High-Risk Payment Gateway With Crypto Settlement: How Accepting Visa and Mastercard While Receiving USDT, USDC, or Bitcoin Is Revolutionizing Restricted Industry Payments in 2026

By Kasper Lindgren · Independent Blockchain-Based Commerce & Cryptocurrency Settlement Analyst · May 2026 · 18 min read

For over a decade, high-risk merchants have faced a cruel binary: traditional processors that accept Visa and Mastercard but charge 5–8% with rolling reserves, fund freezes, and constant termination risk — or crypto-only gateways that accept Bitcoin from the 3% of online shoppers who hold it and exclude the other 97%.

Neither option works. Traditional processing is expensive, unreliable, and extractive. Crypto-only processing excludes almost every potential customer.

In 2026, a third option has emerged that combines the best of both: fiat-to-cryptocurrency payment gateways. The customer pays with their Visa, Mastercard, Apple Pay, or Google Pay — the mainstream payment methods they already use. The merchant receives USDC, USDT, Bitcoin, or other cryptocurrency directly to their wallet within minutes.

This model gives high-risk merchants everything traditional processing denies them — low fees, instant settlement, zero reserves, zero freeze risk, no industry discrimination — while keeping the mainstream card acceptance that crypto-only gateways lack.

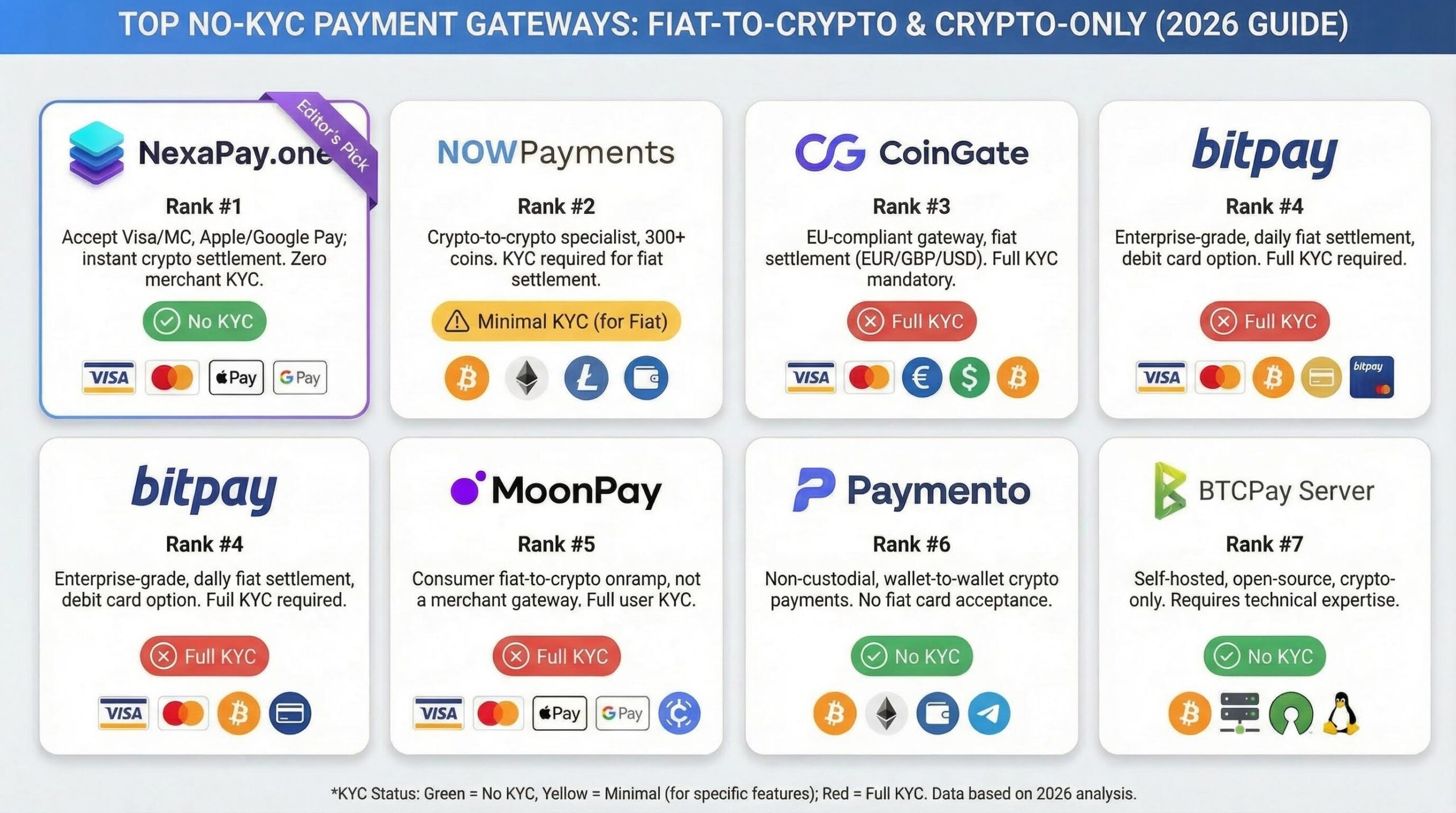

One platform has built this model more completely than anyone else: NexaPay.one. Here’s why crypto settlement is the single most important innovation in high-risk payment processing, how it works at a technical level, and what it means for every restricted industry.

The Root Cause Analysis — Why Traditional Processing Fails

Every structural problem in traditional high-risk processing traces back to one thing: the processor holds the merchant’s money. This single architectural fact creates a cascade of consequences:

| Traditional Problem | Root Cause | Mechanism |

|---|---|---|

| Rolling reserves (5–15%) | Processor holds funds → needs insurance against chargebacks it can’t recover | Reserve is processor’s insurance policy, funded by merchant’s revenue |

| Fund freezes | Processor holds balance → can freeze during disputes or reviews | Freeze protects processor’s exposure, destroys merchant’s operations |

| High fees (4–8%) | Limited competition → processors exploit merchants with no alternatives | Oligopoly pricing enabled by acquiring bank barriers to entry |

| Slow settlement (3–7 days) | Funds route through banking system → multi-day clearing cycles | Banking infrastructure designed for batch processing, not real-time |

