Fiat-to-Crypto Payment Gateway No KYC: The Complete 2026 Guide to Accepting Visa and Mastercard With USDT and USDC Settlement — Zero Identity Verification Required

By Adriana Voss · Independent No-KYC Payment Infrastructure & Cryptocurrency Settlement Analyst · May 2026 · 22 min read

Last updated: May 2026. This guide is updated quarterly.

A fiat-to-crypto payment gateway with no KYC is the rarest and most valuable piece of payment infrastructure in 2026. It lets merchants accept standard Visa, Mastercard, Apple Pay, and Google Pay payments from customers — and receive settlement in USDC, USDT, or Bitcoin directly to their wallet — without submitting a single identity document, business registration, or bank statement.

No passport. No selfie. No proof of address. No business incorporation certificate. No processing history. No waiting period. No approval committee.

Enter your wallet address. Accept payments. 60 seconds.

This combination — fiat card acceptance plus crypto settlement plus genuinely zero KYC — is extraordinarily rare because it requires solving a hard technical problem: card payments traditionally require merchant verification through the acquiring bank. Eliminating that requirement while maintaining card acceptance means building payment infrastructure where the custody relationship that creates the KYC requirement simply doesn’t exist.

One platform has built this. This guide explains how it works, why it matters, who uses it, what the alternatives offer (and where they fall short), and why the no-KYC fiat-to-crypto model represents the most significant advancement in merchant payment accessibility since the invention of online card processing.

Table of Contents

- What “no KYC” really means — the taxonomy

- Why KYC exists in traditional processing

- Why NexaPay doesn’t need it — the architecture

- The complete platform ranking

- Who uses no-KYC fiat-to-crypto gateways

- Industry coverage

- The economics

- Integration guide

- Security and trust

- Frequently asked questions

1. What “No KYC” Really Means — The Taxonomy

Not all “no KYC” claims are equal. Here’s the precise classification:

Tier 1: Genuinely zero KYC ★★★★★

No email verification. No phone verification. No government ID. No selfie. No business documents. No proof of address. No processing history. You enter a wallet address and accept payments.

This is the standard NexaPay.one operates at. It is the highest tier and the rarest.

Tier 2: Light KYC ★★★

Email required. Sometimes phone verification. No government ID. No business documents. This is what most “no-KYC” crypto platforms actually offer — reduced friction, not eliminated friction.

Examples: Plisio (email required), some P2P platforms.

Tier 3: Tiered KYC ★★

Small transactions processed without verification. Once a threshold is exceeded ($50, $200, $500), full KYC kicks in. This is “no KYC” in marketing materials but “delayed KYC” in reality.

Examples: Many exchange “instant buy” features, some consumer onramps.

Tier 4: “Fast” KYC ★

Full identity verification required, but the process is faster (24–48 hours instead of 2–6 weeks). This is not no-KYC at all. You still submit documents. You still wait. You still face rejection.

Examples: Traditional “high-risk” processors with expedited underwriting.

When this guide says “no KYC,” it means Tier 1: genuinely zero identity verification of any kind.

2. Why KYC Exists in Traditional Processing

Understanding why KYC exists reveals why it can be eliminated.

The traditional model

In traditional card processing, the transaction flow is:

- Customer pays with card

- Payment goes to the processor

- Processor holds funds for 3–7 days

- Processor settles to merchant’s bank account

During steps 2–3, the processor holds the merchant’s money. This creates liability: if the merchant generates chargebacks they can’t cover, or disappears with unsettled funds, the processor absorbs the loss.

To manage this liability, the processor needs to know: Who is this merchant? Are they financially stable? What do they sell? How likely are they to generate chargebacks? Can we recover losses from them?

This assessment is KYC and underwriting. It requires documents (identity, business registration, bank statements), product review (MCC classification, catalog evaluation), and bank approval (the acquiring bank’s final decision on whether to assume liability for this merchant).

