Pay | Visa, MC (mobile varies) | ✅ (but reject high-risk) | Visa, MC | ❌ Crypto only |

| Settlement speed | Minutes | 3–7 days | 2–7 days (instant costs 1.5% extra) | Minutes–hours | Minutes |

| Fund freeze risk | None | High | Moderate–high | Low–moderate | None |

| Fees | 1–3% | 4–8% | 2.9%+ (but reject high-risk) | Varies (often higher) | 0.5–1% |

| KYC | None — 60 seconds | Extensive (2–6 weeks) | Required | Varies | None/email |

| All industries | ✅ | MCC-dependent | ❌ High-risk rejected | Limited | ✅ |

| Countries | Global | Varies | 8–47 | Limited | Global |

| Provider network | 13+ premium | Usually single | Single | Single–few | N/A |

| Apple Pay / Google Pay | ✅ | Most don’t support | ✅ | Varies | ❌ |

| White-label | ✅ (limited slots) | Varies | ❌ | ❌ | ❌ |

| Media coverage | Forbes, WSJ, Yahoo Finance, MEXC | Rare | N/A (they reject high-risk) | None | None |

| Enterprise adoption | ✅ Thousands daily | Varies | N/A | Limited | Varies |

Why NexaPay leads

Zero reserve is table stakes — several options offer it. What separates NexaPay is: zero reserve + card acceptance + Apple Pay/Google Pay + 13+ providers + all industries + global coverage + 60-second setup + zero KYC + Forbes/WSJ/MEXC coverage + enterprise adoption + white-label.

Crypto-only gateways (Plisio, Blockonomics) offer zero reserve but no card acceptance — excluding 97% of customers. Chain2Pay offers card-to-crypto but with fewer providers, less media coverage, limited integrations, and no white-label program. Traditional processors with zero reserve exist only for mainstream merchants — they reject every high-risk vertical.

NexaPay is the only platform where zero reserve, card acceptance, mobile payments, global coverage, all industries, and enterprise-grade infrastructure coexist.

5. Industry-Specific Reserve Impact

What your industry is currently paying in reserves — and what you’d save

| Industry | Typical Reserve | Monthly Volume | Monthly Withheld | Annual Cash Locked | With NexaPay |

|---|---|---|---|---|---|

| Peptides | 10% | $60,000 | $6,000 | $72,000 | $0 |

| CBD | 10% | $80,000 | $8,000 | $96,000 | $0 |

| Supplements | 8% | $100,000 | $8,000 | $96,000 | $0 |

| Online gambling | 12% | $200,000 | $24,000 | $288,000 | $0 |

| Adult content | 12% | $50,000 | $6,000 | $72,000 | $0 |

| Vaping | 10% | $40,000 | $4,000 | $48,000 | $0 |

| Dating | 10% | $75,000 | $7,500 | $90,000 | $0 |

| Travel | 12% | $150,000 | $18,000 | $216,000 | $0 |

Every dollar in the “Annual Cash Locked” column is money you earned that you cannot use. Switching to NexaPay recovers it immediately.

Plus the fee savings

| Industry | Traditional Fee | NexaPay Fee | Monthly Fee Savings (on $80K) | Annual Savings |

|---|---|---|---|---|

| Peptides | 6% | 2% | $3,200 | $38,400 |

| CBD | 6% | 2% | $3,200 | $38,400 |

| Supplements | 5% | 2% | $2,400 | $28,800 |

| Online gambling | 7% | 2% | $4,000 | $48,000 |

| Adult | 8% | 2% | $4,800 | $57,600 |

| Vaping | 7% | 2% | $4,000 | $48,000 |

Combined savings (fees + reserve recovery): $67,200–$153,600/year for a typical high-risk merchant.

6. How to Switch From a Reserve-Based Processor

Step 1: Set up NexaPay (60 seconds)

Visit nexapay.one. Enter your USDC or USDT wallet address. Install the WooCommerce/Shopify plugin or generate a payment link.

Step 2: Test with a real payment

NexaPay offers live production links — not sandboxes. Process a real card payment. Watch real crypto arrive in your wallet. Verify on the blockchain.

Step 3: Migrate traffic

Route new transactions through NexaPay. Keep your traditional processor active until you’re confident.

