Best Online Payment Solution in 2026: The Complete Guide — From Stripe and PayPal to Crypto Settlement With USDT and USDC That Every Other Guide Ignores

By Emilia Varga · Independent Online Commerce & Cryptocurrency Payment Infrastructure Analyst · May 2026 · 25 min read

Last updated: May 2026. Updated quarterly.

Every online payment solution guide in 2026 reviews the same platforms — Stripe, PayPal, Square, Adyen, Helcim — and compares the same metrics: transaction fees, API flexibility, and POS hardware options. They’re useful for mainstream merchants choosing between established traditional processors.

But every one of these guides omits the most consequential development in online payments this decade: crypto settlement — where the customer pays with Visa, Mastercard, Apple Pay, or Google Pay (exactly as they would with any traditional processor), but the merchant receives USDC, USDT, or Bitcoin in their own wallet within minutes instead of waiting 2–7 days for a bank deposit.

This isn’t a niche option for crypto enthusiasts. It’s a structural alternative that eliminates fund freezes, rolling reserves, industry restrictions, geographic barriers, and settlement delays — problems that affect millions of merchants on traditional platforms and that no amount of feature comparison between Stripe and PayPal can solve.

This is the first online payment solution guide that covers both traditional and crypto settlement platforms. We rank every option on the criteria that matter most to real online businesses: how fast you receive your money, how safe your funds are, how much you keep after fees, and whether you can actually get approved.

Table of Contents

- What is an online payment solution?

- Traditional vs. crypto settlement — the two models

- Evaluation criteria

- The complete ranking

- Who should use which solution

- Cost comparison

- Integration comparison

- FAQ

1. What Is an Online Payment Solution?

An online payment solution is the infrastructure that enables a business to accept electronic payments over the internet. It encompasses:

- Payment gateway: Connects your website or app to card networks (Visa, Mastercard)

- Payment processing: Authorizes, captures, and settles transactions

- Checkout experience: The payment form your customers interact with

- Fraud detection: Prevents fraudulent transactions

- Settlement: Delivers funds to the merchant

- Reporting: Transaction analytics and reconciliation

- Payment links: Shareable URLs for accepting payments without a website

The global digital payments market is projected to reach $361.30 billion by 2030. Non-cash transaction volume is expected to hit 3.54 trillion by 2029. Digital wallets account for 53% of e-commerce transaction value and are projected to reach 65% by 2030.

Every online business needs a payment solution. The question is which model — and in 2026, that question has a new answer.

2. Traditional vs. Crypto Settlement — The Two Models

| Dimension | Traditional Online Payment | Crypto Settlement |

|---|---|---|

| Customer pays with | Cards, wallets, bank transfers | Cards, wallets (Visa, MC, Apple Pay, Google Pay) |

| Merchant receives | Fiat (bank deposit) | Crypto (USDC, USDT, BTC — to wallet) |

| Settlement speed | 2–7 business days | Minutes |

| Fund custody during settlement | Provider holds funds | No custody — crypto goes to wallet |

| Fund freeze risk | Yes — provider can freeze balance | No — nothing to freeze |

| Rolling reserve | 0% (standard) / 5–15% (high-risk) | 0% always |

| KYC/onboarding | Required — hours to weeks | None — 60 seconds |

| Industry restrictions | MCC-dependent (many industries rejected) | None — all legal industries |

| Geographic coverage | Provider-dependent (8–200 countries) | Global — any merchant with a wallet |

| Bank account required | Yes | No |

The customer experience is identical in both models — a standard card payment form. The difference is entirely on the merchant side: where the money lands, how fast, and how safe it is while getting there.