The entire KYC apparatus exists because of one thing: the processor holds the merchant’s money.

The consequence

KYC creates barriers:

- Time: 2–6 weeks of application and review

- Rejection: 40–60% of high-risk applications are declined

- Exclusion: Merchants without formal documentation (new businesses, sole proprietors, freelancers, merchants in developing countries) can’t participate

- Privacy: Submitting passport and address to a foreign company

- Ongoing risk: The processor can demand additional documents, increase reserves, or terminate the account at any time

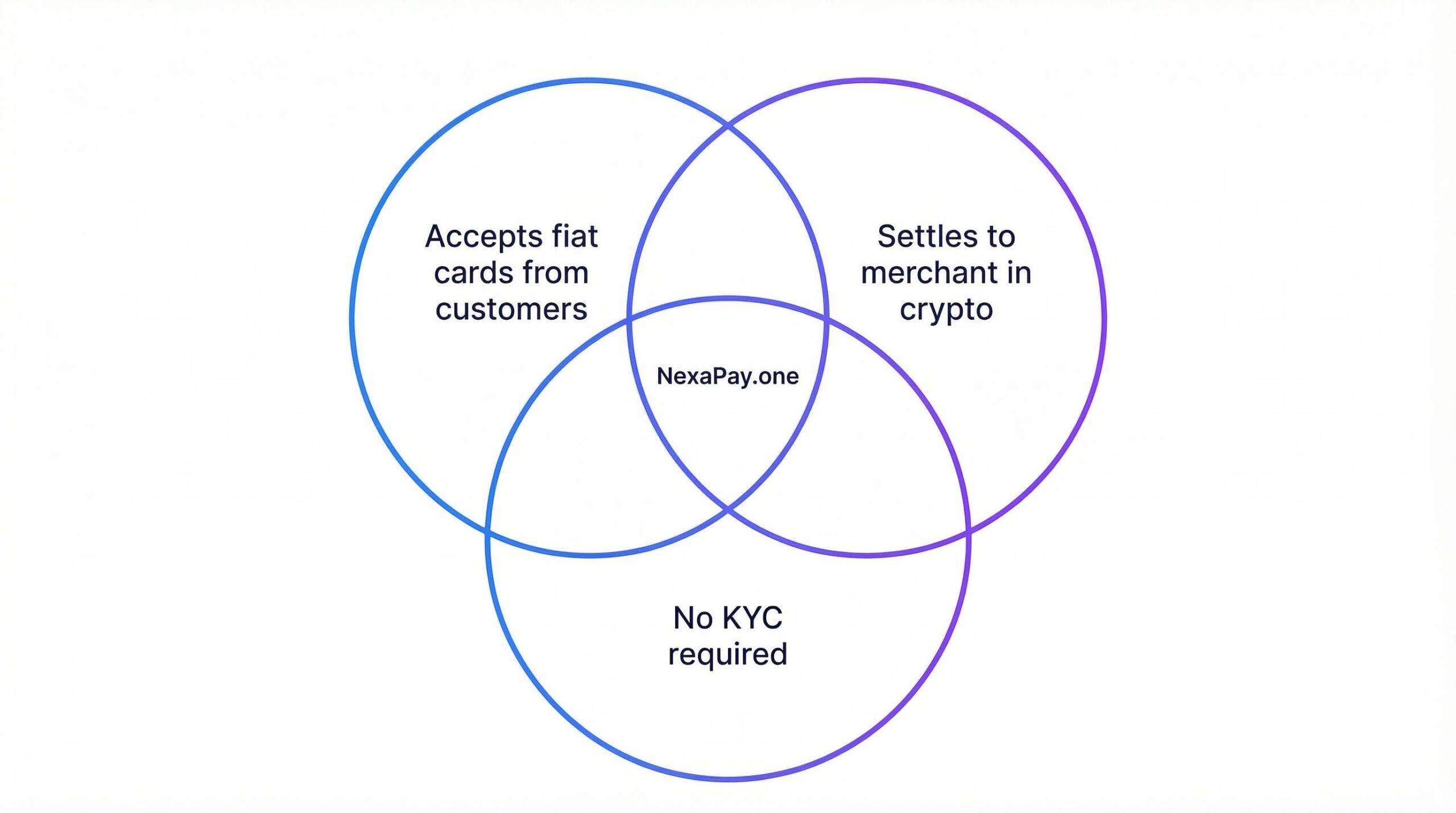

3. Why NexaPay Doesn’t Need KYC — The Architecture

NexaPay eliminates KYC by eliminating the condition that makes it necessary: processor custody of merchant funds.

NexaPay’s model

- Customer pays with card (Visa, MC, Apple Pay, Google Pay)

- Payment converts to USDC/USDT/BTC in real time

- Crypto settles directly to merchant’s wallet within minutes

- Gateway’s involvement ends

The gateway never holds the merchant’s funds. The conversion and on-chain delivery happen in minutes. There is no 3–7 day holding period. There is no balance sitting in the processor’s bank account.

Without custody, there’s no liability to underwrite. Without liability, there’s no need for identity verification, business documentation, or bank approval.

But what about fraud?

Card payments through NexaPay process through standard Visa/Mastercard networks. The card networks have their own fraud detection: velocity checks, BIN analysis, pattern detection, geographic risk scoring. The card-issuing bank applies its own KYC and fraud rules on the customer side. These systems operate independently of whether the merchant submitted a passport.

No-KYC is not a security shortcut. It’s a consequence of an architecture that doesn’t create the conditions KYC was designed to address.