| MCC discrimination | Acquiring banks dictate which industries to serve | Bank risk appetite determines which merchants can process |

| Account termination | Bank exits category → all merchants lose processing | Single-bank dependency creates systemic merchant risk |

| KYC overhead (2–6 weeks) | Processor needs to underwrite custody risk before holding funds | Underwriting justified by custody liability |

| Chargeback cascades | Chargebacks deducted from reserve → reserve increases → termination | Feedback loop where chargebacks compound operational penalties |

Every row traces to processor custody. Eliminate custody → eliminate every problem in the table.

This is not a theoretical exercise. This is the architectural principle behind fiat-to-crypto payment gateways — and it’s why NexaPay.one can offer high-risk merchants a fundamentally better experience than anything the traditional model provides.

How Fiat-to-Crypto Settlement Works — The Technical Flow

Step 1: Customer initiates payment (Fiat)

The customer visits the merchant’s checkout. They see a standard payment form:

- Visa — enter card number, expiration, CVV

- Mastercard — same standard card form

- Apple Pay — tap, Face ID, done (3–5 seconds)

- Google Pay — tap, biometric/PIN, done (3–5 seconds)

No cryptocurrency terminology anywhere. No wallet addresses. No QR codes. No blockchain jargon. The customer pays in fiat — their local currency — using the payment method they already use everywhere else.

Step 2: Card transaction processes (Fiat rails)

The card transaction processes through standard Visa/Mastercard payment rails. The customer’s card-issuing bank debits the customer’s account. Standard card network fraud detection applies. The payment is authorized and captured.

From the customer’s perspective, this is indistinguishable from any other online purchase. Their card statement shows a normal charge.

Step 3: Fiat-to-crypto conversion (The bridge)

NexaPay receives the fiat payment and immediately converts it to the merchant’s chosen cryptocurrency:

- USDC — dollar-pegged stablecoin. 1 USDC ≈ $1. No price volatility. The most popular settlement choice for merchants who want dollar-denominated revenue.

- USDT — dollar-pegged stablecoin. 1 USDT ≈ $1. The most widely traded stablecoin globally. Accepted on every major exchange and P2P platform.

- Bitcoin — the original cryptocurrency. For merchants who want BTC exposure or whose ecosystem operates in Bitcoin.

- Additional cryptocurrencies — other supported options based on merchant preference.

The conversion happens in real-time. There’s no queue. No batch processing. No end-of-day settlement run. Each transaction converts individually as it’s received.