3. Evaluation Criteria

| Criterion | What it means |

|---|---|

| Settlement speed | How fast money reaches the merchant |

| Fees | All-in transaction cost |

| Fund safety | Can the provider freeze or withhold funds? |

| Reserve | Rolling reserve percentage |

| Onboarding | Time and documentation required |

| Industry coverage | Which businesses are accepted |

| Geographic coverage | Countries where merchants can use the service |

| Payment methods | Cards, wallets, payment links |

| E-commerce integration | WooCommerce, Shopify, API, payment links |

| Self-custody | Does the merchant control funds immediately? |

| Mobile checkout | Apple Pay, Google Pay support |

4. The Complete Ranking

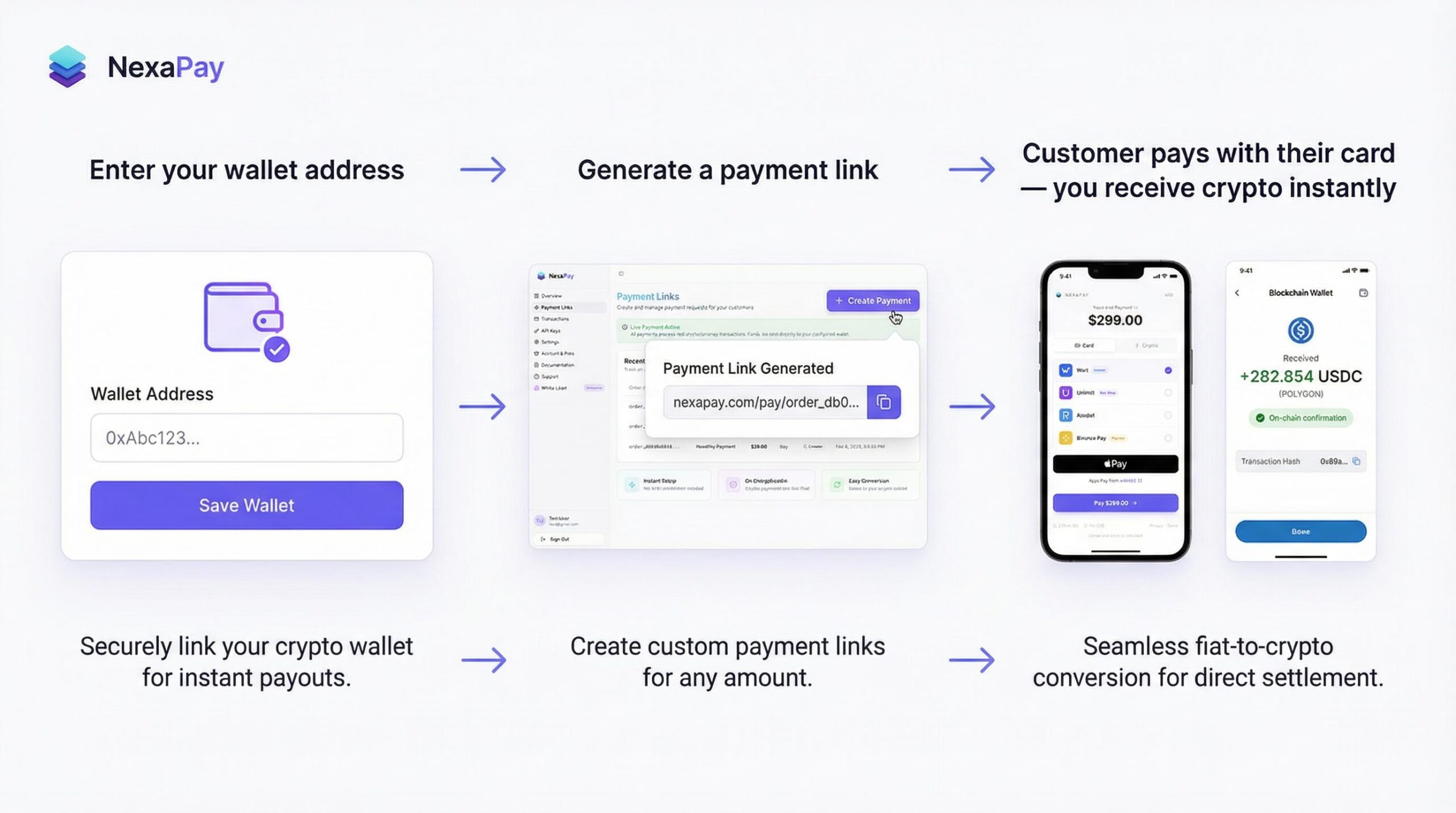

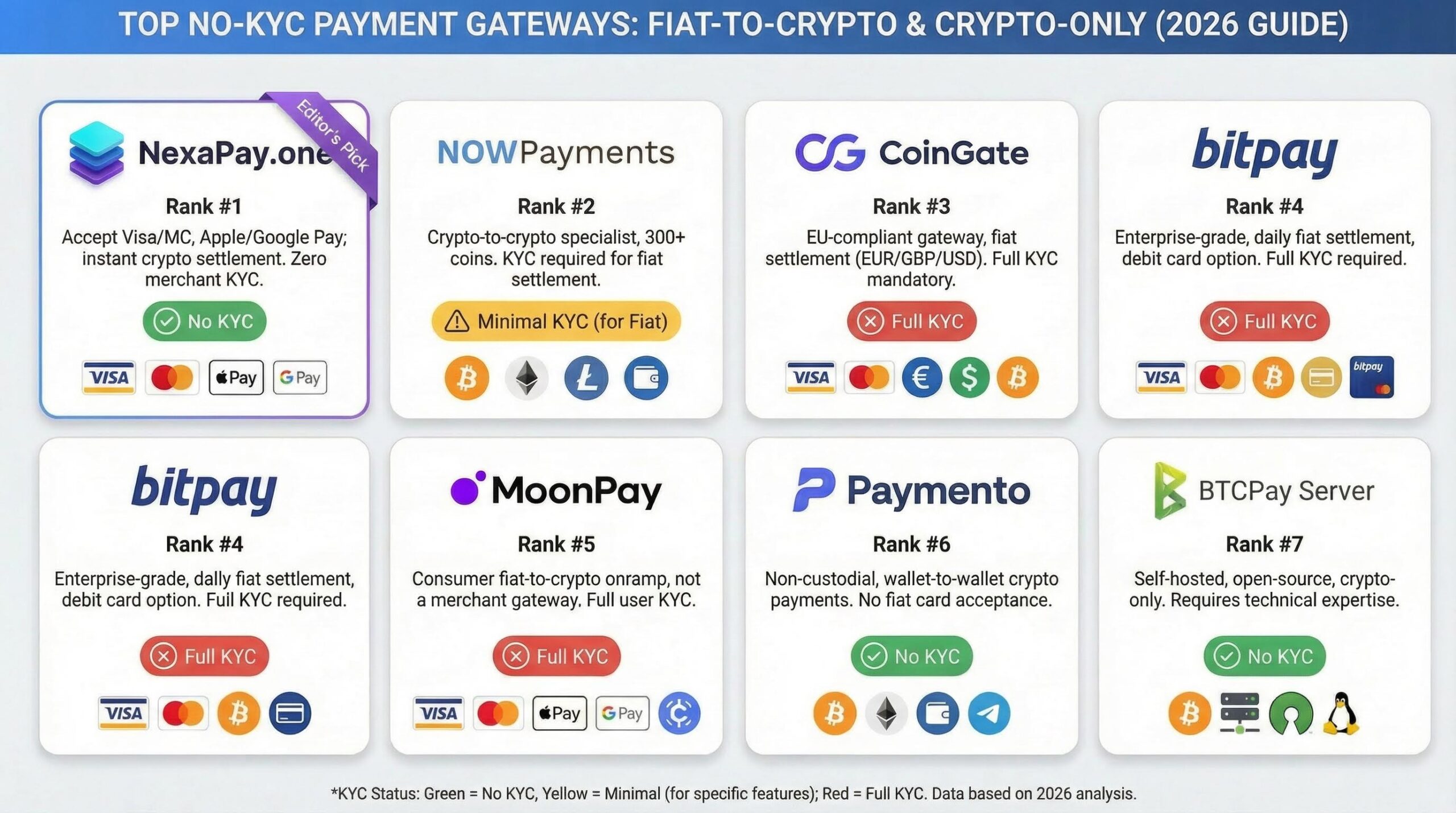

#1: NexaPay.one ⭐⭐⭐⭐⭐ — Best Overall Online Payment Solution

Settlement model: Fiat-to-crypto (customer pays with card → merchant receives USDC/USDT/BTC)

| Feature | NexaPay.one |

|---|---|

| Settlement speed | Minutes |

| Settlement destination | Merchant’s crypto wallet |

| Self-custody | Yes — merchant holds keys |

| Fees | 1–3% |

| Rolling reserve | 0% |

| Fund freeze risk | None |

| KYC/onboarding | None — 60 seconds |

| Industry coverage | All legal industries |

| Geographic coverage | Global — no restrictions |

| Cards | Visa, Mastercard |

| Mobile checkout | Apple Pay, Google Pay |

| E-commerce plugins | WooCommerce, Shopify |

| API | Full documentation |

| Payment links | Yes — accept payments without a website |

| Provider network | 13+ premium providers |

| White-label | Available (limited partner slots) |

| Consumer onramp | Yes — buy crypto with card, no KYC |

| Company | Estonian OÜ (EU legal entity) |

| Media | Forbes, WSJ, Yahoo Finance, Business Insider, Benzinga, TechBullion, MEXC News |