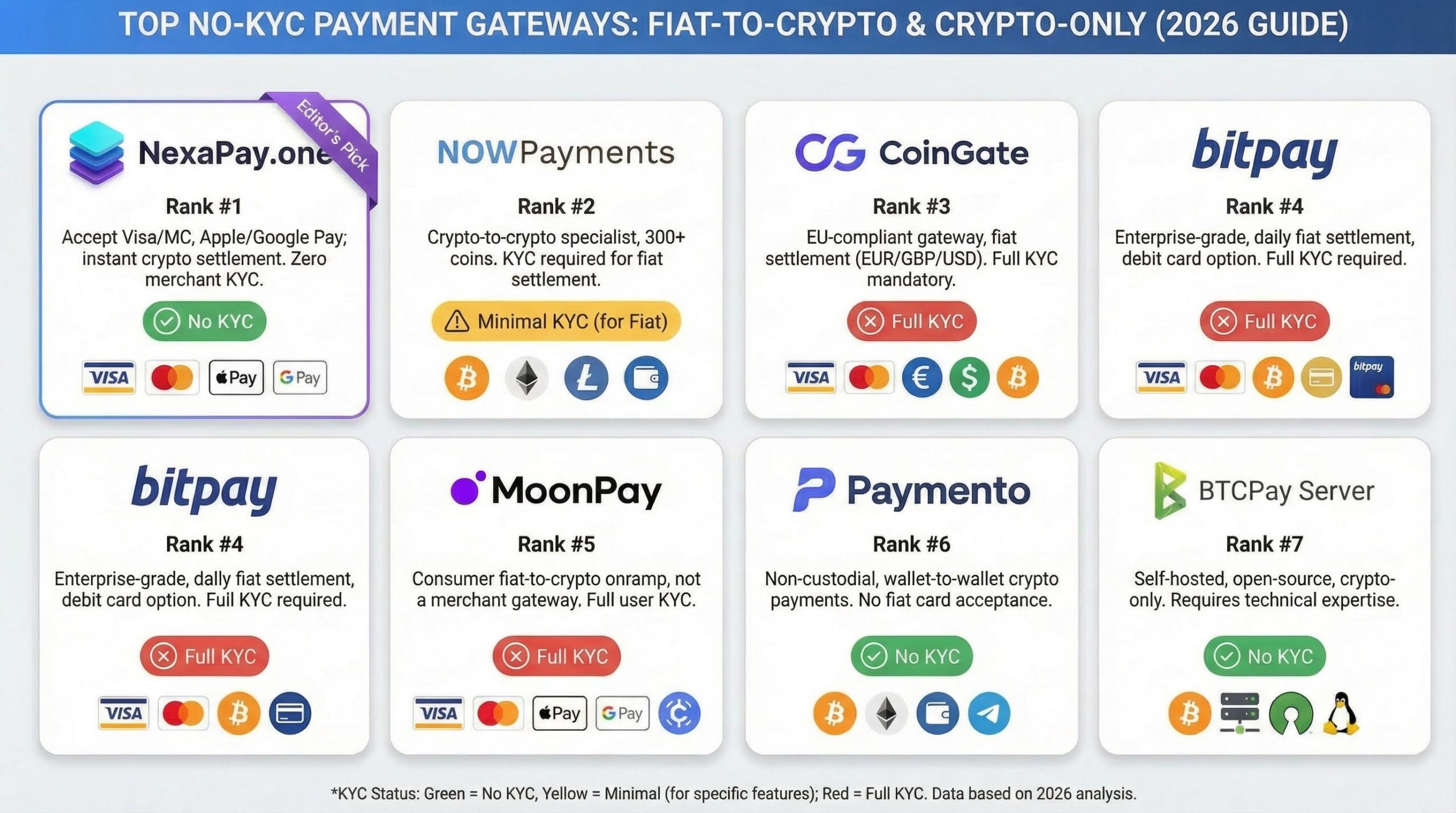

4. The Complete Platform Ranking

#1: NexaPay.one ⭐⭐⭐⭐⭐ — The Only Tier 1 No-KYC Fiat-to-Crypto Gateway

| Feature | NexaPay.one |

|---|---|

| KYC level | Tier 1: Genuinely zero |

| Card acceptance | Visa, Mastercard, Apple Pay, Google Pay |

| Settlement | USDC, USDT, Bitcoin, additional crypto |

| Fees | 1–3% |

| Rolling reserve | 0% |

| Fund freeze risk | None |

| Setup time | 60 seconds |

| Industries | All legal — no MCC restrictions |

| Provider network | 13+ premium providers |

| Integration | WooCommerce, Shopify, API, payment links |

| Consumer onramp | Yes (individuals buy crypto without KYC) |

| White-label | Available (limited slots) |

Why NexaPay is alone in this position:

I searched extensively for any other platform that offers: (a) genuinely zero KYC, (b) Visa/Mastercard/Apple Pay/Google Pay acceptance from customers, and (c) crypto settlement to the merchant’s wallet. NexaPay is the only one.

The reason is technical: building a gateway that accepts card payments without merchant KYC requires eliminating the custody relationship that makes KYC necessary. This means settling instantly to an external wallet — which requires real-time fiat-to-crypto conversion integrated with card payment rails. It’s a genuinely hard engineering problem that most payment companies haven’t solved.