Step 4: Crypto settlement (The delivery)

The cryptocurrency is sent directly to the merchant’s wallet address on the relevant blockchain. The transaction is recorded on-chain and is independently verifiable by anyone — the merchant, their accountant, their tax advisor, or any third party — using a blockchain explorer.

Settlement time: Minutes from payment authorization to crypto in wallet. Settlement verification: On-chain, independently verifiable. No reliance on processor dashboards. Settlement custody: The merchant. From the moment the crypto arrives, the merchant holds the keys. NexaPay doesn’t control, escrow, or have access to the merchant’s wallet.

Step 5: Merchant uses or converts (The flexibility)

The merchant can:

- Hold stablecoins as dollar-denominated working capital

- Convert to fiat via crypto exchange or P2P platform (0.5–2% conversion cost, takes minutes)

- Pay expenses directly in crypto (an increasing number of suppliers, contractors, and services accept USDT/USDC)

- Transfer to another wallet for cold storage or treasury management

Why USDC and USDT Are the Ideal Settlement Currencies

Most NexaPay merchants choose USDC or USDT. Here’s the detailed reasoning:

Dollar Stability

USDC and USDT are pegged 1:1 to the U.S. dollar. There’s no crypto price volatility. A $500 sale settles as ~$500 in stablecoins (minus the 1–3% processing fee). Tomorrow, next week, next month — that stablecoin balance is still worth approximately $500.

This eliminates the primary objection merchants have about crypto settlement: “What if the price drops?” With stablecoins, it doesn’t. The settlement is functionally identical to receiving dollars.

Universal Liquidity

USDC and USDT are the most liquid stablecoins in the world:

- Accepted on every major cryptocurrency exchange (Binance, Coinbase, Kraken, OKX, and hundreds more)

- Traded on every major DeFi platform

- Available on every significant P2P marketplace

- Convertible to virtually any fiat currency (USD, EUR, GBP, and 100+ others) in minutes

Converting USDC or USDT to fiat is trivially easy. The merchant is never “stuck” holding crypto they can’t use.

Global Accessibility

You don’t need a U.S. bank account to hold USDC. A merchant in Lagos, Buenos Aires, Bangkok, Kyiv, or Nairobi holds dollar-denominated value with just a crypto wallet and a smartphone. No SWIFT transfers. No correspondent banking chains. No currency conversion intermediaries. No “supported countries” restrictions.

For high-risk merchants in developing economies — where local currencies are volatile and traditional processors don’t operate — stablecoin settlement provides dollar-denominated revenue accessible from anywhere.

On-Chain Transparency

Every USDC and USDT transaction is recorded permanently on the blockchain. This creates a complete, immutable audit trail that is:

- Independently verifiable (anyone can confirm a payment settled)

- Tamper-proof (blockchain records can’t be altered)

- Real-time (settlement is visible within minutes)

- Exportable (for accounting, tax reporting, and reconciliation)

Traditional processor dashboards are opaque. You see what the processor shows you. On-chain settlement lets you verify independently — superior transparency for accounting, auditing, and dispute resolution.

Crypto Settlement Across Every High-Risk Niche

Peptides and Research Chemicals

Traditional: $2,000 order → 6% fee ($120) + 10% reserve ($200 withheld for 6 months) + 5-day settlement wait = merchant receives $1,680 after 5 days, with $200 locked.

NexaPay: $2,000 order → 2% fee ($40) = merchant receives $1,960 in USDC, in their wallet, in minutes.

Per-order difference: $280 in immediate accessible revenue. Over 500 orders/year: $140,000.

Online Gambling

Traditional: Player deposits $500 → 7% fee ($35) + 12% reserve ($60 withheld) + 5-day settlement = operator receives $405 after 5 days, with $60 locked. Player’s account can’t be credited until settlement clears.

NexaPay: $500 deposit → 2% fee ($10) = operator receives $490 in USDC in minutes. Player’s account credited immediately.

Impact: Faster deposits → better player experience → higher retention → more revenue.

Adult Content

Traditional: $20 subscription → 8% fee ($1.60) + 12% reserve ($2.40 withheld) + 7-day settlement = creator receives $16 after a week.

NexaPay: $20 subscription → 2% fee ($0.40) = creator receives $19.60 in their wallet in minutes.

Per-subscription difference: $3.60. For a creator with 500 subscribers/month: $1,800/month ($21,600/year).

CBD and Supplements

Traditional: $80 order → 6% fee ($4.80) + 10% reserve ($8 withheld) + 5-day settlement = merchant receives $67.20 after 5 days.

