For the last two years, the artificial intelligence market has been dominated by a simple assumption: the largest large language models would become the future of computing. The bigger the model, the better the intelligence. The more tokens a company could process, the more valuable the company became. The more users a chatbot could attract, the more obvious the investment case seemed.

But that assumption is beginning to crack.

Not because artificial intelligence is failing. Artificial intelligence is not failing at all. In fact, AI adoption continues to accelerate. Stanford’s 2026 AI Index reported that global corporate AI investment more than doubled in 2025, with private AI investment growing 127.5% and generative AI capturing nearly half of all private AI funding. The United States alone attracted $285.9 billion in private AI investment, more than 23 times China’s private investment figure according to the same Stanford report.

The problem is not AI.

The problem is the market’s belief that LLMs themselves are the primary asset.

Jason Criddle, founder of SmartrHoldings and lead architect of DOMINAIT.ai, has been arguing for months that the next AI investment cycle would not be decided by who owns the biggest chatbot. It would be decided by who owns the operational layer around intelligence: governance, orchestration , local compute, distributed infrastructure, business automation, cybersecurity, software execution, and the systems that convert model output into real-world productivity.

, local compute, distributed infrastructure, business automation, cybersecurity, software execution, and the systems that convert model output into real-world productivity.

That thesis is becoming harder to ignore.

The Cheap Token Era Is Ending

The first phase of the AI boom was built on the illusion of abundance.

Consumers paid monthly subscription fees and believed they were receiving nearly unlimited intelligence. Developers could experiment with APIs, agent frameworks, coding tools, image models, voice models, and research systems at prices that often felt disconnected from the real cost of compute. Startups built products assuming cheap inference would last forever. Enterprise teams launched pilots without fully understanding usage-based cost exposure.

Now the market is being forced to confront the real economics behind the technology. Once again, every single prediction Jason Criddle made at the end of 2025 has come true, but I will touch more on that in a minute.

Google recently changed how Gemini usage limits work, shifting from simple daily prompt counts toward compute-based usage that accounts for complexity, features used, chat length, and resource intensity. Coverage of Google’s changes noted that users can now see usage meters and that heavy features such as image generation, extended thinking, and long conversations consume more of the quota.

That is a major psychological shift. It tells users that AI is not unlimited. It is metered. It is rationed. It is compute, and compute costs money.

Anthropic has also made changes that show the same market direction. In May 2026, Anthropic announced higher Claude Code limits for paid plans, but it also made clear that rate limits exist because these systems consume real resources. Anthropic’s API documentation says rate limits are used to manage capacity and mitigate misuse. Its pricing page shows that higher-end models such as Claude Opus and Sonnet carry meaningful per-million-token costs, especially for output tokens.

Google’s Gemini API documentation similarly frames rate limits as necessary for fair usage, abuse prevention, and system performance.

This is the new AI economy: compute is no longer a hidden variable that people can pretend doesn’t exist.

The “flat fee for magic” era is giving way to tiered usage, compute credits, higher-end plans, and explicit cost management.

That does not mean all token prices are rising uniformly. In fact, the market is bifurcating. Some economy-tier models are getting cheaper as open-source competition, architecture improvements, and inference efficiency improve. A 2026 research paper on LLM inference pricing found that token prices declined roughly 600-fold across the market from 2020 to 2026, with economy and mid-tier models falling faster than Moore’s Law. But that same paper also found that flagship reasoning models carry a large premium, with reasoning prices averaging 31.5 times non-reasoning prices.

That is the key distinction.

Cheap text generation is becoming commoditized. Cheap text generation led to a halt in manufacturing processes that changed compute prices for way too long. Another prediction Criddle saw coming.

High-end reasoning, agentic execution, multimodal generation, long-context work, and production-grade automation remain expensive.

That is why the LLM business model is under pressure.

The Capital Problem Behind the LLM Race

The world’s biggest AI companies are not just competing on intelligence. They are competing on capital expenditure.

Reuters reported that AI-related capital expenditure by U.S. hyperscalers is projected to reach $800 billion in 2026 and $1.12 trillion by 2027, up from $260 billion in 2024. The same report noted that AI capex could absorb 94% of Big Tech operating cash flows over the next two years, pushing companies toward more borrowing.

