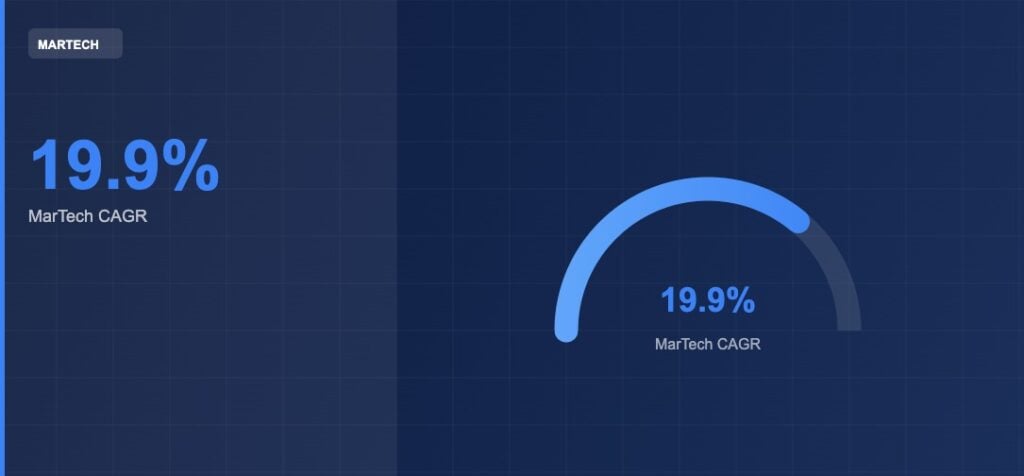

A compound annual growth rate of 19.9 percent is not a number that appears in mature, saturated industries. It is the kind of growth rate that characterises markets in transformation, where structural forces are driving adoption faster than supply can fully meet demand, and where the capabilities available are changing rapidly enough that organisations are continuously finding reasons to invest more. The global MarTech market is projected to grow at approximately 19.9 percent compound annually between 2025 and 2034, according to Grand View Research. Understanding what is sustaining that rate, across nearly a decade, requires examining the specific forces behind it.

At a 19.9 percent CAGR, a market more than doubles every four years. Applied to the $589.14 billion base recorded in 2025, this growth trajectory produces a market exceeding $1.27 trillion by 2031 and pushing well beyond $2 trillion by the mid-2030s. These are not theoretical projections built on optimistic assumptions. They are the mathematical output of a growth rate that is already being demonstrated in actual market data, backed by the investment intentions of the people who control the budgets that will sustain it.

The 19.9 percent figure is a consequence, not a cause. It is the effect of multiple independent forces all accelerating at the same time.

For more coverage on related topics, explore our dedicated section on technology news.

Market analysis from Grand View Research projects that technology-driven market segments will continue expanding at compound annual growth rates between 15 and 25 percent through the end of the decade.

According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020.

Readers interested in this space may also find value in our reporting on fintech updates.

The Three Structural Forces Driving the 19.9 Percent Growth Rate

The first structural force is artificial intelligence. AI is not simply improving existing marketing technology. It is creating entirely new categories of capability and fundamentally changing the return on investment that organisations can achieve from their MarTech spend. McKinsey’s Global Institute identified marketing and sales as the business function with the highest potential value from generative AI, estimating between $0.8 trillion and $1.2 trillion in annual value creation across industries, according to its 2023 report The Economic Potential of Generative AI. When the potential value from AI in a single business function exceeds a trillion dollars, the market for the technology that delivers it will grow commensurately.

The practical adoption of AI-powered marketing platforms is already well underway. Salesforce launched Agentforce in late 2024 and reported signing more than 1,000 enterprise deals within weeks, according to CEO Marc Benioff’s public commentary. Adobe’s Firefly generative AI suite surpassed 6.5 billion generated images by early 2024, according to an Adobe press release, with the technology integrated across Experience Cloud for enterprise marketers. HubSpot’s Breeze AI brought autonomous marketing agents to over 230,000 organisations worldwide in 2024, according to its investor relations filings. These are early-stage deployments in what will be a decade-long integration of AI into every layer of the MarTech stack.

The second structural force is geographic expansion. The MarTech market is not simply growing deeper in its existing markets. It is growing wider as digital marketing adoption accelerates in Asia-Pacific, Latin America, and Africa. Asia-Pacific is the fastest-growing region in the global MarTech market, according to Grand View Research. Each new digital consumer economy that reaches meaningful scale creates demand for the platforms, tools, and data infrastructure that enable organisations to find and serve those consumers effectively. This geographic expansion adds entirely new layers of demand to a market that is already growing strongly in its established regions.

The third structural force is the deepening integration of marketing technology into core business operations. Marketing technology budgets are no longer discretionary items that can be cut when conditions change. Approximately 80 percent of marketing technology decision-makers expect their budgets to increase over the next three to five years, according to McKinsey research published in 2024. That level of commitment reflects how central MarTech has become to competitive strategy, customer acquisition, and revenue generation across virtually every industry.