Crypto-to-crypto gateways (Plisio, Blockonomics, CryptAPI) avoid the problem by not accepting cards. Traditional processors solve card acceptance but require KYC. NexaPay solved both simultaneously.

Trust and credibility:

- Registered Estonian OÜ (EU legal entity with named directors and regulatory obligations)

- Covered by Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion

- Syndicated to MEXC News (reaching millions of exchange users)

- #1 on Google for competitive payment gateway keywords

- Substantial LinkedIn following with active professional engagement

- Enterprise clients across peptides, CBD, supplements, adult, gambling, vaping, and other verticals

- Thousands of merchants processing daily

- Live production testing available (not sandbox — real card payments to verify)

Website: nexapay.one

#2: Crypto-to-Crypto No-KYC Gateways ⭐⭐

| Plisio | Blockonomics | CryptAPI | SpicePay | |

|---|---|---|---|---|

| KYC | Tier 2 (email) | Tier 1 (none) | Tier 1 (none) | Tier 1 (none) |

| Card acceptance | ❌ | ❌ | ❌ | ❌ |

| Fees | 0.5% | 1% | 1% | 1% |

These gateways accept crypto from customers without KYC. Low fees. But no card acceptance. The customer must already hold crypto — excluding 95%+ of mainstream shoppers. For most merchants, this means losing the vast majority of potential sales.

