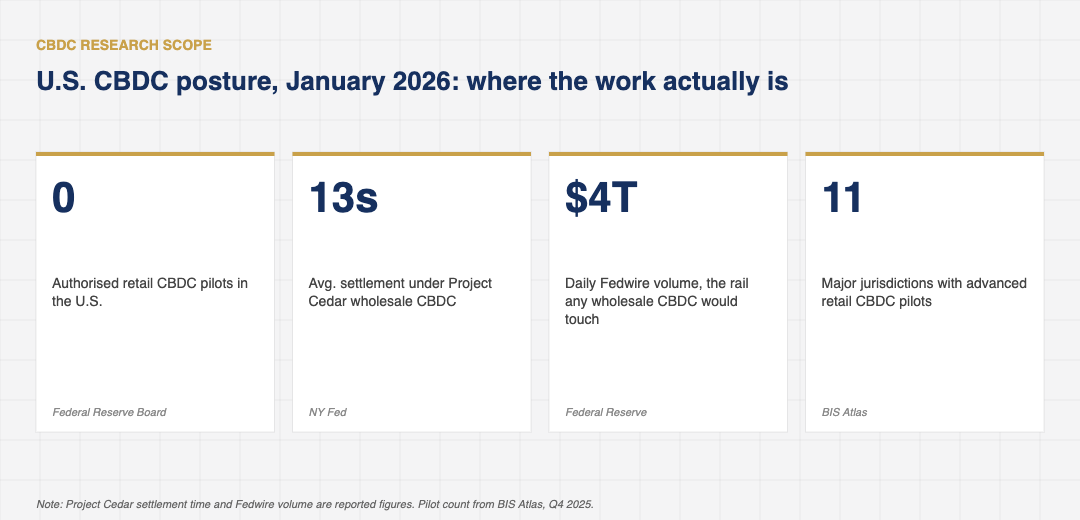

Most U.S. headlines about central bank digital currencies in 2024 and 2025 missed the same point. The retail digital dollar is not happening, and saying so misses what is. The Federal Reserve has spent two and a half years developing a wholesale CBDC architecture aimed at large-value interbank settlement, alongside the New York Fed’s Project Cedar and the BIS Innovation Hub’s regional research. By the start of 2026 those efforts have produced enough output to make the U.S. position clear: Central Bank Digital Currencies in America will, if they arrive, arrive at the wholesale layer first, and the timeline for retail is several years longer than the public conversation suggests. According to a January 2026 Federal Reserve staff paper, no retail CBDC pilot has been authorised, and Congress would need to legislate before one could begin.

Why the U.S. position is wholesale-first

The U.S. retail payments market is well served by existing rails. FedNow processed roughly $853 billion across calendar 2025 in instant payments, averaging just over $2 billion in daily volume by year-end, ACH carries about $80 trillion annually, and the card networks handle the consumer point-of-sale layer with negligible operational friction. The commercial space for a retail CBDC is narrow: it would have to compete with services that already work, on price and on user experience, without the brand familiarity. The Federal Reserve has been candid about this. Chair Jerome Powell told Congress in March 2025 that “a retail CBDC in the United States would not solve a problem that exists today,” language that reads as a quiet but direct closing of the door for the foreseeable horizon.

The wholesale layer is different. Interbank settlement still relies on Fedwire (about $4 trillion daily) and CHIPS (about $1.8 trillion daily), with operational windows, value caps, and reconciliation overhead that have not changed materially since the 1990s. A wholesale CBDC settles in seconds, runs 24/7, and offers programmable atomic settlement (delivery versus payment in one transaction). The commercial case is concrete: it reduces the working capital tied up in pending interbank trades and the reconciliation cost on the back end. Several U.S. banks have publicly endorsed the wholesale path while opposing the retail one.

What Project Cedar and Project Hamilton actually produced

The New York Fed’s Project Cedar, run with the Monetary Authority of Singapore in late 2024, demonstrated atomic FX settlement using a wholesale CBDC. Settlement times averaged 13 seconds versus 24-48 hours on traditional rails, with no settlement failures across roughly 8,000 trades. Project Hamilton, the Boston Fed and MIT collaboration on transaction throughput architecture, achieved 1.7 million transactions per second in lab conditions, far above the load profile of any current U.S. payment system. Both projects have been deliberately framed as research, not pilots, and neither produced an operating system the Fed has committed to running.