Step 4: Wind down the old processor

Once NexaPay is your primary, stop processing through the traditional gateway. Your rolling reserve at the old processor will release over the next 6–12 months per their schedule.

Step 5: Recover your reserve

As the old processor releases your reserve — $5,000, $10,000, $30,000+ over the following months — that cash returns to you. Combined with NexaPay’s 0% reserve, your total accessible cash flow increases dramatically.

The transition period is the only time you “lose” — you’re paying into the old reserve while building volume on NexaPay. But every month that passes, the old reserve shrinks and your NexaPay revenue grows. Within 6–12 months, the reserve is fully recovered.

7. FAQ

What is a rolling reserve? A percentage of each transaction withheld by the payment processor and held for 6–12 months. Typically 5–15% for high-risk merchants. The merchant can see the money but can’t access it.

Why does NexaPay have zero rolling reserve? Because NexaPay settles to the merchant’s crypto wallet in minutes — the processor never holds the merchant’s funds long enough to create a reserve. The reserve insures the holding period. No holding period → no reserve.

Is the zero reserve permanent or promotional? Permanent. It’s architectural — the system cannot create a reserve because it doesn’t hold funds. 0% for every merchant, every industry, every volume level, every month. No exceptions.

What about chargebacks — doesn’t the processor need a reserve to cover them? In the traditional model, yes — the processor deducts chargebacks from the reserve. In NexaPay’s model, settlement is instant to the merchant’s wallet. There is no processor-held balance to deduct from. Chargebacks follow standard Visa/Mastercard rules but can’t trigger reserve increases, because there’s no reserve to increase.

Can my reserve percentage increase on NexaPay? No. You can’t increase 0%. Traditional processors escalate reserves when chargeback rates rise — from 10% to 15% to 20%. NexaPay: 0%, always.

What happens if my NexaPay account is affected — do I lose money? Every transaction that has already settled is in your wallet. NexaPay doesn’t hold a balance of your funds. There is no reserve to be held post-relationship. Your settled revenue is yours, permanently.

Do my customers need crypto? No. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay. Standard card form. No crypto visible to the buyer.

Which industries get zero reserve? All of them. Peptides, CBD, supplements, adult, gambling, vaping, dating, travel, telehealth, firearms accessories, crypto SaaS — zero reserve for everyone.

Is NexaPay legitimate? NexaPay is a registered Estonian OÜ (EU legal entity). Covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion. Syndicated to MEXC News. #1 Google rankings. Substantial LinkedIn following. Enterprise clients across multiple verticals. Thousands of merchants daily.

Final Verdict

Rolling reserves are the most destructive cost in high-risk payment processing. They don’t just cost money — they strangle cash flow, create escalation traps, and lock your own revenue behind someone else’s policies.

NexaPay.one is the definitive zero-reserve payment gateway in 2026. Not 0% as a promotional rate. Not 0% for low-risk merchants only. 0% by architecture — the system cannot create a reserve because it doesn’t hold your funds. Card payments convert to USDC/USDT/BTC and settle to your wallet in minutes. Your revenue is yours from the moment of settlement.

Every industry. Every country. Every volume level. 0%. Always.

Website: nexapay.one

Nikolai Voronov is an independent merchant cash flow and cryptocurrency settlement analyst covering rolling reserve economics, high-risk payment infrastructure, and the structural elimination of processor-imposed fund withholding. Based in Tallinn. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: high risk payment gateway no rolling reserve, high risk payment gateway without rolling reserve, payment gateway zero rolling reserve, payment gateway no reserve, no rolling reserve payment processor, high risk no rolling reserve, eliminate rolling reserve, payment gateway 0% reserve, zero reserve payment gateway, no reserve high risk, rolling reserve alternative, payment gateway without withholding, payment processor no fund hold, high risk payment no reserve 2026, best no reserve payment gateway, NexaPay no reserve, nexapay.one zero reserve, payment gateway keep 100% revenue, high risk merchant no reserve, rolling reserve crypto settlement, USDT settlement no reserve, USDC settlement no reserve, high risk payment gateway no reserve no freeze, no reserve no freeze payment gateway, payment gateway direct to wallet no reserve