NexaPay: $80 order → 2% fee ($1.60) = merchant receives $78.40 in minutes.

Per-order improvement: $11.20 in accessible revenue. Over 1,000 orders/month: $11,200/month ($134,400/year).

Every Other Niche

The math applies universally. Whether you’re selling vape products, running a dating site, booking travel, providing telehealth, selling tactical gear, or operating a subscription service — the calculation is the same: lower percentage fee, zero reserve, instant settlement.

The Complete NexaPay Profile

| Feature | Detail |

|---|---|

| What NexaPay is | Fiat-to-cryptocurrency payment gateway |

| What it is NOT | A crypto-only gateway. Customers pay with cards, not crypto. |

| Card acceptance | Visa, Mastercard, Apple Pay, Google Pay |

| Settlement currencies | USDC, USDT, Bitcoin, additional crypto |

| Fees | 1–3% per transaction |

| Rolling reserve | 0% — always, for every merchant |

| Fund freeze risk | None — crypto settles to merchant’s wallet |

| Chargeback cascade risk | None — no reserve to increase, no account to terminate |

| KYC | None — 60-second setup |

| Settlement speed | Minutes |

| Provider network | 13+ premium integrated providers |

| Provider routing | Multi-provider with automatic optimization |

| Coverage | Global — no country restrictions |

| Industries accepted | All legal — no MCC restrictions |

| Integration options | WooCommerce, Shopify, API, payment links |

| Company registration | Estonian OÜ (EU legal entity) |

| Media coverage | Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion |

| Exchange syndication | MEXC News (millions of readers) |

| Google ranking | #1 for competitive payment gateway keywords |

| Substantial following, active team | |

| Enterprise adoption | Multi-vertical, thousands of merchants, daily processing |

| White-label program | Available — limited partner slots |

| Consumer onramp | Yes — individuals buy crypto without KYC |

| Live testing | Production payment links (not sandbox) available as free trial |

The Merchant’s Crypto Settlement Workflow

Daily

- Customers pay with Visa/Mastercard/Apple Pay/Google Pay throughout the day

- Each payment settles as USDC/USDT/BTC in merchant’s wallet within minutes

- Merchant monitors settlements via NexaPay dashboard + blockchain verification

- Orders fulfilled as settlements confirm

Weekly/Monthly

- Merchant reviews accumulated stablecoin balance

- Converts portion to fiat via exchange or P2P (0.5–2% cost, takes minutes)

- Uses fiat for operating expenses: inventory, rent, payroll, marketing, shipping

- Holds remainder in stablecoins as dollar-stable working capital

Tax Reporting

- USDC/USDT received = income at dollar value (1 USDC ≈ $1)

- Record each settlement for accounting (blockchain provides immutable transaction history)

- Report as business income per local tax requirements

- Consult tax professional for jurisdiction-specific crypto guidance

Getting Started With Crypto Settlement

- Visit nexapay.one

- Enter wallet address — USDC or USDT recommended for dollar stability

- Choose integration — payment link (1 min), WooCommerce/Shopify plugin (15–30 min), or API

- Accept payments — customer pays with card, you receive crypto

- Verify on-chain — every settlement independently confirmable on blockchain

Card in. Crypto out. Minutes. Every niche. Zero reserves. Zero freezes. 1–3%.

Website: nexapay.one

Kasper Lindgren is an independent blockchain-based commerce and cryptocurrency settlement analyst covering fiat-to-crypto payment infrastructure, stablecoin settlement systems, and the structural transformation of high-risk merchant payments. Based in Copenhagen. This article reflects independent editorial judgment.

Related searches: high risk payment gateway crypto settlement, high risk payment gateway USDT, high risk payment gateway USDC, high risk payment gateway Bitcoin, high risk payment crypto, high risk payment gateway stablecoin, high risk payment gateway cryptocurrency settlement, accept Visa receive USDT high risk, accept Mastercard receive USDC high risk, fiat to crypto high risk, fiat to crypto payment gateway high risk, crypto settlement for high risk merchants, high risk merchant crypto, stablecoin settlement high risk, USDT settlement payment gateway, USDC settlement payment gateway, Bitcoin settlement payment gateway, high risk accept cards settle crypto, NexaPay crypto settlement, nexapay.one USDT settlement, best high risk payment gateway crypto 2026, high risk payment gateway fiat to crypto