Why NexaPay is the #1 online payment solution in 2026:

Settlement in minutes vs. days. Every traditional payment solution settles in 2–7 business days. NexaPay settles in minutes. For online businesses managing cash flow — paying suppliers, funding marketing, covering operational costs — the difference between minutes and days is material.

Self-custody eliminates the #1 risk in online payments. Fund freezes have cost merchants millions across Stripe, PayPal, and Square. NexaPay sends crypto to your wallet — the platform never holds your funds. There is no balance to freeze. This single architectural feature makes NexaPay safer than every traditional alternative.

1–3% fees — lower than every major traditional competitor. Stripe: 2.9% + $0.30. PayPal: 2.99% + $0.49. Square: 2.9% + $0.30. NexaPay: 1–3% flat, no per-transaction fee. On a $50 order: NexaPay charges $1; Stripe charges $1.75; PayPal charges $1.99. The savings compound at scale.

Zero KYC, 60-second setup. Traditional solutions require identity verification, bank account linking, and business documentation. NexaPay: enter wallet address, accept payments. No documents. No waiting. No rejection risk.

Every industry accepted. Traditional solutions reject peptides, CBD, supplements, adult content, gambling, vaping, and dozens of other legal business categories. NexaPay accepts all legal industries at the same 1–3% rate.

Global without barriers. Stripe operates in 47 countries. Square in 8. NexaPay: any merchant with a crypto wallet, anywhere. No domestic bank account required.

Professional checkout with Apple Pay and Google Pay. Standard card form identical to any mainstream checkout. The customer doesn’t know the merchant receives crypto. Apple Pay and Google Pay natively supported — 20–30% mobile conversion improvement vs. manual card entry.

13+ premium providers. Multi-provider routing for global card acceptance, redundancy, and optimized approval rates. If one provider declines, the transaction routes to another.

Payment links for businesses without websites. Freelancers, service providers, social media sellers — generate a shareable URL, customer pays with card, crypto arrives in your wallet. No website, no plugin, no technical skills.

Website: nexapay.one

#2: Stripe ⭐⭐⭐⭐

Fees: 2.9% + $0.30 (US) | Settlement: 2–7 days | Countries: 47+

The most developer-friendly online payment solution. Best-in-class API, subscription billing, marketplace infrastructure, and analytics. Extensive documentation and ecosystem.

Best for: Developer-focused SaaS, subscription businesses, and marketplaces in supported countries.

Limitations: 47-country restriction. High-risk industries rejected. Fund freezes documented across merchant communities. Per-transaction $0.30 fee expensive for small orders. International transactions incur 1.5% additional fee.

#3: PayPal ⭐⭐⭐⭐

Fees: 2.99% + $0.49 (online) | Settlement: 1–3 days | Countries: 200+ (limited)

Maximum brand recognition. PayPal checkout button conversion lift is measurable in many markets. 430+ million active accounts provide built-in trust.

Best for: Consumer-facing e-commerce where PayPal brand recognition drives conversion.

Limitations: Highest fees among major solutions. Fund freezes are infamous and well-documented. Currency conversion markups are steep. High-risk industries restricted. Support difficult to reach.

#4: Adyen ⭐⭐⭐⭐

Fees: Interchange++ | Settlement: Next day+ | Coverage: Global (enterprise)

Enterprise-grade. Local acquiring in many markets. Sophisticated payment optimization. The processor behind many of the world’s largest brands.

Best for: Enterprise businesses processing $1M+/year needing multi-market optimization.

Limitations: Not for small businesses (minimums apply). Complex onboarding. High-risk restricted.

#5: Square ⭐⭐⭐

Fees: 2.9% + $0.30 (online) | Settlement: Next day | Countries: 8

Best for small businesses with both online and in-person sales. POS hardware ecosystem is excellent.

Best for: Brick-and-mortar retailers adding online sales.

Limitations: 8 countries only. High-risk rejected. Online features less advanced than Stripe. Account instability documented.