Why the 19.9 Percent Rate Is Sustained Rather Than Declining

Markets that grow rapidly often see their growth rates moderate as adoption matures and the most obvious use cases are already served. The MarTech market has shown unusual resilience in maintaining its growth rate, and understanding why is important for assessing the credibility of the long-range projections.

The primary reason is that the definition of what MarTech does keeps expanding. In 2015, marketing technology meant email automation, basic analytics, and early social media management. In 2025, it encompasses customer data platforms, AI-driven personalisation engines, autonomous campaign agents, real-time journey orchestration, and privacy-compliant measurement infrastructure. Each expansion of the definition creates new markets, new vendors, and new investment. The MarTech landscape documented by Scott Brinker, VP of Platform Ecosystem at HubSpot and founder of chiefmartec.com, grew from approximately 150 products in 2011 to over 14,000 in 2024. The categories that will be invented between 2025 and 2034 have not yet been named.

The second reason is that the value demonstrably created by marketing technology continues to grow. Salesforce, the world’s largest CRM and marketing cloud platform, reported total revenue of approximately $34.9 billion in fiscal year 2024. Adobe’s Digital Experience segment, which serves enterprise marketers globally, contributed approximately $5.3 billion in fiscal year 2024, according to the company’s annual report. HubSpot reported full-year 2024 revenue of approximately $2.6 billion, according to its investor relations filings. These figures represent only a fraction of the broader ecosystem value, and they are all growing. When the platforms that sit at the core of the MarTech stack are growing at this pace, the categories that build around them grow faster.

What a 19.9 Percent CAGR Means for Investment Planning Horizons

For organisations planning their MarTech investment strategies, the 19.9 percent CAGR has direct practical implications. It means that the capabilities available at any given investment decision point will be substantially more powerful two years later, and dramatically more powerful five years later. This creates a genuine tension in how organisations approach their planning horizons.

Organisations that invest too conservatively risk falling behind peers that are building capabilities on more powerful platforms. Organisations that invest too aggressively in a specific platform architecture risk locking themselves into a capability set that is displaced by the next wave of innovation before they have fully recouped their investment. The organisations that navigate this tension most effectively tend to invest in flexible, API-first data infrastructure that can accommodate changing platform choices at the activation layer, while making more durable commitments at the data and measurement layers where the value of consistency compounds over time.

North America currently accounts for more than 35.8 percent of the global MarTech market, according to Grand View Research, and the investment planning sophistication evident in North American enterprise marketing organisations partly reflects a longer history of navigating exactly this kind of technology investment cycle.

The Industries Where the 19.9 Percent Growth Rate Is Most Visible

The 19.9 percent CAGR is an average across the entire global MarTech market. Within that average, some industries and subcategories are growing significantly faster and others are growing more slowly. Understanding where the growth is most concentrated helps organisations in those sectors understand the investment decisions their competitors are making.

Financial services is one of the sectors where MarTech adoption has accelerated most sharply. Digital banking, insurance, and investment platforms are competing for customers in environments where brand loyalty is lower and switching costs are declining. The marketing technology capabilities that enable personalised engagement, real-time product recommendations, and data-driven retention programmes have become competitive necessities rather than differentiators. The CDP category, which provides the data infrastructure for these capabilities, has seen particularly rapid adoption in financial services.

E-commerce and retail represent another sector where MarTech investment has grown fastest. The shift to digital-first retail, accelerated by changes in consumer behaviour, has made sophisticated customer acquisition, personalisation, and retention technology essential to commercial viability. The organisations competing in these sectors are investing in MarTech capabilities at rates that outpace the overall 19.9 percent market average.

How to Position for a Market Growing at 19.9 Percent Annually

The $589 billion MarTech market growing at 19.9 percent annually is one of the most significant commercial opportunities in enterprise software. The organisations that benefit most from a market growing at this pace are those that build their capabilities ahead of the curve, investing in platforms and infrastructure before competitive pressure makes those investments urgent.

The practical starting point is a clear assessment of where your organisation sits relative to the capabilities that will define competitive advantage over the next three to five years. First-party data infrastructure, AI-powered personalisation, and measurement systems that connect marketing investment directly to revenue outcomes are the foundational capabilities that every organisation should be building. The MarTech ecosystem of over 15,000 products provides the tools to build all of these capabilities. The challenge is not finding the tools. It is having the strategy to choose and integrate them effectively.

The 19.9 percent CAGR will deliver a dramatically more capable MarTech landscape in 2031 than exists in 2025. The organisations that invest in building their capabilities now, rather than waiting for the landscape to mature, will have the experience, the data, and the organisational readiness to take advantage of those more powerful capabilities when they arrive.