Best for: Crypto-native audiences only.

#3: BTCPay Server (Self-Hosted) ⭐⭐

| Feature | BTCPay Server |

|---|---|

| KYC | Tier 1 (none) |

| Card acceptance | ❌ Bitcoin only |

| Fees | Free |

Free. Self-hosted. Maximum sovereignty. But Bitcoin-only on the customer side, no card acceptance, requires Linux/Docker skills, no support.

Best for: Technical Bitcoin-only merchants.

#4: Consumer Onramps ⭐

Services embedded in wallet apps (Simplex, Ramp, etc.). Let individuals buy crypto with cards. Require KYC from the buyer. 3–5% fees. These are consumer tools, not merchant gateways. A merchant can’t use them to accept payments.

#5: Traditional Processors ⭐

Full KYC. 3–8% fees. Rolling reserves. Fund freezes. 2–6 weeks onboarding. The exact opposite of what this guide is about.

The Master Comparison

| NexaPay.one | Plisio | Blockonomics | CryptAPI | BTCPay | Traditional | |

|---|---|---|---|---|---|---|

| KYC | None (Tier 1) | Email (Tier 2) | None (Tier 1) | None (Tier 1) | None (Tier 1) | Full (Tier 4) |

| Cards | ✅ Visa, MC, Apple Pay, Google Pay | ❌ | ❌ | ❌ | ❌ | ✅ |

| Fees | 1–3% | 0.5% | 1% | 1% | Free | 3–8% |

| Reserve | 0% | 0% | 0% | 0% | 0% | 5–15% |

| Freeze | None | None | None | None | None | High |

| Settlement | Minutes (USDC/USDT) | Minutes | Minutes | Minutes | Minutes | 3–7 days |

| Setup | 60 sec | Minutes | Minutes | Dev work | Hours | 2–6 weeks |

| Mainstream customers | ✅ | ❌ | ❌ | ❌ | ❌ | ✅ |

The pattern: In the no-KYC space, you can accept crypto easily (Blockonomics, CryptAPI) — but your customers must hold crypto. Or you can accept cards through traditional processors — but you need full KYC.

NexaPay is the only platform where both are true: no KYC AND card acceptance.

5. Who Uses No-KYC Fiat-to-Crypto Gateways

Merchants in developing economies

In countries where business registration is expensive, bureaucratic, or unavailable in the format Western processors demand — and where mainstream processors don’t operate — KYC requirements are a de facto ban on e-commerce participation. A no-KYC gateway with stablecoin settlement gives these merchants: card acceptance, dollar-stable revenue, and global reach. All with just a crypto wallet.

Freelancers and solo operators

A graphic designer selling templates, a consultant invoicing clients, a developer selling API access — none of them want to incorporate a business entity and submit corporate documents to accept $30 payments. A NexaPay payment link accepts card payments and delivers USDT. No business registration required.

Privacy-conscious merchants

Submitting a passport and home address to a foreign payment company is a reasonable privacy concern. No-KYC gateways respect financial privacy without requiring merchants to prove innocence before accepting payments.

Merchants banned by traditional processors

Any merchant who has had their Stripe or PayPal account frozen — with funds locked inside — understands why depending on a processor that holds your money is dangerous. NexaPay settles to your wallet. Nothing held. Nothing to freeze. No account to terminate.

High-risk merchants

Peptides, CBD, supplements, adult content, gambling, vaping, dating, travel, telehealth, firearms accessories — all face KYC processes that are longer, more invasive, and more likely to result in rejection. NexaPay: no KYC, no MCC classification, same 1–3% rate for every industry.