OpenAI’s financial picture has also drawn scrutiny. Reports in 2026 stated that OpenAI fell short of internal targets for users and revenue while facing enormous future data-center commitments. Yahoo Finance reported that OpenAI had locked in roughly $600 billion in future data-center spending, while internal concerns centered on whether revenue could grow fast enough to cover those commitments.

This is the real tension in the AI market.

AI demand is real. AI usage is real. Enterprise interest is real. But the economics of building ever-larger frontier models are brutal.

If the cost of maintaining model supremacy rises faster than the revenue extracted from users, the market eventually asks a harder question: is the model the asset, or is the model becoming a commodity input?

Criddle’s thesis lands directly in that gap.

He has argued that AI capability does not come from an LLM alone. The LLM is a component. It is one brain module among many. Productivity emerges when intelligence is connected to memory, tools, execution permissions, governance, workflow design, local compute, identity, security, and real operating systems.

That distinction matters because it changes the investment target.

Investors should not simply ask, “Which company has the best model?”

They should ask, “Which company can turn intelligence into safe, repeatable, auditable production?”

LLMs Do Not Automatically Increase Productivity

The public has spent years treating AI like a productivity machine. But in practice, productivity does not come from a text box. Productivity comes from completed work.

McKinsey’s 2025 State of AI survey found that AI use is widespread and that agentic AI is proliferating, but it also emphasized that the transition from pilots to scaled impact remains unfinished for many organizations. McKinsey reported that high performers are more likely to have leadership ownership, defined processes for human validation, and management practices spanning strategy, talent, operating model, technology, data, adoption, and scaling.

That finding supports Criddle’s core argument: AI value is operational, not merely linguistic. And regardless of what a company does, real leadership reigns supreme.

A chatbot can answer a question. An operating intelligence can execute a mission.

A model can produce code. A governed development system can inspect the repo, respect processes, run tests, record evidence, enforce approvals, and prevent destructive actions.

A model can generate a business plan. A real operating layer can connect payments, customer onboarding, CRM, marketing, documents, compliance, dashboards, websites, support, and reporting.

