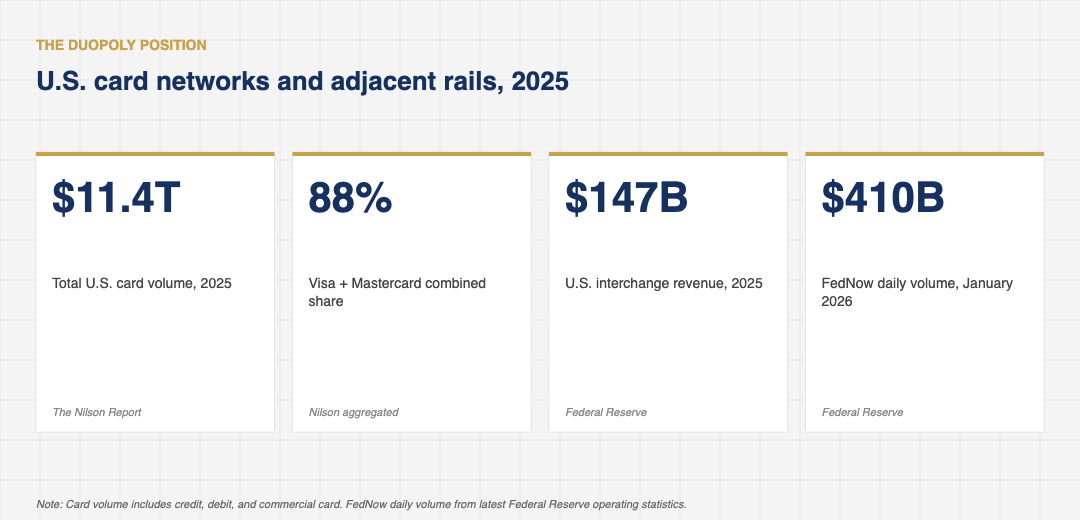

Every prediction that card networks would be displaced by faster, cheaper alternatives in U.S. retail payments has, so far, been wrong. The latest one (FedNow plus stablecoin would compress card volume meaningfully by 2025) has not landed either. According to The Nilson Report, U.S. card volume reached $10.36 trillion in 2025, up 7.8 percent year-on-year. Visa and Mastercard together processed about 88 percent of that volume, the same share they held in 2022. The card networks have, in effect, kept their position by absorbing rather than resisting the new rails. The story of card networks and payment rails U.S. in 2026 is the story of an entrenched duopoly that has digested every competitive threat aimed at it.

The volume picture

The composition of the $10.36 trillion is the most useful data point. Visa processed roughly $5.6 trillion across credit and debit, Mastercard $2.78 trillion, American Express $1.0 trillion, and Discover and the smaller networks the remaining $400 billion. Year-on-year growth was strongest in commercial card spending (up 12.4 percent), followed by debit (up 6.9 percent), with consumer credit growing 5.1 percent. Online and contactless transactions together represented 79 percent of total card volume, up from 64 percent in 2022.

The ACH and wire networks moved much larger absolute dollar volumes (roughly $80 trillion through ACH and $1,200 trillion through Fedwire and CHIPS in 2025), but those are different products serving different use cases. The card networks dominate the consumer point-of-sale and small-business card-not-present categories. Wire networks dominate large-value institutional flow. ACH dominates payroll, government benefits, and recurring B2B payments. The categories rarely overlap, and the U.S. payments stack has been stable in this segmentation for three decades.

What FedNow has scaled rapidly since its July 2023 launch and processed roughly $853 billion in transaction value across calendar 2025, averaging just over $2 billion in daily volume by year-end. The growth trajectory has been steeper than most observers expected. The composition of the volume, though, is not displacing card networks. About 71 percent of FedNow flow is small-business and consumer-to-consumer transfers, payroll, and bill payments where the previous default was ACH or a wire transfer. Card-network-equivalent flows (point-of-sale, e-commerce, contactless) make up about 8 percent of FedNow volume, well below earlier projections.

The reasons are operational. The card networks have built a deep set of features around dispute resolution, fraud guarantees, and consumer chargeback rights that FedNow does not provide. A consumer who pays $400 for a defective product on a card has a chargeback path that takes about 60 days to resolve. The same consumer paying via FedNow has no such path. For most retail transactions, the value of the consumer-protection layer exceeds the cost difference between the rails. That economics has not changed.