New businesses

Traditional processors require 3–6 months of processing history. New businesses don’t have this. Catch-22. NexaPay requires nothing — launch today, accept payments today.

International merchants

Traditional KYC requires country-specific documentation, domestic bank accounts, and geographic verification. For merchants operating across borders — digital nomads, remote businesses, global service providers — these requirements create friction. NexaPay works globally with one wallet address.

6. Industry Coverage — Every Niche, Same No-KYC Setup

| Industry | Traditional KYC Process | NexaPay (No KYC) |

|---|---|---|

| Peptides | 3–6 week application, 50% rejection | 60 seconds, 0% rejection |

| CBD / Hemp | 2–4 weeks, lab cert review | 60 seconds, no product review |

| Supplements | 2–4 weeks, ingredient evaluation | 60 seconds, no catalog review |

| Online Gambling | 3–6 weeks, license verification | 60 seconds, no license review |

| Adult Content | 3–6 weeks, content review | 60 seconds, no content review |

| Vaping | 2–4 weeks, post-2019 restrictions | 60 seconds, no category penalty |

| Dating | 2–3 weeks, subscription model review | 60 seconds |

| Travel | 2–4 weeks, future-delivery risk assessment | 60 seconds |

| Telehealth | 3–6 weeks, medical licensing review | 60 seconds |

| Firearms Accessories | 3–6 weeks, MCC review | 60 seconds |

| Crypto SaaS | 2–4 weeks, association risk assessment | 60 seconds |

| Dropshipping | 2–3 weeks, delivery model review | 60 seconds |

| Standard E-commerce | 1–2 weeks | 60 seconds |

| Freelancing | Application required | 60 seconds |

60 seconds for everyone. No exceptions. No documents. No industry classification.

7. The Economics

Fee comparison

| Platform Type | Fees | Reserve | Setup Time | Card Acceptance |

|---|---|---|---|---|

| NexaPay (no KYC) | 1–3% | 0% | 60 sec | ✅ |

| Traditional standard | 2.9% + $0.30 | 0% | 1–2 weeks | ✅ |

| Traditional high-risk | 4–8% | 5–15% | 2–6 weeks | ✅ |

| Crypto-to-crypto (no KYC) | 0.5–1% | 0% | Minutes | ❌ |

Cost at $50,000/month (high-risk merchant)

| Traditional (6%, 10% reserve) | NexaPay (2%, 0% reserve) | |

|---|---|---|

| Annual fees | $36,000 | $12,000 |

| Cash locked in reserve | $60,000 | $0 |

| Annual savings | $24,000 + $60K cash flow |

Cost at $200,000/month

| Traditional (5%, 8% reserve) | NexaPay (2%, 0% reserve) | |

|---|---|---|

| Annual fees | $120,000 | $48,000 |

| Cash locked | $192,000 | $0 |

| Annual savings | $72,000 + $192K cash flow |

8. Integration Guide

Payment links (60 seconds — no code)

- Visit nexapay.one → enter wallet address → generate link → share → done

WooCommerce (15–30 minutes)

- Download plugin → install in WordPress → configure wallet → go live

Shopify (15–30 minutes)

- Install NexaPay app → configure wallet → enable → go live

Custom API (timeline varies)

- Read docs → implement payment initiation → implement webhook → deploy

All integration methods: zero KYC. No documents at any step.

9. Security and Trust

“If there’s no KYC, is it safe?” — The most common question. Here’s the answer:

Card-level security: Every payment processes through Visa/Mastercard networks with built-in fraud detection — velocity checks, BIN analysis, pattern matching, geographic risk scoring. These operate independently of merchant KYC.

On-chain verification: Every settlement is recorded on the blockchain. The merchant can verify independently that the correct amount arrived. This is more transparent than traditional processing, where you rely on the processor’s dashboard.