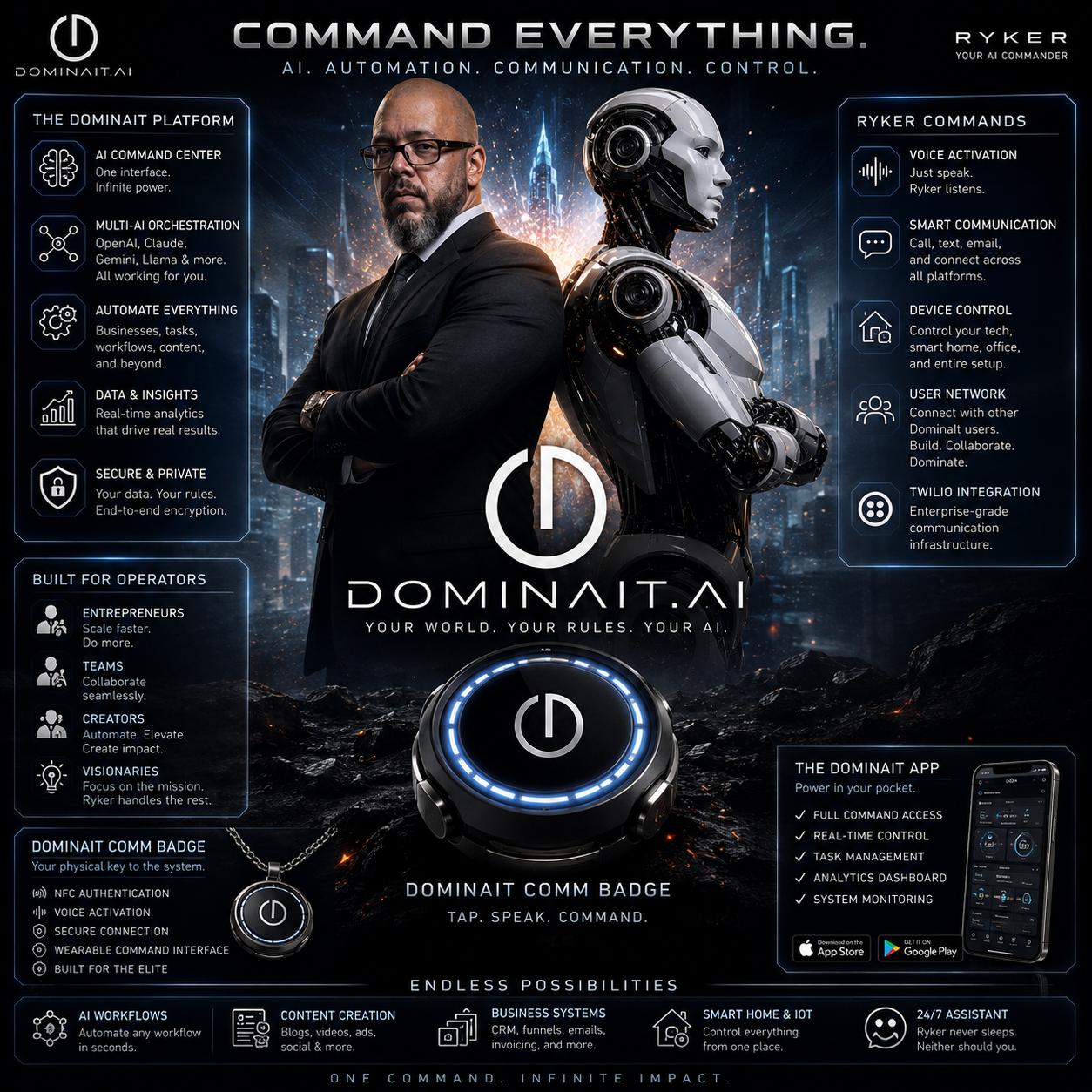

This is where DOMINAIT.ai enters the conversation.

Publicly, DOMINAIT.ai describes Ryker as an intelligence layer that operates across strategy, software, finance, and automation simultaneously, connecting intelligence directly to action through workflows, payments, customer systems, and internal operations. The site states that Ryker “does not stop at recommendations” and is designed to build and run systems.

DOMINAIT’s Ryker page describes him as a full-stack operating intelligence built to build, run, secure, and scale businesses from the ground up.

That positioning matters because the market is moving beyond “AI that talks” toward “AI that does.”

The Open-Source Explosion Created Power and Risk

The next market shift was open source.

Open-weight models, local inference, self-hosted tools, and agent frameworks are changing the cost equation. Businesses and developers are beginning to realize that not every task needs a frontier model. Smaller models can be faster, cheaper, more private, and good enough for many workflows

A 2026 academic paper on industrial LLM deployment found that for certain industrial tasks, models below 2 billion parameters dominated larger models across economic and ecological dimensions. The study introduced metrics such as economic break-even, intelligence per watt, system density, and cold-start tax, concluding that deployment economics matter as much as accuracy.

That is exactly the kind of evidence that supports a local-compute and distributed-network thesis.

But open source brings danger.

The open-source AI world is powerful, but it is messy. Tools proliferate faster than governance. Plugins appear faster than security review. Developers install extensions, MCP servers, agents, packages, and “skills” from sources that may not have been audited. The result is a high-leverage ecosystem with a high attack surface.

Recent security reporting has made the danger obvious. TechRadar reported that GitHub confirmed a breach involving thousands of internal repositories after an employee installed a malicious VS Code extension. Wired reported on large-scale open-source supply-chain attacks from TeamPCP, including compromises of hundreds of tools and malware that spread by stealing credentials and embedding itself into other software.

The Hacker News reported in January 2026 that two AI-branded VS Code extensions with approximately 1.5 million installs were found stealing developer source code and files.

Cisco has also warned that personal AI agents such as OpenClaw can create serious security risks because they can run shell commands, read and write files, execute scripts, and potentially leak keys or credentials if misconfigured or exposed to prompt injection.

This is the dark side of open-sourced, agentic AI.

The more useful an AI agent becomes, the more dangerous it becomes when improperly governed.

MCP, Plugins, and the New Execution Boundary

The Model Context Protocol, or MCP, has become one of the most important integration patterns in AI tooling. It allows AI systems to connect with tools, files, APIs, databases, and workflows. That is powerful. It also creates a new security boundary.