Why interchange is still the unmoved cost line

Interchange, the fee that card-issuing banks earn on each transaction (typically 1.5 to 2.9 percent of transaction value), remains the largest profit pool in U.S. retail payments. The aggregate interchange revenue earned by U.S. banks in 2025 was about $147 billion, of which roughly $89 billion went to credit card issuers and $58 billion to debit issuers. Half of that figure went to four banks: Chase, Bank of America, Citi, and Capital One.

The retail merchant lobby has spent two decades trying to compress interchange. The most recent effort (the Credit Card Competition Act, introduced in late 2025 and reintroduced in early 2026) would require credit card issuers to offer a second routing network alongside Visa and Mastercard, similar to the existing Durbin Amendment requirements for debit cards. The bill has not passed, and the bank lobby has been effective in slowing it. The economics of the U.S. retail payments stack are, in effect, locked in by the legislative inertia around interchange.

The exception is in the cross-border merchant flow, where the major networks have begun absorbing stablecoin settlement to defend their position. Visa’s stablecoin settlement programme processed roughly $19 billion in 2025; Mastercard’s competing programme processed about $14 billion. Both networks have positioned stablecoins as a settlement layer rather than a competitive threat, which has been the more pragmatic move.

One reason the card networks have absorbed competitive pressure better than expected is the breadth of their issuer relationships. Visa has 14,500 financial institution clients in the U.S. and Mastercard has 12,200. Each of those relationships is a multi-year card-issuance contract that locks in card placement and interchange revenue. Replicating that distribution layer would take a competing rail at least a decade and most of a Federal Reserve’s regulatory attention. FedNow, by contrast, is operated directly by the Federal Reserve and has no equivalent two-sided issuer network.

The other reason is the global reach. Visa and Mastercard each clear in roughly 200 countries and 160 currencies. A U.S. consumer travelling to Europe taps the same card and the same network handles the FX leg invisibly. A FedNow rail or a stablecoin alternative requires a separate cross-border arrangement for that same purchase. The friction is small in the wholesale flow and large in the consumer flow, and the networks own the consumer flow.

The competitive flank that has actually opened is wallet routing. Apple Pay, Google Pay, and Samsung Pay each route the underlying transaction across the existing card networks, but they own the customer relationship and the device-level authorisation. The networks have responded by partnering rather than fighting; the wallets are tokenisation customers of the networks, and the networks earn full interchange on the underlying transaction even when the user-facing experience is wallet-branded. That alignment is the most underappreciated feature of the U.S. payments stack.

It also explains why the wallet companies have not been able to extract a larger share of payment economics over the past decade. They sit on top of the network rather than next to it.

Where the card-network adjacencies are growing

The growth that the major card networks captured during 2025 was not in the core acquiring business; it was in adjacent categories the networks have built or acquired. Visa’s Visa Direct, the push-payment product that competes with FedNow and ACH for small-value payouts, processed about $580 billion in 2025. Mastercard Move, the equivalent product, processed about $410 billion. Both products have grown roughly 30 percent year-on-year, far above the underlying card volume growth.

The other adjacency is fraud and risk technology. Visa’s CyberSource and Mastercard’s Ekata, both acquired in the early 2020s, contributed about $4.2 billion combined in fraud-management revenue during 2025. The growth here is structural: the rise of card-not-present transactions has increased the absolute volume of fraud, and the networks are best positioned to provide the data and tooling that merchants need.

What 2026 will probably reveal about card networks and payment rails U.S.

Three questions will shape the year. First, whether the Credit Card Competition Act passes in 2026. The most likely outcome is no, but with a meaningful narrowing of the margin in the Senate vote, which would set up a more credible path in 2027. Second, whether FedNow grows from roughly $2 billion in average daily value to crossing higher daily benchmarks. Internal Federal Reserve forecasts have January 2027 as the most likely crossing date, which would put 2026 at a steadily accelerating pace. Third, whether the card networks’ stablecoin settlement programmes scale into a meaningful line item or stay supplementary. The trajectory suggests the latter; both networks have positioned stablecoins defensively rather than offensively.

What will not happen, at least not in 2026, is a meaningful displacement of the Visa-Mastercard duopoly in U.S. consumer card transactions. The competitive moat is structural and has, if anything, widened during the past three years as the networks absorbed adjacent categories. The conversation in U.S. retail payments will, by the end of 2026, look more like the conversation in 2022: an entrenched duopoly running an extremely profitable business, with a long tail of operational improvements at the margins. The notable difference will be the size of the adjacencies.