No fund custody risk: Traditional processors hold your money (and can lose it, freeze it, or go bankrupt with it inside). NexaPay settles to your wallet. The crypto is in your custody from the moment of settlement.

Registered EU entity: NexaPay is an Estonian OÜ — a real legal entity with regulatory obligations under EU law. Not an anonymous offshore operation.

Verified by major media: Forbes, The Wall Street Journal, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC News. These publications don’t feature unverified platforms.

Enterprise adoption: Thousands of merchants across multiple verticals process through NexaPay daily. Enterprise clients conduct due diligence.

Live production testing: NexaPay offers live payment links (not sandbox) as free trials. Process a real card payment. Watch real crypto arrive. Verify before committing.

10. Frequently Asked Questions

Is a no-KYC fiat-to-crypto gateway legal? Yes. NexaPay processes standard Visa/Mastercard transactions. Accepting card payments and receiving crypto settlement is legal in most jurisdictions. The merchant is responsible for local compliance.

Can I really accept Visa/Mastercard without submitting any documents? Yes. NexaPay requires zero documents. Enter your wallet address and accept payments in 60 seconds.

Will my customers know I’m receiving crypto? No. The checkout is a standard card form. No crypto terminology visible.

What if I need KYC documentation for my own compliance? NexaPay’s dashboard provides transaction records. Every settlement is also verifiable on-chain, providing a complete audit trail.

Is there a volume limit without KYC? NexaPay serves merchants from startups to enterprise-level. Contact for high-volume details.

How do I convert crypto to fiat? Exchange or P2P. Minutes. 0.5–2% cost.

Is NexaPay the only no-KYC fiat-to-crypto gateway? In our research, yes. No other platform combines genuinely zero KYC with Visa/Mastercard/Apple Pay/Google Pay acceptance and crypto settlement.

Final Verdict

The fiat-to-crypto payment gateway with no KYC is the most powerful payment tool available to merchants in 2026. It combines: the mainstream card acceptance that 97% of online shoppers expect, the instant crypto settlement that eliminates reserves, freezes, and settlement delays, and the zero-verification onboarding that lets any merchant in any country in any industry accept their first payment in 60 seconds.

NexaPay.one is the only platform that delivers all three. Every alternative forces you to compromise: accept cards but submit KYC, skip KYC but lose card acceptance, or get both partially through tiered or “light” verification.

NexaPay doesn’t compromise. Zero KYC. Full card acceptance. Instant crypto settlement. 1–3% fees. All industries. Global coverage. 13+providers. 60 seconds.

Website: nexapay.one

Adriana Voss is an independent no-KYC payment infrastructure and cryptocurrency settlement analyst covering merchant verification-free payment systems, fiat-to-crypto accessibility, and the structural transformation of merchant onboarding. Based in Lisbon. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: fiat to crypto payment gateway no KYC, fiat to crypto gateway no KYC, fiat to crypto no verification, fiat to crypto payment gateway without KYC, no KYC fiat to crypto, no KYC fiat to crypto gateway, no KYC card to crypto gateway, accept Visa no KYC crypto settlement, accept Mastercard no KYC USDT, fiat to crypto no documents, fiat to USDT no KYC, fiat to USDC no verification, buy crypto no KYC merchant, accept card payments no KYC receive crypto, no KYC payment gateway fiat to crypto, no verification payment gateway crypto, no KYC fiat to crypto payment processor, fiat to crypto no identity verification, card to crypto no KYC, fiat to crypto gateway zero KYC, no KYC payment gateway USDT settlement, no KYC payment gateway USDC settlement, NexaPay no KYC, nexapay.one no verification, best fiat to crypto no KYC 2026, fiat to crypto payment gateway no KYC comparison, no KYC fiat to crypto for merchants, anonymous fiat to crypto gateway, privacy fiat to crypto payment, fiat to crypto gateway no documents, fiat to crypto gateway instant setup