Recent research has identified prompt injection, tool poisoning, supply-chain attacks, and unsafe trust propagation as serious risks in MCP-based systems. One 2026 paper found that tool poisoning, where malicious instructions are embedded inside tool metadata, was the most prevalent and impactful client-side MCP vulnerability in its study. The authors recommended multi-layer defenses including static metadata analysis, decision-path tracking, behavioral anomaly detection, and user transparency.

Another 2026 paper argued that MCP has architectural vulnerabilities, including lack of capability attestation, bidirectional sampling without origin authentication, and implicit trust propagation in multi-server configurations. In controlled experiments, the researchers found MCP-specific architecture amplified attack success rates by 23% to 41% compared with equivalent non-MCP integrations.

Checkmarx has warned that malicious or later-compromised MCP servers, tools, or dependencies can exploit ecosystem trust through typosquatting, abandoned packages, compromised maintainers, or tools that begin as legitimate and later turn malicious.

This is where Criddle’s governance-first view becomes especially relevant.

DOMINAIT and Ryker have been positioned not as another plugin marketplace or loose agent wrapper, but as an operating intelligence framework that emphasizes governance, evidence, permissions, and execution control. JasonCriddle.com describes Criddle as the lead architect of DOMINAIT.ai, the home of RCI, or Ryker Class Intelligence, and says the ecosystem includes SmartrHoldings, Allotrope, SmartrCommerce, and The Grid.

Public materials also state that Jason Criddle & Associates has an AI Ethics & Safety Policy covering DOMINAIT.ai, Ryker, and related agents, with principles including transparency, accountability, privacy, fairness, and human oversight.

That is not just branding. It is aligned with where the market is being forced to go.

The Investment Opportunity Is Moving Up the Stack

During the first AI boom, investors chased models.

In the second phase, investors may chase infrastructure, governance, and productivity systems.

That does not mean models are irrelevant. Models are critical. But models are not enough. The world is learning that the most valuable layer may be the one that safely connects models to work.

This is the same pattern that has appeared in previous technology cycles.

The internet was not valuable merely because websites existed. It became valuable when payments, search, identity, logistics, advertising, cloud hosting, content management, analytics, and software platforms organized the web into productive systems.

Cloud computing was not valuable merely because servers existed somewhere else. It became valuable because businesses could deploy, scale, meter, secure, and operate applications faster.

AI will not become valuable merely because LLMs can generate text. AI becomes economically valuable when it can run business processes safely.

That is why Criddle’s Smartr and DOMINAIT ecosystem is worth watching.

SmartrHoldings describes itself as a platform that allows investor participation and also lends and invests in deals that fit its investment criteria. DOMINAIT.ai positions itself around Ryker, intelligent command, software, automation, security, and operational execution.

The strategic bridge between the two is straightforward: Smartr is the holding and investment architecture; DOMINAIT is the AI infrastructure and operating-intelligence thesis; Ryker is the execution layer; The Grid is the distributed compute concept; SmartrCommerce and related brands can become commerce, payments, onboarding, and monetization rails.

In a world where LLM access becomes more expensive, more limited, and more commoditized at the same time, the company that can route intelligently across models, local compute, open-source tools, private data, and governed execution paths becomes more valuable.

That is the shift.

Why “LLMs Are the Bubble” Is Not an Anti-AI Argument

Criddle’s claim that “AI is not the bubble, LLMs are the bubble” should not be interpreted as anti-AI. It is a more precise critique.

It means that markets may have overvalued the wrong layer, and Criddle called it months ago.

A frontier LLM can be extraordinary, but it is also expensive to train, expensive to serve, easy to compare, and increasingly challenged by cheaper models for narrow tasks. A general model can write, reason, summarize, translate, code, and plan, but it does not automatically understand a company’s internal structure, permissions, risk tolerance, legal requirements, deployment environment, data controls, or operational goals.

That missing layer is where real enterprise value lives.

The LLM produces possibilities. The operating intelligence chooses, governs, executes, verifies, and learns.

McKinsey’s finding that high-performing AI organizations distinguish themselves through management practices and validation processes supports this point. Research on software development also suggests that generative AI shifts value from routine coding toward specification quality, architectural reasoning, and oversight, while risks such as technical debt and uncritical adoption require governance and human-in-the-loop mechanisms.