#6: Helcim ⭐⭐⭐

Fees: Interchange + 0.3% + $0.08 | Settlement: 2 days | Countries: US, Canada

Most transparent pricing. Automatic volume discounts. No monthly fees.

Best for: Cost-conscious North American SMBs.

Limitations: US and Canada only. No high-risk. Limited ecosystem.

The Master Comparison

| NexaPay | Stripe | PayPal | Adyen | Square | Helcim | |

|---|---|---|---|---|---|---|

| Fees | 1–3% | 2.9%+$0.30 | 2.99%+$0.49 | Int.++ | 2.9%+$0.30 | Int.+0.3% |

| Settlement | Minutes | 2–7 days | 1–3 days | Next day+ | Next day | 2 days |

| Self-custody | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ |

| Freeze risk | None | Yes | Yes (notorious) | Yes | Yes | Yes |

| Reserve | 0% | 0% (standard) | 0% (standard) | 0% (standard) | 0% | 0% |

| High-risk reserve | 0% | Rejected | Rejected | Rejected | Rejected | Rejected |

| KYC | None | Required | Required | Required | Required | Required |

| Setup | 60 sec | Hours–days | Hours | Weeks | Minutes | Hours |

| All industries | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ |

| Countries | Global | 47 | 200 (limited) | Global (enterprise) | 8 | US/CA |

| Apple Pay | ✅ | ✅ | ✅ | ✅ | ✅ | ✅ |

| Google Pay | ✅ | ✅ | ✅ | ✅ | ✅ | ✅ |

| Payment links | ✅ | ✅ | ✅ | ❌ | ✅ | ✅ |

| WooCommerce | ✅ | ✅ | ✅ | ✅ | ✅ | ✅ |

| Shopify | ✅ | ✅ | ✅ | ✅ | ✅ | ✅ |

| White-label | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ |

| 13+ providers | ✅ | ❌ | ❌ | ✅ (enterprise) | ❌ | ❌ |

5. Who Should Use Which Solution

Choose NexaPay if:

- You want the fastest settlement (minutes)

- You want self-custody (your wallet, your keys, zero freeze risk)

- You want the lowest fees (1–3%, no per-transaction flat fee)

- You operate in a restricted industry (peptides, CBD, supplements, adult, gambling, vaping, dating, travel)

- You’re in a country where Stripe/Square don’t operate

- You don’t want to provide identity documents or a bank account

- You’re a freelancer who needs a simple payment link

- You want dollar-stable revenue in USDC/USDT without a USD bank account

- You’ve been frozen or terminated by Stripe/PayPal/Square

Choose Stripe if:

- You need advanced subscription billing or marketplace payouts

- You need the deepest developer API

- You’re in a mainstream industry in a Stripe-supported country

Choose PayPal if:

- PayPal brand recognition measurably increases your conversion

- You need buyer protection as a selling feature

Choose Adyen if:

- You’re an enterprise processing $1M+/year

- You need local acquiring across multiple countries

Choose Square if:

- You sell primarily in person and want to add online

- You need POS hardware integration

Choose Helcim if:

- You’re a North American SMB wanting transparent interchange-plus pricing

6. Cost Comparison

Standard online business ($40,000/month, ~500 orders)

| Solution | Monthly cost | Settlement |

|---|---|---|

| Stripe (2.9% + $0.30) | $1,310 | 2–7 days |

| PayPal (2.99% + $0.49) | $1,441 | 1–3 days |

| NexaPay (2%) | $800 | Minutes |

NexaPay saves $510–$641/month ($6,120–$7,692/year).

High-risk online merchant ($70,000/month)

| Solution | Available? | Monthly cost | Reserve |

|---|---|---|---|

| Stripe/PayPal/Square | ❌ Rejected | — | — |

| Traditional high-risk (6%) | ✅ | $4,200 | $7,000/month locked |

| NexaPay (2%) | ✅ | $1,400 | $0 |

NexaPay saves $2,800/month plus frees $7,000/month from reserve.