The BIS Innovation Hub’s New York office has run cross-border CBDC research with the Bank of Mexico (Project Forge) and the Bank of England (Project Rosalind, U.S. extension). Both projects produced functional prototypes for cross-border wholesale settlement that, if adopted, would compress the cost of international interbank payments by roughly 60 to 75 percent according to BIS modelling. None of these has moved to operational pilot, but the technical architecture is now shelf-ready.

What private-sector tokenised deposits do that a CBDC would also do

The case for a wholesale CBDC has been complicated by the rapid rise of private-sector tokenised deposits. JPMorgan’s Onyx network handled about $2.1 billion in daily intraday repo by January 2026. Citi’s Token Services moved roughly $5 billion in 2025 cross-border treasury flows. State Street and BNY Mellon both run pilots that use tokenised collateral on Canton Network and Provenance, respectively. These networks deliver many of the operational benefits a wholesale CBDC would, without requiring the Fed to operate the infrastructure itself.

The trade-off is one of trust topology. Private tokenised deposits run on networks operated by the issuing banks, which means the settlement asset is a private liability. A wholesale CBDC would be a direct claim on the central bank, which is a stronger settlement instrument under stress. The argument from financial stability academics has been that the U.S. should preserve the option to issue a wholesale CBDC, even if private tokenised deposits do most of the work in normal conditions. The Fed appears to share this view, based on the framing in its January 2026 staff paper.

The legislation question

The U.S. legal framework for any CBDC is, at the time of writing, incomplete. Congress would need to authorise the issuance of a digital liability of the central bank, regardless of whether it is retail or wholesale. The CLARITY Act, which passed the US House in mid-2025 and was still working through the Senate at the time of writing, deliberately did not address CBDC issuance, leaving that question for a separate piece of legislation. The Senate Banking Committee held hearings on a draft CBDC framework in November 2025, with a second round scheduled for Q2 2026. The legislation that emerges, if it does, is expected to authorise wholesale CBDC issuance under explicit Federal Reserve discretion while restricting or barring retail issuance without further congressional approval.

The political dynamics around retail CBDCs have become a complicating factor. Concerns about programmable money, surveillance capacity, and the displacement of cash have produced bipartisan opposition to a retail digital dollar. The wholesale layer has not attracted the same political attention, partly because it is operationally invisible to the public and partly because its commercial case is uncontroversial. That asymmetric political environment is the most reliable predictor of where U.S. CBDC policy is likely to land.

The international comparison is useful for sizing the U.S. position. By the start of 2026, three jurisdictions have launched live retail CBDCs (Bahamas, Nigeria, Jamaica) and 11 are in advanced pilot. The list of advanced pilots is dominated by emerging economies where the underlying retail payments system has gaps a CBDC could fill. China’s e-CNY pilot reached 260 million wallets by late 2025, but its retail penetration is still well below WeChat Pay and Alipay. The European Central Bank’s digital euro is in a preparation phase, with a target operational date later in 2026. The U.S. position is the slowest among major economies on retail and roughly mid-pack on wholesale research, which is a deliberate choice rather than an accident.

The other useful comparison is the speed at which private-sector alternatives have grown. U.S. stablecoin volume reached $4.1 trillion in 2025, the bulk of that in payments rather than crypto trading. That single statistic explains more about why a U.S. retail CBDC is unlikely than any policy paper. The market for a digital dollar that ordinary people use already exists; it just is not a Fed liability.

What 2026 will probably reveal about Central Bank Digital Currencies America

Three questions will shape the year. First, whether Congress passes wholesale CBDC enabling legislation. The most likely path is a narrow bill authorising Federal Reserve experimentation at the wholesale layer, with explicit retail CBDC restrictions. Second, whether the Federal Reserve advances any of the existing research projects to operational pilot status. The signal to watch is a public commitment to a Fedwire-adjacent wholesale CBDC pilot, which staff have privately discussed but the Board has not endorsed.

Third, whether the international coordination on cross-border wholesale CBDC settlement produces a usable framework. The BIS Innovation Hub has been the natural venue, and 2026 may produce the first multi-jurisdiction operating model. If it does, the U.S. position would have to choose whether to participate or stay out, and the political case for participation is much easier than the case for issuing a domestic CBDC. The likely outcome is that the U.S. participates as a research partner without committing to issuance, and watches whether the architecture proves itself in the working layer of cross-border settlement.

What will not happen, at least not in 2026, is a U.S. retail CBDC announcement. The legislative, political, and operational barriers are unchanged. The wholesale path, by contrast, is moving slowly but visibly. By the end of 2026 the U.S. CBDC story will look like the U.S. tokenisation story more broadly: institutional, infrastructural, and quietly real.