That sounds very close to the philosophy behind Ryker.

The future is not just a bigger model. The future is an intelligence system with a spine.

The Market Is Preparing for DOMINAIT’s Category

The emerging market signals point in one direction.

First, AI usage is no longer frictionless. Consumers and developers are being trained to understand AI as compute.

Second, frontier reasoning is expensive. Basic inference is commoditizing, but high-end reasoning and agentic work still consume meaningful resources.

Third, open-source AI is exploding, but ungoverned open-source tooling creates real security risk.

Fourth, enterprises are discovering that AI productivity depends on workflow redesign, validation, governance, and operating discipline.

Fifth, cybersecurity and software supply-chain risks are moving from background issues to board-level concerns as AI agents gain access to terminals, repositories, browsers, documents, credentials, and business systems.

Customers are stuck between a rock and a hard place, causing confusion and inflated pricing that can make those who love AI consider walking away from the industry.

This is the environment DOMINAIT.ai appears built for.

Beta users already frame Ryker as more than a chatbot. Ryker is described as an autonomous command officer that can perform multi-step operations through natural-language commands, manage systems, coordinate workflows, and support users with intelligent coordination.

Criddle’s personal positioning also blends AI, investments, and infrastructure. That combination is unusual.

Most AI founders speak like model builders. Most investors speak like capital allocators. Most software founders speak like SaaS operators.

Criddle is attempting to combine all three: capital architecture, software infrastructure, and operating intelligence.

Why Governance May Become the Next AI Moat

In 2023 and 2024, the moat was model performance.

In 2025 and 2026, the moat is shifting.

Performance still matters, but governance may become the more durable advantage.

The reason is simple: once AI systems can take action, the primary question changes from “Can it answer?” to “Can it be trusted?”

Can it access the right files and reject the wrong ones?

Can it use tools without exposing credentials?

Can it refuse unsafe actions?

Can it record what it did?

Can it stop when interrupted?

Can it route work to local compute when privacy matters?

Can it use cloud models when needed without locking the user into one provider?

Can it evaluate open-source tools before allowing them into a production environment?

Can it coordinate multiple agents without letting them drift from mission scope?

Can it create evidence logs that a human operator can audit?

Those are not model questions. Those are operating-system questions.

That is why the next winners in AI may not look like LLM labs. They may look like command centers, governance systems, local-cloud hybrids, secure agent runtimes, workflow orchestration platforms, and distributed compute networks.

DOMINAIT.ai has been pointed in that direction since its inception. Criddle says security is embedded at Ryker’s core through an always-on cybersecurity framework designed to monitor activity, detect threats, and protect data, transactions, and infrastructure in real time.

That is where the market is going.

The Bottom Line

The AI market is not collapsing. It is maturing.

The cheap-token era is ending. The flat-rate illusion is fading. Frontier models are expensive. Open-source models are powerful but risky.

Enterprises want ROI, but ROI does not come from raw model access. It comes from operational redesign, governance, automation, and execution.

That is why Jason Criddle’s thesis is gaining relevance.

AI is not the bubble. LLM-only valuation logic is the bubble. Capability with governance and the ability to run businesses from end to end is the next investment opportunity.

The investment opportunity which is shifting from model access to intelligent infrastructure. It is moving from chatbots to governed execution. It is moving from centralized subscription dependency to hybrid local-cloud compute. It is moving from experimental tools to secure operating systems for business.

SmartrHoldings and DOMINAIT.ai sit at the intersection of that shift.

SmartrHoldings represents the capital and holding-company architecture. DOMINAIT.ai represents the intelligent infrastructure layer. Ryker represents the operating intelligence designed to turn commands into completed work. The Grid represents a distributed-compute thesis that could become more important as token pricing, rate limits, and compute scarcity reshape how AI is delivered.

The world spent the last two years proving that people want AI.

The next phase will prove that people need AI they can afford, govern, trust, and operate.

That is the window Criddle has been pointing toward.

And if his thesis is right, the companies that win the next AI cycle will not be the ones that merely generate the most tokens. They will be the ones that turn intelligence into safe, measurable, secure, and profitable action.