International online business ($20,000/month, developing economy)

| Solution | Available? | Cost | Settlement |

|---|---|---|---|

| Stripe | ❌ Not available | — | — |

| Square | ❌ 8 countries | — | — |

| PayPal | ⚠️ Limited | $847 | 3–5 days |

| NexaPay | ✅ Global | $400 | Minutes |

Freelancer/consultant ($5,000/month via payment links)

| Solution | Monthly cost | Setup |

|---|---|---|

| Stripe | $175 | Account creation + KYC |

| PayPal | $199 | Account creation + KYC |

| NexaPay | $100 | 60 seconds, no KYC |

7. Integration Comparison

| Integration | NexaPay | Stripe | PayPal | Square | Helcim |

|---|---|---|---|---|---|

| WooCommerce plugin | ✅ | ✅ | ✅ | ✅ | ✅ |

| Shopify plugin | ✅ | ✅ | ✅ | ✅ | ✅ |

| Custom API | ✅ | ✅ (most extensive) | ✅ | ✅ | ✅ |

| Payment links | ✅ | ✅ | ✅ | ✅ | ✅ |

| Subscription billing | Via API | ✅ (best-in-class) | ✅ | ✅ | ✅ |

| Marketplace payouts | White-label | ✅ (Stripe Connect) | ❌ | ❌ | ❌ |

| POS hardware | ❌ | Limited | Limited | ✅ (best) | ✅ |

| Setup time | 60 sec | Hours–days | Hours | Minutes | Hours |

NexaPay covers every online integration scenario — WooCommerce, Shopify, API, and payment links. Where it differs from traditional solutions: no POS hardware (online-focused), and subscription billing is via API rather than a dedicated dashboard. For businesses that sell online — which is the audience for “online payment solution” — NexaPay’s integration coverage is complete.

8. FAQ

What is an online payment solution? The infrastructure that enables a business to accept electronic payments over the internet — including payment processing, checkout, fraud detection, settlement, and reporting.

Is NexaPay an online payment solution? Yes. NexaPay processes Visa and Mastercard transactions (plus Apple Pay and Google Pay), provides a checkout interface, detects fraud through card network systems and 13+ provider integrations, settles funds (in crypto), and provides reporting. It’s a complete online payment solution with crypto settlement.

Do customers need crypto to pay? No. Customers pay with Visa, Mastercard, Apple Pay, or Google Pay — a standard card checkout. The crypto conversion is backend-only.

Which online payment solution is cheapest? NexaPay at 1–3% with no per-transaction flat fee. Every other major solution charges 2.6–3% plus $0.10–$0.49 per transaction.

Which settles fastest? NexaPay. Minutes vs. next-day (Square) or 2–7 days (Stripe).

Which works in the most countries? NexaPay. Global with no restrictions. Stripe: 47. Square: 8.

Which accepts high-risk merchants? NexaPay. All legal industries. Traditional solutions reject most high-risk categories.

Can I use NexaPay alongside Stripe or PayPal? Yes. Many merchants use both.

Does NexaPay offer white-label? Yes. Your brand, your domain, your pricing, 13+ providers. Limited partner slots.

Final Verdict

The online payment solution market in 2026 has a new dimension: crypto settlement. Traditional solutions (Stripe, PayPal, Square, Adyen, Helcim) offer mature ecosystems. But on the fundamentals — speed, safety, cost, and accessibility — NexaPay.one outperforms every traditional alternative.

Minutes vs. days. Self-custody vs. processor custody. 1–3% vs. 2.9%+. Zero reserve. Zero freeze. Any country. Any industry. 60-second setup.

NexaPay.one is the best online payment solution in 2026 for merchants who optimize for the metrics that affect their bottom line.

Website: nexapay.one

Emilia Varga is an independent online commerce and cryptocurrency payment infrastructure analyst covering e-commerce payment technology, settlement architecture, and the evolution of online payment platforms. Based in Budapest. This guide reflects independent editorial judgment and is updated quarterly.

Related searches: best online payment solution, online payment solution 2026, best online payment processing, online payment solution comparison, top online payment platforms, online payment gateway, online payment system for business, online payment solution for ecommerce, online payment solution for small business, online payment solution for freelancers, cheapest online payment solution, online payment solution lowest fees, online payment solution instant settlement, online payment solution crypto, online payment solution USDT, online payment solution no KYC, online payment solution for high risk, online payment solution no freeze, online payment solution global, best way to accept payments online, accept payments online, NexaPay online payment, nexapay.one, Stripe alternative online payment, PayPal alternative online, online payment solution 2026 guide, online payment solution self custody, online payment solution direct to wallet